If you own a rental property in Spring Lake, you probably focus on how much the home is worth today compared to what you paid. You watch appreciation. You track rent checks in the summer. You smile when property values climb.

But here’s the uncomfortable truth:

Most investors focus on appreciation —

very few optimize their tax position.

And in a high-tax state like New Jersey, that gap can cost you tens of thousands of dollars every year — maybe more.

Filing a tax return is not the same as having a tax strategy. Most landlords file, but few plan. The difference between the two is money in your pocket vs tax dollars handed over to the IRS and NJ Division of Taxation.

If you’re not actively reducing your real estate tax burden — you’re almost certainly overpaying.

Section 1: 5 Signs You’re Overpaying Taxes in Spring Lake

Here are the most common red flags that show your tax strategy is costing you money — not saving it:

1. You’ve Never Done a Cost Segregation Study

Cost segregation breaks your property into parts the IRS lets you depreciate faster.

A proper study can accelerate depreciation, reduce taxable income, and free up cash flow early.

If you own a rental and never explored this, you are almost certainly paying too much tax.

Impact:

Potential accelerated deductions of 5–15x ordinary schedules — money left on the table.

2. Your CPA Files Your Return But Never Runs Projections

If your tax preparer only fills out forms and never models what-if scenarios, you are reacting instead of planning.

- What if you qualified as a real estate professional?

- What if you restructured ownership?

- What if you changed rental classification?

Without modeling, you pay now and regret later.

Impact:

Failing to forecast can cost a portion of loss optimization and passive loss utilization opportunities.

3. You Don’t Know If You Qualify for Real Estate Professional Status

Many investors assume rental loss rules are passive by default.

If you qualify as a Real Estate Professional under IRS rules, you can treat rental losses as active, unlocking deductions that can wipe out taxable income at higher brackets.

But qualification isn’t obvious. It requires:

- More than 50% of your working hours in real estate

- Over 750 hours per year materially participating

- Documented involvement in rental operations

If you haven’t checked this — you might be leaving big savings on the table.

4. You Report Short-Term Rentals as Passive by Default

Many Spring Lake properties generate short-term income — especially in summer.

If your property averages less than 7 days per stay and you materially participate, the IRS can treat your business as active rather than passive.

That changes everything:

✔ You avoid passive loss limitations

✔ You deduct losses against active income

✔ You improve cash flow

But most accountants don’t ask about average stay length or participation level — so this strategy is overlooked.

5. You Haven’t Reviewed Your Entity Structure in Years

How you hold property matters:

- LLC vs S Corp vs individual ownership affects liability and taxes

- Entity elections determine how income and losses flow

- New Jersey has compliance quirks that can inflate liability if ignored

If you haven’t evaluated your structure since you bought your first property, you’re probably paying more tax than necessary.

Section 2: Spring Lake-Specific Rental Pitfalls

These are the mistakes local investors make again and again — and why they cost real money:

Seasonal Rental Income Misclassification

Spring Lake rents spike in summer and swing low in winter. Some owners mix personal use and rental use. If you don’t track days carefully, you can misclassify income and lose deductions.

Example:

Counting personal days as rental days inflates income and shrinks your deductible losses.

Incorrect Expense Allocation

Every dollar counts. But many owners deduct all maintenance as current year expenses when some should be capitalized and depreciated.

- Repairs vs improvements

- Interest and insurance mix

- Shared expenses across properties

Misallocation inflates your current tax burden.

Missing Depreciation Recapture Planning

Depreciation helps today — but recapture taxes haunt owners at sale. Without planning, depreciation recapture can erase years of tax benefit.

A proper strategy anticipates recapture and models future liability before you sell.

Overlooking New Jersey Tax Nuances

New Jersey has some of the highest property taxes in the nation, and it treats rental income differently than other states.

Without state-specific planning, federal strategies can fall flat.

Section 3: Advanced Strategies Most Local Investors Don’t Use

Here’s where serious investors separate themselves from the crowd:

Short-Term Rental Loophole Strategy

If your average stay is under 7 days and you materially participate, you can treat your rental as non-passive — giving you bigger deductions today.

This is not generic rental strategy — it’s active tax planning.

