Looking to launch your dream business or give your existing one a boost? You might be familiar with traditional funding options like SBA loans or lines of credit. But there’s another option gaining traction: 401(k) Business Financing, also known as ROBS.

ROBS allows you to tap into your retirement savings, specifically your 401(k), to fund your business without the burden of debt or risking your personal assets as collateral. This can be a great way to expedite access to capital, especially if you don’t have a stellar credit score or haven’t built up a lot of cash reserves. Let’s dive deeper and explore the ins and outs of ROBS, including its benefits and potential downsides.

Funding Your Business with Retirement Savings: How ROBS Works

ROBS, or Rollover for Business Startups, allows you to use your retirement savings to fund your business venture. This can be a great option if you have money saved in a retirement account like a 401(k), IRA, 457(b), 403(b), Thrift Savings Plan (TSP), or similar plans.

Normally, if you take money out of your retirement account before you reach age 59½, you’ll face a double penalty: income taxes on the withdrawn amount and a 10% early withdrawal penalty from the IRS. ROBS offers a way around this penalty.

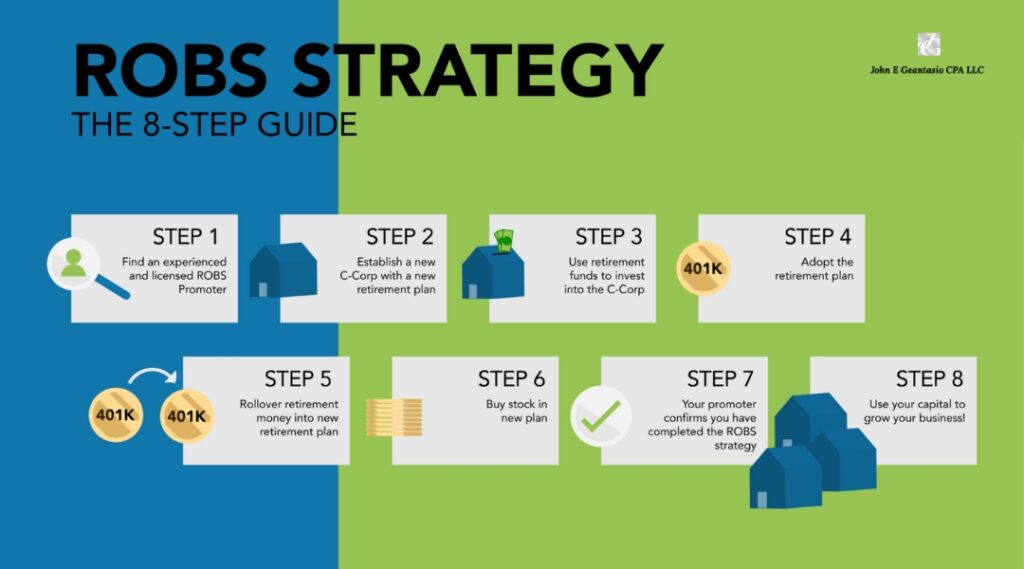

Here’s the step-by-step process:

By following these steps, you can leverage your retirement savings to fund your business venture while still maintaining a tax-advantaged retirement plan for yourself and your employees.

Debt-Free Funding and Easier Access for Startups with ROBS

While traditional business loans can get your company off the ground, they often come with high monthly payments. For example, a typical monthly payment on a $250,000 SBA loan can be $2,775, and an unsecured line of credit can cost even more at $3,881 per month. These significant debt obligations can strain your cash flow, especially during the crucial startup phase. This is where ROBS comes in. By allowing you to use your retirement funds, ROBS helps you finance your business without the burden of debt, giving your startup a vital cash flow advantage.

ROBS also offers easier access to funding for businesses with limited credit history. Unlike traditional lenders who often require a good credit score, ROBS doesn’t have strict credit score requirements. This can be a game-changer for entrepreneurs who may have faced credit challenges in the past. Easier access to capital through ROBS can significantly improve a startup’s chances of achieving profitability sooner. Reaching profitability faster can then open doors to new opportunities such as partnerships, mentorships, and additional funding for future growth.

ROBS: A Surprisingly Beneficial Structure for Your Business

While ROBS is a strategy to access retirement funds for your business, it offers unexpected advantages that go beyond just funding. Here’s how ROBS can positively impact your company’s health and day-to-day operations:

- Stronger Financial Management: ROBS requires your C Corporation to follow strict guidelines set by the IRS and Department of Labor (DOL). This translates to regular meetings with your accountant (quarterly is recommended) to review finances, create business valuations and reports, and file IRS Form 5500 annually. These requirements aren’t just bureaucratic hoops to jump through – they ensure your business is running smoothly financially. The regular reviews with your accountant provide valuable insights and knowledge you can use to make informed financial decisions for your company’s future.

