I want to save you from an audit: report all income, especially crypto and side gigs, because the IRS matches data electronically. Keep meticulous records for large deductions like charity or home offices. High earners over $400,000 and those with foreign assets face the most scrutiny. Be consistent and get professional advice.

What are the odds of getting audited by the IRS?

General Odds: Statistically, the chance of being audited remains below 1% for most taxpayers. However, an overall audit rate of 0.4% is observed over the years. So, your odds of getting audited by IRS is pretty low.

What triggers an IRS audit?

• High-Income Earners: Your risk increases exponentially as your income rises. Taxpayers earning over $1 million face audit rates nearly 10 times higher than middle-class filers. For ultra-high-net-worth individuals, the odds of an audit can exceed 10%.

• Business and Industry Specifics:

◦ Marijuana Businesses: This is a extremely high-risk sector, with the IRS examining over 75% of returns in this industry.

◦ Research and Development (R&D) Credits: Claiming this credit makes the audit chance approximately 5 times higher than average. Specifically, the IRS Large Business division audits 80% of large R&D claims.

• Specific Tax Credits and Distributions:

◦ Earned Income Tax Credit (EITC): The audit chance for certain credits like the EITC approaches 80%.

◦ Early Retirement Withdrawals: For those taking large early distributions, the audit rate is 3.2%.

• International Considerations: The audit chance for expatriate returns is nearly triple the national average.

The sources also mention that the IRS uses a discriminant index function (DIF) system to flag returns where deductions exceed statistical norms for similar income levels, meaning the “odds” are often tied to how much your return deviates from the average. Additionally, the IRS has stated they will prioritise enforcement for individuals reporting over £400,000 in annual income (converted from $400,000 in the sources)

How far back will IRS audit?

The IRS can generally examine your tax return for up to three years from the date you filed it or the original due date, whichever is later. This is the standard audit statute under Internal Revenue Code Section 6501.

However, there are important exceptions where the look-back period is longer:

1. Substantial Understatement of Income (25% rule): If you underreport your income by more than 25% of your gross income, the IRS can extend the audit window to six years.

2. Fraud or Willful Evasion: If the IRS suspects fraud or intentional tax evasion, there is no statute of limitations—meaning they can audit and assess tax for any year, no matter how old.

3. Failure to File: If you never filed a tax return, the IRS can go back indefinitely until you do file or they assess a substitute return.

4. Foreign Income / Offshore Reporting (FBAR/ FATCA): For issues involving foreign bank accounts or assets, penalties and audit look-back windows can be extended—even if the underlying return was filed—especially if the IRS considers the omission willful.

Key Practical Points:

Most audits occur within three years. That is the default timeframe.

The IRS often selects returns using data-matching systems that compare information they receive from employers, banks, exchanges, and foreign financial institutions.

Returns with serious discrepancies, unreported income, or aggressive deductions are more likely to be examined.

This comprehensive guide explores 18 major IRS audit triggers in exhaustive detail, providing actionable insights to help you navigate tax season safely.

1. Unreported or Underreported Income: The IRS Already Knows

One of the most common ways taxpayers inadvertently increase their odds of being audited by the IRS is by failing to report all taxable income. The IRS receives copies of every W-2, 1099, and other income documentation through its Information Returns Processing (IRP) system. When your filed return doesn’t match these third-party reports, it creates an immediate discrepancy that often triggers an automated notice or full audit.

The IRS audit chance increases substantially for taxpayers who omit income from:

Freelance work or gig economy platforms (Uber, DoorDash, Etsy)

Rental property earnings

Investment income (dividends, interest, capital gains)

Cryptocurrency transactions

Foreign bank accounts

Cash payments for services

Many taxpayers mistakenly believe small income streams don’t require reporting, but the IRS requires disclosure of all taxable income regardless of amount. Payment apps like Venmo and PayPal now issue 1099-K forms for transactions exceeding $600, meaning the IRS has greater visibility than ever into previously “invisible” income.

