The tax problem most Indianapolis business owners realize too late

If you run a business in Indianapolis, you’ve likely seen this pattern already. Your revenue grows, your responsibilities increase, and your time disappears — but the money you keep never reflects the effort it took to earn it.

Then tax season arrives, and the numbers explain exactly what happened.

Because in 2026, taxes are no longer just about compliance. They are about control.

What most business owners miss is this: the tax bill you see in April is not created in April. It’s the result of decisions made throughout the year — how you structured your business, how you paid yourself, when you recognized income, and what you invested in.

Once the year ends, those decisions are locked. And that’s where the real problem begins.

If that’s the outcome, the next question becomes obvious — where exactly is the money being lost?

Where Indianapolis business owners actually lose money

Most business owners don’t lose money because they made a mistake. They lose it because they never made a decision in the first place.

Take a typical example. A business owner in Indianapolis earning $400,000 stays structured as a sole proprietor because that’s how they started. No one revisits it. As a result, nearly all of that income is exposed to higher self-employment taxes and top federal brackets.

Nothing illegal happened. Nothing incorrect was filed. But tens of thousands of dollars were lost simply because no one asked if the structure still made sense.

This happens in more places than business structure:

- Income is recognized in the wrong year

- Expenses are taken too late to matter

- Compensation is misaligned with tax efficiency

- Profits are treated as income instead of being redirected

Each decision on its own looks small. Over a full year, they compound into a number that most business owners don’t expect.

And this is exactly where the difference between filing and planning starts to matter — not in theory, but in actual dollars.

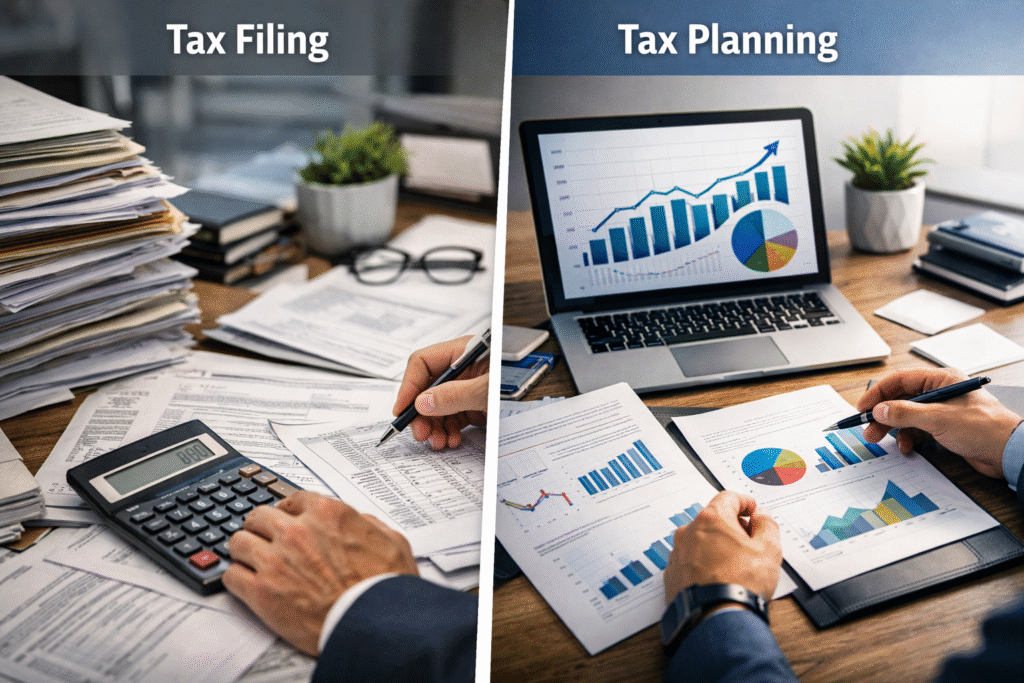

The difference between filing taxes and designing them

Filing is historical. It reports what already happened.

Planning is forward-looking. It changes what will happen before the year closes.

The distinction sounds simple, but the impact is significant.

When a business owner comes to John earning $400,000 structured as a sole proprietor, the first thing he looks at is how much of that income is being taxed unnecessarily at the highest rate. From there, he evaluates whether an S-Corporation election could split income between salary and distributions, reducing exposure to self-employment tax.

