Tax-free income is what every taxpayer dreams of, and with a Roth account, that dream can become a reality. Whether you’re saving for retirement or looking for ways to optimize your tax strategy, a Roth IRA offers a powerful way to build a tax-free income stream. Since its introduction in 1998—followed by the Roth 401(k) in 2006—this retirement account has gained popularity for its long-term tax advantages.

As of 2024, you can contribute up to $6,500 per year to a Roth IRA (or $7,500 if you’re over 50), and the best part? You can withdraw your contributions anytime without penalties. However, Roth IRAs come with specific rules that can be tricky to navigate.

If you want to make the most of your retirement savings, understanding how to maximize your Roth IRA benefits is key. In this blog, we’ll break down ten essential points to help you optimize your savings. And if you ever need expert guidance, searching for a CPA near me for taxes can ensure you’re on the right track.

Let’s dive in and simplify your path to a tax-free retirement!

10 ROTH IRA Benefits to help you maximize your retirement planning

1. Pay Taxes Now, Enjoy Tax-Free Withdrawals Later

When it comes to retirement planning, a Roth IRA offers a unique approach to taxes. Instead of the traditional IRA or 401(k) where you get a tax break when you contribute and then pay taxes on withdrawals, a Roth IRA works differently. You contribute after-tax dollars now, and in return, you can enjoy tax-free withdrawals in retirement.

Choosing a Roth IRA means you deal with taxes upfront. This strategy can be particularly beneficial if you expect to be in a higher tax bracket when you retire. By paying taxes at your current rate, you avoid potentially higher taxes later.

For example, if you’re in a 24% tax bracket during retirement, the IRS would take 24% of your traditional IRA withdrawals, including both your contributions and earnings. With a Roth IRA, all the money you withdraw in retirement is yours to keep.

However, the Roth advantage depends on your tax situation. If you are in a lower tax bracket when you retire compared to when you contribute, the immediate tax savings of a traditional IRA might have been more advantageous.

But if you expect your income to grow, making you subject to higher taxes in retirement, a Roth can be a smart move.

2. Roth IRA Contribution Limits for Your Retirement Plan

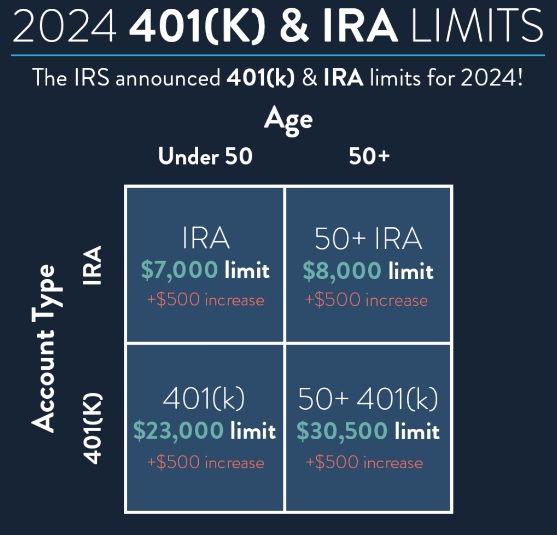

To contribute to a Roth IRA, you must have earned income. For 2024, you can contribute up to $7,000 annually to a Roth IRA, with an extra $1,000 allowed if you’re 50 or older.

You can split contributions between a Roth and a traditional IRA, but the combined total cannot exceed the annual limit.

However, if your income is high, you might not be eligible to contribute to a Roth IRA. For 2024, the ability to contribute begins to phase out if your modified adjusted gross income (MAGI) exceeds $146,000 for single filers or between $230,000 and $240,000 for married couples filing jointly.

Once your income reaches $161,000 for single filers or $240,000 for married couples filing jointly, you can no longer contribute to a Roth IRA.

Remember, you have until April 15, 2024, to make contributions for the 2023 tax year.

3. Explore Your Company’s Roth 401(k) Option

Many employers now offer a Roth option in their 401(k) plans. While contributions to a Roth 401(k) are made with after-tax money, meaning you won’t get an immediate tax break, your investments will grow tax-free. Note that any matching contributions from your employer will go into a traditional 401(k) account, not the Roth.

For 2024, you can contribute up to $23,000 per year to your Roth 401(k). If you’re 50 or older, you can add an extra $7,500 annually. In 2023, the contribution limit was $22,500, with the same catch-up provision for those 50 and older.

It’s important to make your contributions by December 31 to count for the current tax year. Keep in mind, that the contribution limits apply to the combined total of your traditional and Roth 401(k) contributions. Opting for a Roth 401(k) is a smart move if your income is too high to qualify for a Roth.

This way, you can still benefit from tax-free growth, even if a Roth isn’t an option for you due to income limits.

4. Converting a Traditional IRA to a Roth IRA

Converting your traditional IRA to a Roth IRA can open the door to tax-free earnings, but it’s important to understand the details before making the move.