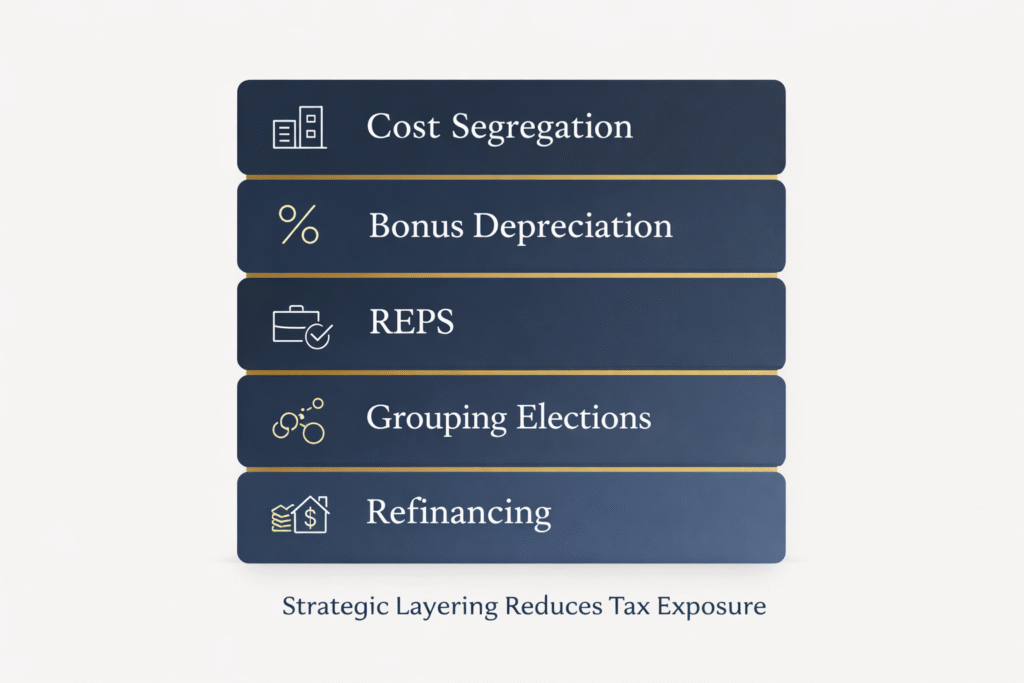

Grouping Elections

You can elect to group related activities for tax purposes so that losses in one activity offset gains in another. This avoids losing deductions due to passive loss limits.

This is a sophisticated IRS tactic — most CPAs never mention it.

Depreciation Stacking

By layering:

- Cost segregation

- Bonus depreciation

- Mid-year and partial year rules

You can accelerate depreciation beyond what many investors think possible.

But without strategy, these stack poorly — or not at all.

Leveraging Refinancing Tax-Free Cash

Refinancing does not trigger capital gains. Smart investors refinance to pull cash out while deferring tax events. That liquidity can be used for:

- Buying another property

- Funding renovations

- Strategic tax moves

Too many owners sell to access cash — unnecessarily triggering tax.

Combining Cost Segregation with Real Estate Professional Status

This combo is a multiplier.

Cost segregation accelerates deductions.

Real estate professional status unlocks them against active income.

Together, they turn passive losses into real savings — faster.

Section 4: Case Scenario — A Real Spring Lake Investor (Hypothetical)

Investor:

Owns 3 Spring Lake rentals valued at $3.2M total.

Without Strategy:

- Annual taxable income from rents

- Standard depreciation only

- No cost segregation

- Passive loss limits apply

Tax owed: $X (federal + NJ)

With Strategy:

- Cost segregation study

- Evaluated STR classification

- Considered Real Estate Professional qualification

- Grouping elections applied

Tax owed: $X – significant savings

The difference isn’t theory — it’s plausible cash savings many investors overlook every year.

Section 5: What Proactive Tax Planning Looks Like

Proactive tax planning doesn’t happen at April 14th.

It happens long before year-end.

A real plan:

✔ Projects multiple scenarios

✔ Integrates federal + NJ rules

✔ Looks at entity structure and rental classification

✔ Coordinates with investment goals

This isn’t reactive tax preparation — it’s forward-looking wealth preservation.

If your Spring Lake portfolio is growing, your tax strategy should evolve with it.

FAQ

Q: Does New Jersey tax rental income differently than federal?

A: Yes. NJ treats rental income under state tax rules that don’t always match federal deductions and depreciation.

Q: What is the short-term rental loophole?

A: If average rental stays are under 7 days and you materially participate, your rental can be treated as non-passive for deductions.

Q: What are passive activity loss limits?

A: Rental real estate losses are generally passive unless you qualify as a real estate professional or meet specific IRS tests.

Q: Is cost segregation worth it for small rental portfolios?

A: Often yes — it accelerates depreciation and improves cash flow, especially for high-value properties.

Q: How much can I save with proactive planning?

A: Every owner’s situation differs, but strategic planning can significantly reduce federal and state tax liabilities.