To minimize your odds of being audited by the IRS for unreported income:

Cross-check all 1099s and W-2s against your records

Maintain detailed records of side income

Report all income streams, even if under $600

Be aware of new cryptocurrency reporting requirements

Keep business and personal accounts separate

The consequences of unreported income range from simple penalty notices to full-scale audits, especially if the IRS suspects willful evasion. In fiscal year 2022 alone, the IRS identified over $30 billion in unreported income through document matching programs.

2. High Income Earners Face Greater Scrutiny

Your IRS audit chance increases exponentially as your income rises. Recent IRS statistics show that taxpayers earning over $1 million face audit rates nearly 10 times higher than middle-class filers. This increased scrutiny stems from both the potential for larger tax adjustments and the complexity of high-net-worth returns.

The IRS has explicitly stated that enforcement efforts will prioritize:

Individuals reporting over $400,000 in annual income

Complex returns with multiple income streams

Taxpayers with significant investment activity

Business owners filing Schedule C or partnership returns

Those claiming unusual deductions relative to income

For ultra-high-net-worth individuals, the odds of being audited by the IRS can exceed 10%, particularly if they:

Utilize advanced tax strategies like conservation easements

Maintain offshore assets or accounts

Claim large business losses

Have inconsistent year-to-year income reporting

The IRS’s “High Wealth Audit Group” specializes in examining wealthy taxpayers through comprehensive reviews that go beyond the 1040 to analyze related entities, trusts, and financial instruments. These audits often span multiple years and require extensive documentation.

Consider pre-filing disclosure for uncertain positions

While the IRS claims it won’t increase audit rates for those earning under $400,000, the reality is that any return containing red flags may face examination regardless of income level.

3. The Dangers of Not Filing a Return

Failing to file a tax return significantly increases your odds of being audited by the IRS, especially if information documents (W-2s, 1099s) have been submitted under your Social Security number. The IRS’s Automated Substitute for Return (ASFR) program generates assessments for non-filers based on third-party information, often resulting in higher tax bills than if you had filed properly.

The IRS audit chance for non-filers is particularly high for:

Individuals with income over $100,000

Business owners who skip quarterly estimated payments

Those with foreign financial accounts

Recipients of significant investment income

Taxpayers with previous filing compliance issues

Penalties for failure to file can be severe:

5% monthly penalty on unpaid taxes (max 25%)

Additional 0.5% monthly failure-to-pay penalty

Potential criminal charges for willful evasion

Loss of refund claims after 3 years

Levies on bank accounts and wages

The IRS has recently intensified its focus on high-income non-filers through:

Special compliance initiatives targeting missing returns

Automated matching of financial data

Coordination with state tax authorities

Information sharing through international agreements

To reduce your IRS audit chance if you’ve missed filings:

File delinquent returns as soon as possible

Consider the Streamlined Filing Compliance Procedures for offshore issues

Consult a tax professional about penalty abatement options

Stay current with all future filing requirements

Respond promptly to any IRS notices

The IRS’s Non-Filer Program has identified billions in unpaid taxes from individuals who failed to file returns. In 2023 alone, the agency recovered over $500 million from non-filer enforcement actions.

4. Excessive Deductions Relative to Income

Claiming deductions that appear disproportionate to your reported income is one of the surest ways to increase your odds of being audited by the IRS. The agency’s discriminant index function (DIF) system flags returns where deductions exceed statistical norms for similar income levels.

Your IRS audit chance rises significantly if you report:

Business losses year after year

Charitable contributions exceeding 60% of AGI

Home office deductions without proper documentation

Unusually high medical expenses

Excessive business vehicle use claims

The IRS maintains detailed benchmarks for average deductions by:

Income bracket

Profession/industry

Geographic location

Filing status

For example, claiming 50,000incharitabledeductionsona50,000incharitabledeductionsona100,000 salary would immediately raise red flags, as would reporting consistent Schedule C losses while maintaining an affluent lifestyle.

