In this comprehensive guide, we’ll explore how the average person—not just billionaires—can legally reduce their tax burden and even pay zero taxes in some cases. If you’ve ever searched for “CPA near me for taxes” to find expert advice, this guide will break down practical tax-saving strategies that cater to the 99%, not just the ultra-wealthy.

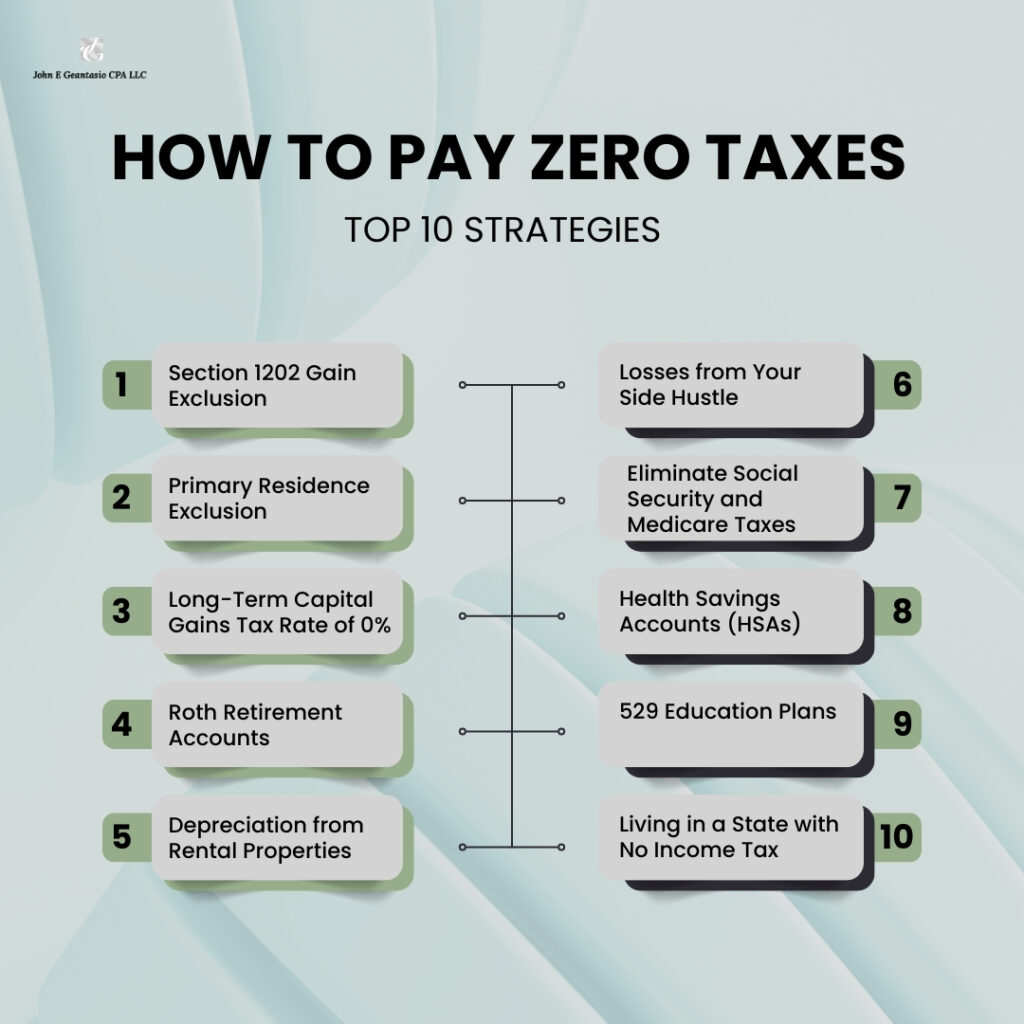

1. Section 1202 Gain Exclusion

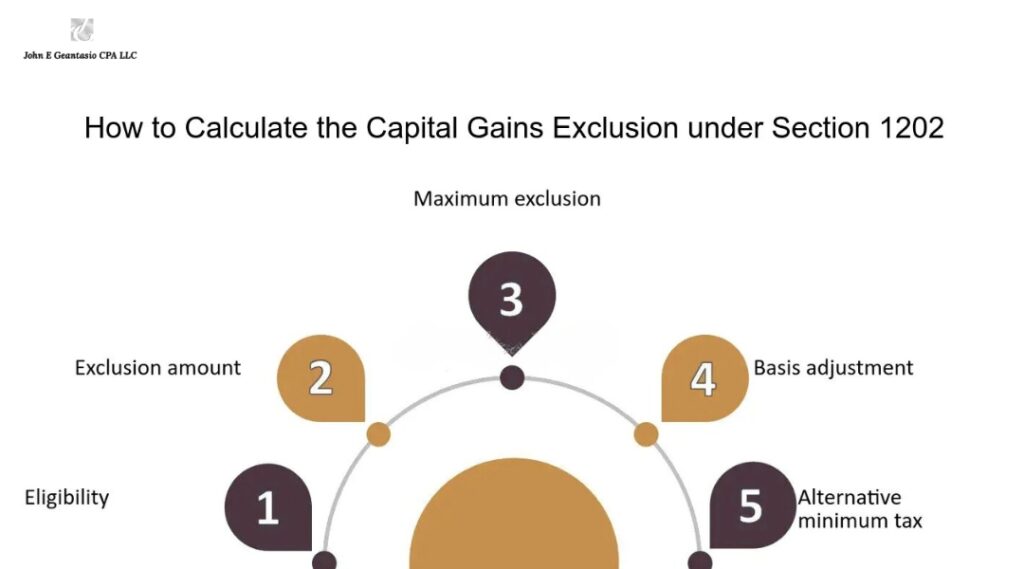

Small business stock investments offer a notable opportunity through Section 1202 of the U.S. Code, which allows for a significant gain exclusion.

For Investors:

- Step 1: Invest in the stock of a qualifying small business.

- Step 2: Hold your investment for at least five years.

- Step 3: Upon selling the stock, up to $10 million of the gain is tax-free.

For Small Business Owners:

- Step 1: Structure your business as a qualifying C corporation or LLC.

- Step 2: After five years, sell your business. Your gain on the sale can be 100% tax-free up to $10 million.

This exclusion doesn’t require a minimum investment amount or any offshoring activities.

2. Primary Residence Exclusion

Homeowners have an opportunity to save on taxes when selling their primary residence, with profits up to $250,000 (or $500,000 for married couples filing jointly) being tax-free if certain conditions are met.

Requirements:

- The home must have been your primary residence for at least 24 months out of the last five years, though these months do not need to be consecutive.

For example, if you lived in your home for a total of two years over a five-year period, with intervals of renting it out in between, you would still qualify for this exclusion.