- Retirement Savings for All: The ROBS structure necessitates setting up a retirement plan for all your employees. This is a double win: you can continue saving towards your own retirement while offering an attractive benefit to potential hires. A well-structured retirement plan can be a significant perk for employees, making your company more competitive in the job market.

- Boosting Loan Applications: If you’re considering applying for an SBA loan (or any small business loan for that matter), a large down payment is typically required – up to 30% of the loan amount. The funds you access through ROBS can be used for all or part of this down payment, significantly improving your chances of loan approval. Since only about one-quarter of SBA loan applications are successful, having a sizable down payment can be a major advantage.

ROBS Drawbacks: Consider These Downsides Before You Invest

While ROBS offers a tempting way to fund your startup, there are some important drawbacks to consider. First, unlike a traditional loan, ROBS puts your retirement savings at risk. If your business fails, you could lose all or a portion of the retirement funds you invested. This is a significant risk, as many startups don’t succeed.

Running a ROBS plan also adds complexity to your business operations. The IRS, Department of Labor (DOL), and other regulations require you to administer a retirement plan and meet specific employee eligibility requirements. You cannot simply be a passive investor in your own company; you must be a salaried employee. Failing to comply with these regulations can lead to hefty fines and administrative headaches.

Starting Your Business with ROBS: Advantages and Disadvantages

ROBS, or Rollovers for Business Startups, can be a powerful tool for getting your business off the ground. Here’s a closer look at the benefits and some things to keep in mind:

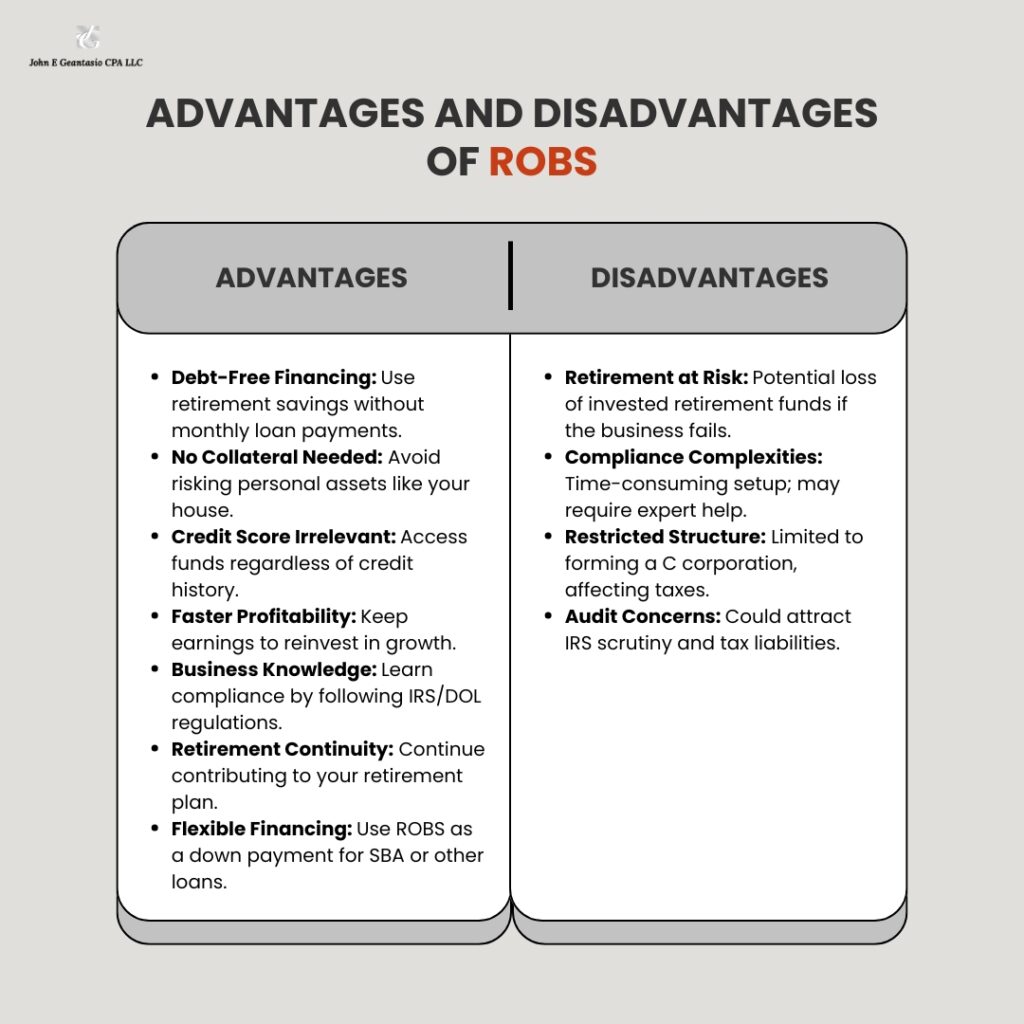

- Debt-Free Financing: ROBS allows you to use your retirement savings to fund your business, without taking on any debt. This means you won’t have monthly loan payments eating into your profits, giving your business a better chance to succeed.