To minimize your IRS audit chance when claiming deductions:

Ensure all write-offs have proper documentation

Compare your deductions to industry averages

Avoid round numbers that suggest estimation

Maintain logs for business use of home/vehicle

Be prepared to justify unusual deductions

The IRS particularly scrutinizes:

Cash charitable contributions without receipts

Large casualty loss claims

Excessive business entertainment expenses

Home office deductions in high-income returns

Medical expenses barely exceeding the 7.5% threshold

If your deductions are legitimate but unusually high, consider attaching explanatory statements to your return preemptively addressing potential questions. This proactive approach can sometimes prevent an audit from being initiated.

5. Large Charitable Contributions Without Proper Documentation

Claiming substantial charitable donations is another factor that can increase your odds of being audited by the IRS, especially if the amounts appear disproportionate to your income or lack proper substantiation. The IRS maintains detailed databases of typical giving patterns and aggressively pursues questionable deductions.

Your IRS audit chance rises when claiming:

Noncash donations exceeding $500 without Form 8283

Gifts of property valued over $5,000 without appraisal

Conservation easements (highly scrutinized)

Donor-advised fund contributions

Fractional interest gifts of artwork or collectibles

The IRS pays particular attention to:

Sudden spikes in charitable giving

Contributions representing large percentages of income

Noncash donations of hard-to-value items

Donations to unfamiliar organizations

Gifts of appreciated property

Required documentation varies by donation amount:

Under $250: Bank record or written acknowledgment

250−250−500: Written acknowledgment from charity

$500+: Form 8283 for noncash gifts

$5,000+: Qualified appraisal for certain property

$50,000+: Detailed appraisal summary

To reduce your IRS audit chance for charitable deductions:

Obtain contemporaneous written acknowledgments

Use qualified appraisers for property donations

Photograph noncash items donated

Maintain records of how valuations were determined

Avoid “overvaluation” of donated property

The IRS has won numerous cases involving inflated charitable deductions, particularly for:

Overvalued vehicle donations

Improperly appraised artwork

Abusive conservation easements

Misclassified personal property as charitable gifts

If you’re making substantial charitable gifts, consider consulting a tax professional to ensure full compliance with increasingly complex substantiation requirements. Proper documentation is your best defense if the IRS questions your deductions.