Here are a straightforward tips to help you decide if a Roth conversion is right for you.

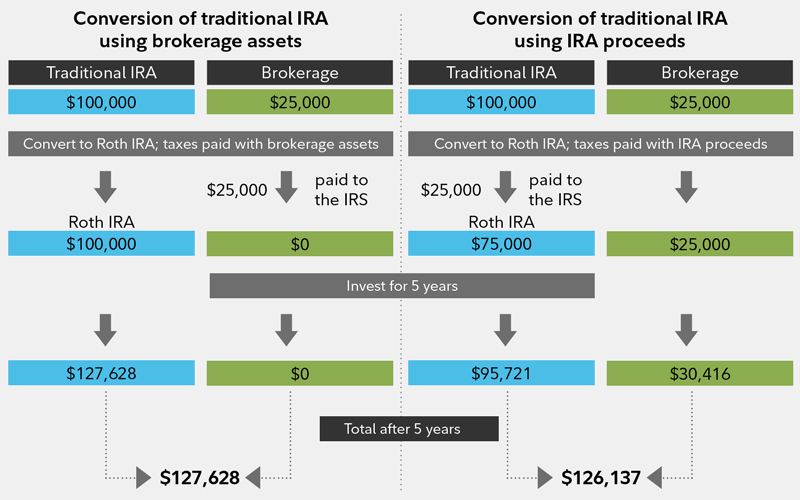

When you convert a traditional IRA to a Roth IRA, you’ll need to pay taxes on the amount you transfer. This upfront tax cost is the trade-off for the benefit of tax-free earnings in the future. If you have contributed to your traditional IRA with after-tax money, part of your conversion might be tax-free.

Consider your future tax rate. If you think your tax rate will be the same or higher when you withdraw from your IRA, converting now could be beneficial. However, if you anticipate a lower tax rate in retirement, a conversion might not be the best move.

It’s best to pay the taxes on your conversion with money outside of your IRA. Using your IRA funds to pay the tax bill can result in additional taxes and possibly a penalty if you’re under 59 1/2.

Before proceeding with a Roth conversion, be aware of potential drawbacks. One major concern is that the conversion could increase your taxable income, which might push you into a higher tax bracket temporarily. This surge in income could also trigger other taxes, such as the 3.8% net investment income tax, commonly known as the Medicare surtax.

To manage your tax bill, consider spreading your conversions over several years. For example, you could convert just enough each year to stay within your current tax bracket.

Always look at the overall impact on your financial situation before deciding on a Roth conversion. If done thoughtfully, it can be a smart strategy for tax-free growth, but it’s crucial to weigh the immediate tax cost against future benefits.

5. Hidden Tax Perks of Roth IRAs

Roth IRAs offer a fantastic tax advantage. They provide you with a pool of tax-free money that can help reduce your overall tax burden.

For example, when it comes to calculating taxes on your Social Security benefits, Roth IRA withdrawals aren’t counted. Similarly, these withdrawals don’t factor into the tax calculations for investment income.

This makes Roth IRAs an excellent tool for keeping your tax bill in check, especially in retirement. By strategically using your Roth IRA, you can enjoy more of your hard-earned money without worrying about unexpected taxes.