That single adjustment can shift thousands of dollars immediately — not by finding a deduction, but by changing how income is treated.

This is what most business owners never experience. They are shown results after the fact, not options before decisions are made.

And once you see that difference clearly, the next question becomes bigger — what is all of this actually building toward?

Tax planning is not about saving money — it’s about building something

Most people think tax strategy is about reducing a bill.

That’s only the surface.

The real objective is to redirect money that would have gone to taxes into assets that grow over time. This is how long-term wealth is built — not by cutting costs, but by reallocating them.

Think of it this way. Every year, your business produces profit. That profit can either:

- Flow out in taxes, or

- Be positioned into assets that appreciate, generate income, and reduce future tax exposure

Real estate is a common example. Instead of paying tax on profit, that same money can be used to acquire property that produces depreciation — offsetting income while building equity.

Over time, these decisions stack. And eventually, they form something much more stable than income alone.

The financial fortress most business owners never build

A business creates income. A strategy turns that income into a financial structure that can stand on its own.

That structure is what many refer to as a financial fortress.

It is built from assets — businesses, real estate, investments — that generate income without requiring constant effort. It is reinforced by tax strategies like depreciation, capital gains treatment, and income timing that reduce ongoing tax exposure. And most importantly, it protects the business owner from volatility, because income is no longer tied to a single source.

Very few business owners reach this point because they never move beyond reactive decisions. They operate year to year, focusing on revenue, without realizing that tax strategy is one of the main tools that converts revenue into long-term wealth.

In fact, only a small percentage of families consistently use the tax code to build wealth over time, which is why most never reach financial independence

Once you understand that, the role of the right advisor becomes much clearer.

What makes a CPA in Indianapolis actually valuable

The difference is not credentials. It’s involvement.

Most CPAs step in after the year ends and organize what already happened. A strategic advisor works inside the year, when decisions are still flexible.

For example, instead of waiting until filing season, John reviews a client’s numbers in Q3. If profit is trending higher than expected, he may recommend accelerating certain expenses, adjusting compensation, or shifting income timing before year-end.

These are not complex ideas. But they only work if they are applied before the deadline passes.

That is where most business owners lose the opportunity — not because they didn’t qualify, but because no one brought it up in time.

And by the time they realize it, the window has already closed.

How to choose the best CPA in Indiana

If you are looking for a CPA in Indianapolis, the real question is not who can file your taxes.

It is who will sit down with you before the year ends and ask:

- Does your current structure still make sense?

- Are you paying yourself the right way?

- Are you recognizing income at the right time?

- Are you using profit to build assets, or just reporting it?

A good CPA answers questions.

A strategic CPA asks the ones you didn’t know to ask.

That difference is subtle at first. Over time, it becomes measurable.

And it usually shows up in one place — how much of what you earn you actually keep.

FAQs: What Indianapolis business owners need to know

Do I really need tax planning if I already have a CPA?

Yes — because most CPAs focus on filing, not forward planning. Filing ensures accuracy, but it does not change your outcome. Planning happens before the year ends and directly affects how much tax you owe. For example, adjusting your entity structure mid-year can reduce tax exposure immediately, while waiting until filing season removes that option. The practical implication is simple: without planning, you are accepting whatever result your current setup produces.

When should tax planning actually start?

Tax planning should begin as early as possible in the year, ideally in Q1 or Q2. This allows enough time to make meaningful adjustments before deadlines pass. For instance, changing how you pay yourself or investing in assets requires time to implement properly. Waiting until Q4 limits your options significantly. The earlier the planning starts, the more control you have over the final outcome.

Can tax strategy really make a big difference in what I pay?

Yes — but not through small deductions. The biggest impact comes from structural decisions like entity selection, income timing, and investment positioning. A business owner earning $300,000 can see a noticeable difference simply by restructuring how that income is categorized. These are not aggressive tactics — they are built into the tax code. The key is applying them before the year closes, not after.

What happens next

Right now, you’re likely doing what most business owners do — running your business, staying profitable, and relying on your CPA to handle taxes when the time comes.

The shift happens when you start making decisions before those numbers are finalized.

That’s where working with John changes the outcome — not by filing differently, but by structuring the year differently while it’s still in motion.

If you want to see what that looks like for your business, the next step is simple:

Schedule a strategy session and review your numbers before this year is locked.