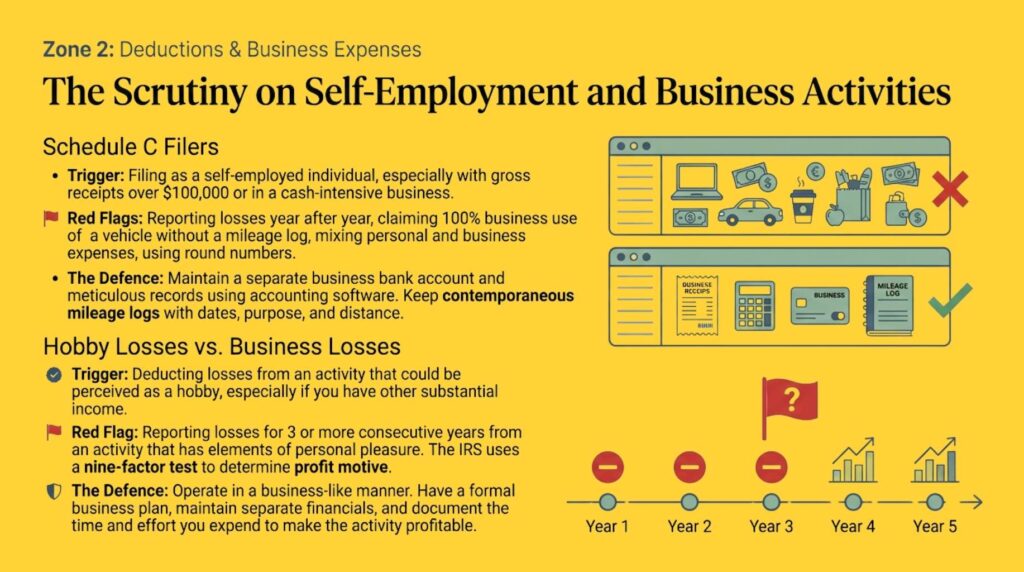

6. Self-Employment and Schedule C Audit Risks

Self-employed individuals and small business owners face significantly higher odds of being audited by the IRS compared to W-2 employees. Schedule C filers represent a disproportionate share of audited returns due to the potential for underreported income and overstated deductions.

Your IRS audit chance increases if you:

Report over $100,000 in gross receipts

Claim 100% business use of a vehicle

Show consistent losses year after year

Have cash-intensive businesses (restaurants, salons, etc.)

Take large home office deductions

The IRS pays special attention to:

Business expenses that seem personal in nature

Round numbers suggesting estimation rather than actual amounts

Deductions disproportionate to income

Sudden changes in reported profit margins

Returns mixing business and personal expenses

Common problem areas include:

Vehicle expenses without mileage logs

Meals and entertainment without business purpose documentation

Home office deductions for occasional use spaces

Excessive “other expenses” categories

Unsubstantiated travel expenses

To reduce your IRS audit chance as a self-employed taxpayer:

Maintain separate business bank accounts

Keep detailed mileage logs with dates/purposes

Retain receipts for all deductible expenses

Document business purpose for questionable expenses

Use accounting software to track income/expenses

Avoid mixing personal and business funds

The IRS has sophisticated tools to detect questionable Schedule C filings, including:

Industry-specific income/expense ratios

Cash transaction analysis

Comparison to similar businesses in your area

Matching against information returns (1099s, etc.)

If you’re self-employed, investing in proper record-keeping systems and potentially working with a tax professional can pay dividends by reducing audit risk while ensuring you claim all legitimate deductions.

7. Hobby Losses vs. Legitimate Business Deductions

The distinction between a hobby and a business is a frequent audit trigger that can significantly increase your odds of being audited by the IRS. The agency closely examines activities that generate consistent losses, particularly when taxpayers have other substantial income sources.

Your IRS audit chance rises if you:

Report losses from an activity for 3+ consecutive years

Have significant income from other sources

Participate in the activity irregularly

Lack business licenses or professional credentials

Don’t maintain proper business records

The IRS applies a nine-factor test to determine profit motive:

Whether you carry out activity in businesslike manner

Expertise of taxpayer or advisors

Time and effort expended

Expectation that assets may appreciate

Success in similar activities

History of income/losses

Amount of occasional profits

Financial status of taxpayer

Elements of personal pleasure/recreation

The “3-of-5” year rule creates a presumption of profit motive if you show a net profit in any 3 of 5 consecutive years (2 of 7 for horse breeding). However, this is only a presumption – the IRS can still challenge activities that meet this test but appear hobby-like.

To reduce your IRS audit chance for activity losses:

Maintain separate business bank accounts

Develop a formal business plan

Keep detailed records of time spent

Document efforts to improve profitability

Obtain necessary business licenses

Track income/expenses using accounting software

If your activity is legitimate but hasn’t yet turned profitable, consider attaching a statement explaining your profit strategy and progress. This can sometimes preempt IRS questions about your deductions.

The IRS wins most hobby loss cases that go to court, so proper documentation is essential if you’re deducting losses from an activity that could be viewed as recreational rather than commercial.

8. Misclassified Self-Employment Income: A Growing IRS Target

The IRS has dramatically increased scrutiny of self-employment income classification, directly impacting your odds of being audited by the IRS. This issue particularly affects LLC members, limited partners, and gig workers who may incorrectly avoid paying self-employment taxes. The IRS audit chance spikes when filers attempt to characterize earned income as passive investment income to evade the 15.3% self-employment tax.