3. Long-Term Capital Gains Tax Rate of 0%

Investing in stocks or cryptocurrencies and holding them for more than one year could result in a 0% tax rate on the gains if your income falls below certain thresholds, which are adjusted annually for inflation.

Income Thresholds:

- Single filers: Approximately $60,000 or less.

- Head of household: About $80,000 or less.

- Married filing jointly: Around $120,000 or less combined.

It’s essential to prioritise long-term over short-term gains to benefit from this tax-free opportunity, especially in years when your income might be lower.

4. Roth Retirement Accounts

Investments in Roth 401(k)s or Roth IRAs grow tax-free. Withdrawals made after retirement are also tax-free, provided certain conditions are met. This makes Roth accounts an excellent tool for long-term financial planning.

5. Depreciation from Rental Properties

Real estate can depreciate on paper, presenting a tax advantage even as the property’s market value appreciates over time.

How It Works:

- Depreciation is considered an expense against rental income, providing a tax write-off.

- By accumulating enough rental properties and qualifying as a real estate professional, you can remove the limits on how much depreciation you can claim.

6. Losses from Your Side Hustle

If you start a side business and it operates at a loss, those losses can be deducted from your other income, potentially reducing your overall tax liability.

7. Eliminate Social Security and Medicare Taxes

If you’re self-employed, forming an S corporation can help you avoid paying self-employment taxes on a portion of your income, which includes Social Security and Medicare taxes.