- No Collateral Required: Unlike traditional loans, ROBS doesn’t require you to put up any personal assets like your house as collateral. This reduces the risk involved in starting your business.

- Credit Score Doesn’t Matter: Even if you don’t have a perfect credit score, you can still qualify for ROBS funding. This opens doors for those who might struggle to get a traditional business loan.

- Faster Path to Profitability: By avoiding debt payments, your business can keep more of its earnings. This can help you reach profitability sooner and reinvest those profits back into your company’s growth.

- Gain Valuable Business Knowledge: Setting up a ROBS plan involves following IRS and Department of Labor (DOL) regulations. This process can actually help you gain a deeper understanding of important business compliance requirements.

- Continued Retirement Savings: Even while using ROBS, you can still contribute to your retirement plan. This allows you to keep building your nest egg for the future, while also investing in your business dreams.

- Flexibility with Other Financing: ROBS funds can be used as a down payment for other types of business loans, such as those offered by the Small Business Administration (SBA). This gives you more options for financing your growing company.

While using your retirement savings to fund your business venture (through an ROBS plan) can be an attractive option, it’s important to be aware of the potential drawbacks before you dive in. Here’s a closer look at some key considerations:

- Risk to your retirement: If your business doesn’t take off as planned, you could lose all or part of the retirement funds you’ve invested. Unlike some other forms of financing, this money won’t be readily available to grow again in the stock market.

- Compliance complexities: Setting up and maintaining an ROBS plan involves following specific IRS regulations. This can be a complicated and time-consuming process, so be prepared to invest some effort (or hire professional help) to ensure everything is done correctly.

- Limited business structure: ROBS plans typically restrict you to forming a C corporation as your business structure. This might not be the most suitable option for all businesses, and it can have different tax implications compared to other structures like sole proprietorships or LLCs.

- Potential audit headaches: The complexity of a ROBS plan may raise red flags for the IRS during an audit. This could lead to additional scrutiny and potential tax liabilities.

By carefully weighing these potential downsides, you can make a more informed decision about whether an ROBS plan is the right fit for your business financing strategy. Remember, it’s always wise to consult with a financial advisor to discuss your specific situation and explore all available options.

Frequently Asked Question

Ques. What is ROBS and how does it work?

Ans. ROBS (Rollovers as Business Startups) allows individuals to invest funds from an eligible retirement account into a new or existing business without needing to pay early withdrawal penalties or taxes.

Ques. Is using ROBS for financing a business a safe option?

Ans. While ROBS can be a powerful tool for financing a business, it involves significant risks including the potential complete loss of retirement funds. Consulting with a financial advisor or ROBS expert is crucial.

Ques. What are the legal requirements for setting up a ROBS?

Ans. Setting up a ROBS involves specific legal steps, including establishing a C-corporation, creating a retirement plan under the corporation that can invest in private stock, and rolling over retirement funds into this new plan.

Ques. Are there any penalties or taxes when using ROBS for business financing?

Ans. Typically, if properly executed, ROBS allows individuals to use their retirement funds for business investment without triggering early withdrawal penalties or immediate tax liabilities.

Ques. Can ROBS be used to fund any type of business?

Ans. ROBS can fund various businesses, but the business must be operated as a C-corporation. This structure is essential to comply with IRS and Department of Labor regulations.

Ques. What are the potential downsides of using ROBS?

Ans. The downsides include the risk of losing retirement savings, the costs of setting up and maintaining a C-corporation, and potential scrutiny from IRS and DOL.

Ques. How does ROBS compare to traditional business loans?

Ans. Unlike traditional loans, ROBS does not require monthly repayments or interest payments, which can alleviate financial pressure. However, the risk of losing retirement funds can be higher with ROBS.

Ques. What happens to my retirement funds if the business fails?

Ans. If the business financed through ROBS fails, the invested retirement funds may be lost, which could significantly impact your future financial security.

Ques. How can I set up a ROBS plan?

Ans. Setting up a ROBS plan typically involves working with a specialized ROBS provider who can ensure compliance with all applicable laws and regulations.

Ques. Are there ongoing compliance requirements after using ROBS?

Ans. Yes, businesses using ROBS must maintain compliance with a variety of federal regulations, including annual reporting requirements for the retirement plan and adherence to employee benefits laws.

Also Read – 2024 Income Tax Brackets: Federal Tax Rates and What They Mean for You

How to Pay ZERO TAXES: Tax Loopholes for the Average Taxpayer