Recent court cases have established important precedents that increase your IRS audit chance:

Hedge fund managers (Tax Court 2023): Active participants must pay SE tax regardless of LP status

Law firm LLC members (Tax Court 2022): Professional service providers cannot claim passive treatment

Real estate investors (Tax Court 2021): Material participation triggers SE tax obligations

The IRS uses several indicators to identify misclassification:

1099-MISC/1099-NEC forms showing significant income without Schedule SE

Schedule K-1 filings with guaranteed payments to active participants

Social media profiles or websites demonstrating active business involvement

State business licenses requiring personal participation

To reduce your IRS audit chance regarding self-employment taxes:

Properly document your role in any business entity

File Schedule SE if you actively participate in operations

Review LLC operating agreements for guaranteed payment clauses

Maintain time logs proving passive vs. active involvement

Consult a tax professional when structuring business entities

The IRS’s Self-Employment Tax Compliance Initiative has recovered over $900 million in unpaid taxes since 2020, primarily from:

Doctors and lawyers in LLCs

Hedge fund and private equity partners

Real estate professionals

Gig economy workers with multiple 1099s

9. Rental Real Estate Losses: Passive Activity Rules

Claiming rental real estate losses improperly will substantially increase your odds of being audited by the IRS. The IRS audit chance escalates when taxpayers attempt to deduct rental losses against other income without meeting strict passive activity rules. The IRS maintains specialized audit teams focused exclusively on real estate tax compliance.

Critical thresholds affecting your IRS audit chance:

The IRS Real Estate Audit Technique Guide reveals their focus areas:

Verification of 750+ hours across all properties

Comparison to primary occupation time commitments

Analysis of property management company usage

Review of advertising and tenant screening processes

Recent audit statistics show:

72% of real estate professional audits result in adjustments

Average additional tax assessed: $28,500 per audit

Most common disallowed deductions: Travel, depreciation, and repairs

10. Questionable Refundable Tax Credits

Claiming refundable tax credits incorrectly will dramatically increase your odds of being audited by the IRS. The IRS audit chance approaches 80% for certain credits like the Earned Income Tax Credit (EITC), making proper documentation essential.

High-risk credits that increase IRS audit chance:

Credit

Improper Payment Rate

Key Audit Triggers

EITC

33%

Qualifying child tests, income limits

ACTC

28%

SSN validity, relationship tests

AOTC

22%

Enrollment status, 4-year limit

PTC

19%

Marketplace documentation, income reconciliation

EITC-specific audit triggers:

Children not meeting residency requirements

Income above threshold amounts

Invalid Social Security numbers

Claiming a child already claimed elsewhere

American Opportunity Credit red flags:

Claiming for more than 4 tax years per student

Missing Form 1098-T from educational institution

No documentation of qualified expenses

Claiming for ineligible students (graduate programs)

Premium Tax Credit compliance issues:

Failure to reconcile advance payments

Household income above 400% poverty level

Incorrect family size reporting

Lack of Marketplace insurance documentation

Documentation strategies to reduce audit risk:

School enrollment verification for education credits

Medical insurance forms for PTC reconciliation

Birth certificates for child-based credits

Full-year residency proof for EITC qualifying children

The IRS Automated Underreporter Program flags over 5 million credit claims annually, with nearly $14 billion in improper payments identified in 2023 alone. Taxpayers claiming these credits should be prepared for potential review and maintain all supporting documents for at least 6 years.