8. Health Savings Accounts (HSAs)

HSAs offer triple tax advantages:

- Contributions are tax-deductible.

- The account balance grows tax-free.

- Withdrawals for qualified medical expenses are tax-free.

9. 529 Education Plans

A 529 plan is an education savings plan that offers tax-free growth and withdrawals, provided the funds are used for qualified educational expenses. These plans can be set up for anyone—your children, grandchildren, or even yourself.

10. Living in a State with No Income Tax

Relocating to a state with no income tax can significantly reduce your overall tax burden. States like Florida, Texas, and Nevada offer this benefit, which can be especially appealing to high earners who also face high state tax rates elsewhere.

Final Thoughts

By understanding and utilizing these tax loopholes and strategies, you can legally and effectively reduce your tax liability. To ensure you meet all qualifications and plan your tax strategy according to current laws, it’s best to consult with a CPA near me for taxes who can provide expert guidance tailored to your financial situation.

Frequently Asked Questions:

Ques. Can I use the Section 1202 gain exclusion for any small business investment?

Ans. The Section 1202 gain exclusion applies only to qualified small business stock, and there are specific requirements regarding the type of business, holding period, and issuance date. If you’re considering this strategy, finding a CPA near me for taxes can help ensure you meet all the criteria. Our tax expert, John Geantasio, is available to guide you—book a free initial consultation call to discuss your specific situation.

Ques. How does the primary residence exclusion work if I haven’t lived in my home for two consecutive years?

Ans. The IRS requires that you live in your home as your primary residence for at least 24 months out of the 5 years prior to selling it, but these months do not need to be consecutive. You can split the time as needed. For personalized advice, consider booking a session with our expert John Geantasio.

Ques. What are the income limits for the 0% long-term capital gains rate?

Ans. For 2023, the 0% rate applies if your income is below $41,675 for single filers, $55,800 for heads of household, and $83,350 for married couples filing jointly. These thresholds are adjusted annually for inflation.

Ques. Can I contribute to a Roth IRA at any income level?

Ans. There are income limits for contributing to a Roth IRA. For instance, in 2023, single filers must have modified adjusted gross incomes under $144,000 to contribute the full amount, and married couples filing jointly must have incomes under $214,000. If your income is above these thresholds, your contribution limit starts to phase out.

Ques. How does real estate depreciation work as a tax deduction?

Ans. Depreciation allows you to deduct the costs of buying and improving a rental property over its useful life, acknowledging the property’s wear and tear. This can significantly offset rental income, thereby reducing your taxable income. For details tailored to your properties, book a consultation with John Geantasion.

Ques. Can losses from a side hustle be used to offset other income?

Ans. Yes, if you operate a side business that reports a loss, you can usually deduct those losses from your other income, such as wages or salaries, potentially reducing your overall tax liability. Be sure to keep detailed records and consult with a tax professional like John Geantasion to ensure proper reporting.

Ques. What are the benefits of an S corporation in reducing taxes?

Ans. An S corporation can help reduce taxation by allowing income to pass through to shareholders without being subject to self-employment taxes. This structure is beneficial for avoiding double taxation and reducing payroll taxes on distributed income.

Ques. Are Health Savings Accounts (HSAs) worth it?

Ans. HSAs can be extremely beneficial if you have high-deductible health plans. Contributions are tax-deductible, growth is tax-free, and distributions used for qualified medical expenses are also tax-free. This makes HSAs a powerful tool for managing healthcare costs.

Ques. What is a 529 plan, and how does it help with taxes?

Ans. A 529 plan is an education savings plan that offers tax-free growth and tax-free withdrawals when the funds are used for qualified education expenses. It’s an excellent way to save for college or other educational expenses.

Ques. Is moving to a state with no income tax a good strategy for everyone?

Ans. Moving to a state with no income tax can help lower your overall tax burden, but it’s essential to consider other factors like cost of living, job opportunities, and lifestyle preferences. Consulting with a CPA near me for taxes can provide valuable insights into the financial impact of such a move and help you make an informed decision.

Also Read –

2024 Income Tax Brackets: Federal Tax Rates and What They Mean for You

Tax Saving Tips: Strategic Account Withdrawals for Best Returns