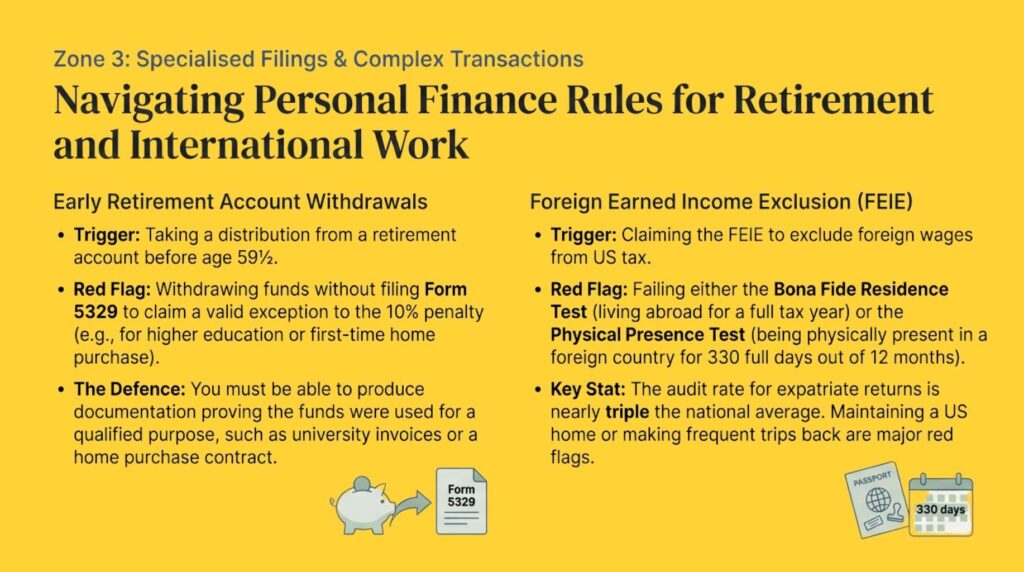

11. Early Retirement Account Withdrawals

Taking early distributions from retirement accounts significantly increases your odds of being audited by the IRS. The IRS audit chance spikes when taxpayers withdraw funds before age 59½ without properly documenting exceptions to the 10% penalty. IRS compliance programs specifically target retirement account distributions.

Most heavily scrutinized early withdrawals:

Substantially equal periodic payments (72(t) plans) with calculation errors

Medical expense withdrawals without corresponding bills

Higher education payments without enrollment verification

Documentation requirements:

Form 5329 must be filed to claim exceptions

Proof of qualified expenses for education/medical withdrawals

Actuarial calculations for 72(t) payment plans

Home purchase contracts for first-time buyer exceptions

Recent enforcement statistics:

2.8 million taxpayers made early withdrawals in 2022

$1.3 billion in penalties assessed

Audit rate for large early distributions: 3.2% (vs. 0.4% overall)

Red flags increasing IRS audit chance:

Multiple early withdrawals in same tax year

Distributions followed by large purchases (boats, vacations)

No corresponding Form 5329 filed

History of early withdrawals

Strategies to reduce audit risk:

Directly pay institutions for qualified expenses

Maintain paper trails linking withdrawals to allowed purposes

Consult tax professionals before taking distributions

Consider alternatives like loans before early withdrawals

The IRS Retirement Plan Compliance Unit uses sophisticated tracking systems to identify questionable distributions, making proper documentation essential for anyone needing early access to retirement funds.

12. Alimony Deduction Errors

Incorrectly claiming alimony deductions will increase your odds of being audited by the IRS. The IRS audit chance escalates when divorce agreements don’t meet strict tax law requirements or when ex-spouses file inconsistent returns. The IRS has implemented new matching programs specifically targeting alimony reporting.

Critical timing rules affecting deductibility:

Pre-2019 agreements: Deductible if meeting all requirements

Post-2018 agreements: Never deductible under TCJA changes

Modified agreements: Must explicitly adopt new tax treatment

Audit triggers for alimony deductions:

Missing ex-spouse’s Social Security number

No divorce/separation instrument attached

Payments continuing after recipient’s death

Contradictory reporting between ex-spouses

Required documentation:

Written divorce decree specifying alimony

Payment records (cancelled checks, bank statements)

SSN verification of recipient

Termination clauses regarding death/remarriage

Recent enforcement data:

34% mismatch rate in alimony reporting

$240 million in adjustments from 2022 audits

Average additional tax assessed: $6,800 per case

Strategies to reduce audit risk:

File Form 1040 Schedule 1 with recipient’s SSN

Ensure decree language complies with tax law

Coordinate reporting with ex-spouse

Maintain payment records for 7+ years

The IRS Alimony Audit Technique Guide reveals their focus on:

Cash payments without documentation

Property settlements mischaracterized as alimony

Child support payments incorrectly deducted

Agreements modified after 2018 without proper language

Taxpayers claiming alimony deductions should be prepared for potential review, especially if payments are substantial or recently modified. Proper documentation is the best defense against audit adjustments.

13. Gambling Winnings and Losses: A High-Stakes Audit Trigger

Failing to properly report gambling income is one of the fastest ways to increase your odds of being audited by the IRS. The IRS audit chance skyrockets when taxpayers either omit casino winnings or exaggerate losses, as gaming establishments electronically report all significant payouts directly to tax authorities.

Key thresholds that trigger IRS scrutiny:

Slot machine jackpots of $1,200+ (reported on W-2G)

Table game wins of $5,000+ (reported for tournaments)

Sports betting net wins of $600+ with 300+ times odds

Poker tournament winnings exceeding $5,000

Documentation requirements to reduce audit risk:

Maintain detailed win/loss statements from all gambling venues

Keep original tickets and wagering records for sports betting

Document session records showing dates/locations of play

Obtain casino player card statements showing annual activity

Common audit triggers:

Claiming large losses without corresponding W-2G forms

Reporting net losses instead of gross winnings

Failing to itemize deductions while claiming gambling losses

Inconsistent reporting between state and federal returns

Professional gambler considerations:

Must report on Schedule C with ordinary income rates

Can deduct legitimate business expenses

Subject to self-employment taxes

Must prove profit motive and regularity of play

The IRS Gambling Audit Technique Guide reveals their examination focus:

Comparing W-2G forms to reported income

Verifying loss deductions don’t exceed winnings

Checking for personal expense deductions disguised as gambling losses

Reviewing bank records for unreported withdrawals at gaming venues

14. Foreign Earned Income Exclusion Mistakes

Claiming the Foreign Earned Income Exclusion (FEIE) improperly will substantially increase your odds of being audited by the IRS. The IRS audit chance for expatriate returns is nearly triple the national average, as the IRS has dedicated international exam teams scrutinizing these filings.

Critical requirements for FEIE qualification:

Bona fide residence test: Full tax year in foreign country

Physical presence test: 330+ days abroad in 12-month period

Tax home requirement: Work base must be overseas

Income limitations: $126,500 maximum exclusion (2024)

Red flags that trigger audits:

Maintaining a U.S. home while claiming exclusion

Frequent return trips to the United States

Working for U.S. government or military overseas

Failing to file Form 2555 with proper documentation

Documentation strategies:

Passport stamps proving physical presence

Foreign lease agreements or property deeds

Local tax filings in host country

Employer verification letters confirming work location

Recent enforcement trends:

Increased coordination with foreign tax authorities

Social media monitoring for evidence of U.S. presence

Focus on “digital nomads” working remotely abroad

Scrutiny of COVID-era work location claims

The IRS International Individual Compliance Program has collected over $1.2 billion in additional taxes from expat audits in the past three years, making proper documentation essential for anyone claiming the FEIE.

15. Marijuana Business Deductions: A High-Risk Industry

Operating a cannabis business dramatically increases your odds of being audited by the IRS, with the agency examining over 75% of returns from this industry. The IRS audit chance remains exceptionally high due to Internal Revenue Code Section 280E, which prohibits standard business deductions for drug trafficking organizations.

Current tax treatment of marijuana businesses:

Allowed deductions: Cost of goods sold (COGS) only

Prepare for 100% documentation requests during audits

The IRS Marijuana Industry Compliance Program has collected over $300 million in additional taxes from cannabis business audits since 2018, making professional tax guidance essential for operators in this high-risk sector.

16. Research and Development (R&D) Tax Credit Claims

Aggressively claiming the R&D tax credit can significantly increase your odds of being audited by the IRS. The IRS audit chance for returns claiming this credit is approximately 5 times higher than average, as the IRS battles widespread abuse by both businesses and unethical tax preparers.

Four-part test for qualified research:

Permitted purpose: New or improved function/performance

Technical uncertainty: Technological information unknown

Process of experimentation: Systematic trial-and-error

Technological in nature: Hard sciences principles

Common audit triggers:

Claiming credit for routine business activities

Including ineligible personnel costs

Failing to properly document research activities

Claiming the credit without Form 6765

Aggressive allocation methods for qualified expenses

Documentation best practices:

Project lists with technical challenges

Payroll records showing researcher time

Lab notebooks and experiment logs

Patent applications supporting research

Project meeting minutes discussing uncertainties

Recent enforcement actions:

IRS Large Business division auditing 80% of large R&D claims

Criminal investigations of fraudulent credit mills

New requirements for detailed project descriptions

Focus on software development claims

The IRS R&D Credit Audit Technique Guide reveals their examination priorities, making proper documentation and conservative claiming essential for businesses seeking this valuable credit.

17. Cryptocurrency and Digital Asset Transactions

Failing to properly report cryptocurrency transactions is one of the fastest-growing audit triggers that increases your odds of being audited by the IRS. The IRS audit chance for crypto investors has quadrupled since 2020, as the agency receives increasing amounts of data from exchanges and blockchain analysis firms.

Key reporting requirements:

Form 1040 question: Must answer truthfully about crypto activity

Capital gains reporting: Required for all trades/exchanges

Income reporting: Mining rewards, staking income, airdrops

FBAR filings: For foreign exchange accounts exceeding $10,000

Audit red flags:

Large transactions without reported cost basis

Inconsistent reporting between exchanges and tax return

Failure to report DeFi or NFT transactions

Omitting crypto received as payment for services

Claiming excessive losses without documentation

Compliance strategies:

Use crypto tax software to reconcile all transactions

Maintain records of wallet addresses and private keys

Document cost basis for all acquisitions

Report forks and airdrops as ordinary income

Consider filing amended returns for past omissions

The IRS Virtual Currency Compliance Campaign has resulted in:

Over 10,000 warning letters sent to crypto holders

John Doe summonses to major exchanges

Development of blockchain forensic tools

Coordination with international tax authorities

With the IRS prioritizing crypto enforcement, proper reporting is essential to avoid severe penalties that can reach 75% of unpaid tax for willful violations.

18. Foreign Bank Account Reporting (FBAR) Violations

Failing to disclose foreign financial accounts will dramatically increase your odds of being audited by the IRS. The IRS audit chance for taxpayers with international connections is exceptionally high, as the agency receives automatic account information from over 100 countries under FATCA and other agreements.

Critical reporting thresholds:

FBAR (FinCEN 114): Aggregate $10,000+ in foreign accounts

Form 8938: Higher thresholds based on residency (50,000−50,000−600,000)

FATCA reporting: Required by foreign financial institutions

Penalty risks:

Non-willful violations: $10,000 per account per year

Willful violations: Greater of $100,000 or 50% of account balance

Criminal charges: Possible for deliberate concealment

Audit triggers:

Foreign address on tax return

Foreign-sourced income

FATCA data received from foreign banks

Large unexplained deposits or withdrawals

Prior non-compliance history

Compliance options:

Streamlined Filing Procedures: For non-willful violations

Delinquent FBAR Submission: For missed filings without IRS notice

Voluntary Disclosure Program: For willful violations

The IRS Offshore Compliance Initiative has collected over $15 billion since 2009, making proper foreign account disclosure essential for anyone with international financial connections. With automatic data exchanges now routine, the risk of detection has never been higher.