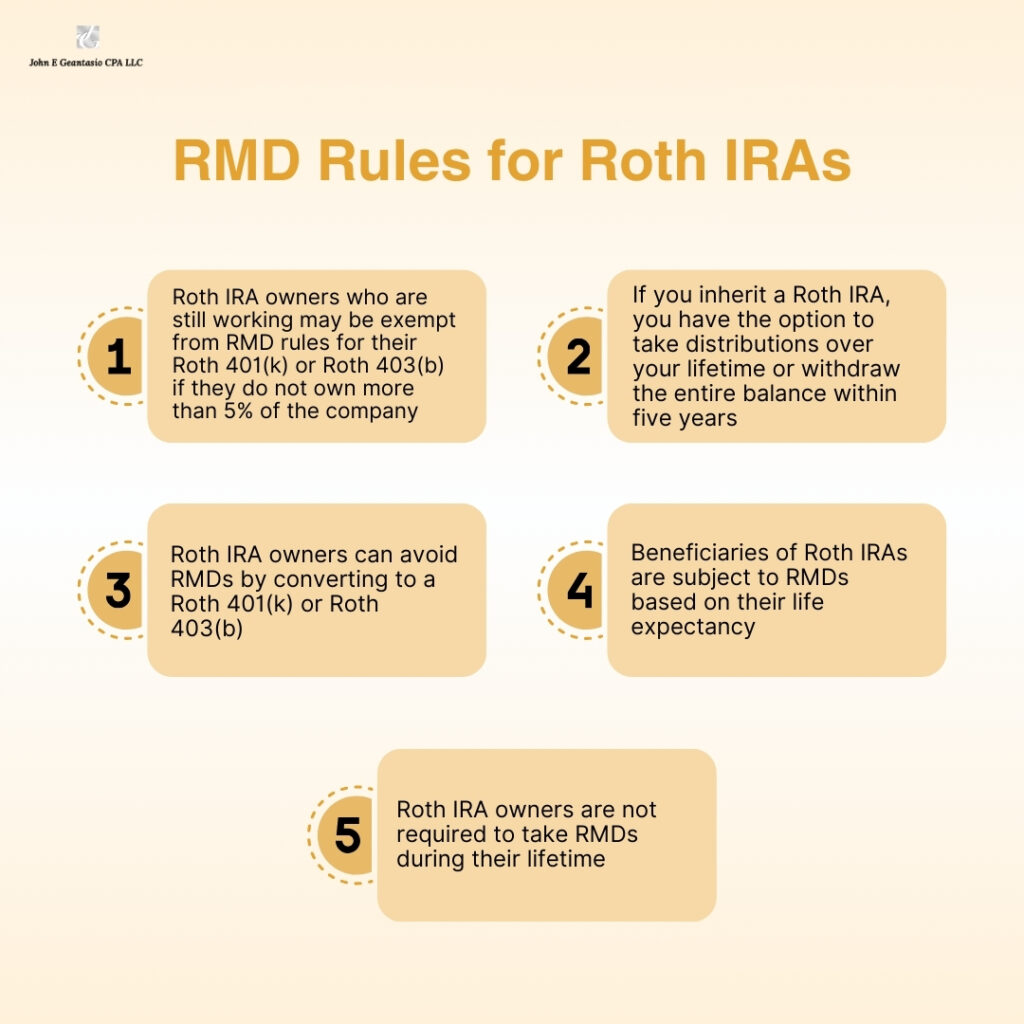

6. Enjoy Flexibility with Roth IRAs: No Required Minimum Distributions

A great benefit of Roth’s are that you aren’t required to take out a specific amount each year, which is known as a required minimum distribution (RMD). This means your money can stay in the Roth IRA, growing tax-free, for as long as you like. This isn’t the case with traditional IRAs and most 401(k) accounts, where RMDs are mandatory.

However, keep in mind that if you inherit a Roth, different rules apply. Starting in 2024, designated Roth 401(k) accounts will also no longer require RMDs, giving you even more flexibility with your retirement savings.

7. Understand Roth IRA Withdrawal Rules (Taxes and Penalties)

If you’re considering taking money out of your Roth IRA, there are specific rules you need to follow to avoid taxes and penalties. Let’s break it down:

Contributions: The money you initially contribute to your Roth IRA can be withdrawn at any time, without any taxes or penalties, no matter your age. This is because you’ve already paid taxes on these contributions.

Earnings: The earnings, or the money your contributions have made over time, have a couple of conditions to be tax- and penalty-free:

- You must be 59 1/2 years old or older.

- Your Roth IRA must have been open for at least five years.

For example, if you open your first Roth IRA at age 58 in 2024, you can start withdrawing earnings without penalties when you turn 59 1/2. However, to avoid taxes on those earnings, you’ll need to wait until 2029.

Conversions:

If you convert money from a traditional IRA to a Roth IRA, you have to wait five years or until you turn 59 1/2, whichever comes first, to withdraw the converted amount without the 10% early withdrawal penalty. This five-year period starts on January 1 the year you make the conversion. So, if you convert late in the year, you might only need to wait a little over four years.

Each conversion starts its own five-year period. For instance, if you convert funds in 2024 and again in 2025, the 2024 conversion can be withdrawn penalty-free in 2029, and the 2025 conversion in 2030.

Order of Withdrawals: When you withdraw money from your Roth (IRA), it comes out in a specific order:

- Contributions: Always tax and penalty-free.

- Conversions: Tax- and penalty-free if you are 59 1/2 or older, or if the converted funds have been in the account for at least five years.

- Earnings: Tax- and penalty-free if you meet both age (59 1/2 or older) and the five-year rule.

This order works in your favour, allowing you to avoid taxes and penalties on withdrawals for as long as possible.

By understanding these rules, you can better manage your IRA (Roth) withdrawals and avoid unnecessary costs.

8. Using Your Roth IRA Before Retirement for Emergencies

Having a Roth IRA offers you a valuable perk: the ability to withdraw money without penalty before turning 59 1/2. This feature provides you with the flexibility to use your Roth funds for various needs beyond retirement savings. For instance, if you face unexpected medical expenses or need to cover your child’s education costs, your Roth IRA can serve as a financial backup.

However, it’s wise to access these funds only when absolutely necessary. When you do need to withdraw money from your Roth IRA before retirement, try to limit it to the contributions you’ve made. This approach helps you avoid taxes and penalties that can occur if you withdraw earnings.

In short, while your Roth IRA is primarily a retirement savings tool, it can also provide a safety net for emergencies. Just remember to use it wisely to maintain your long-term financial goals.

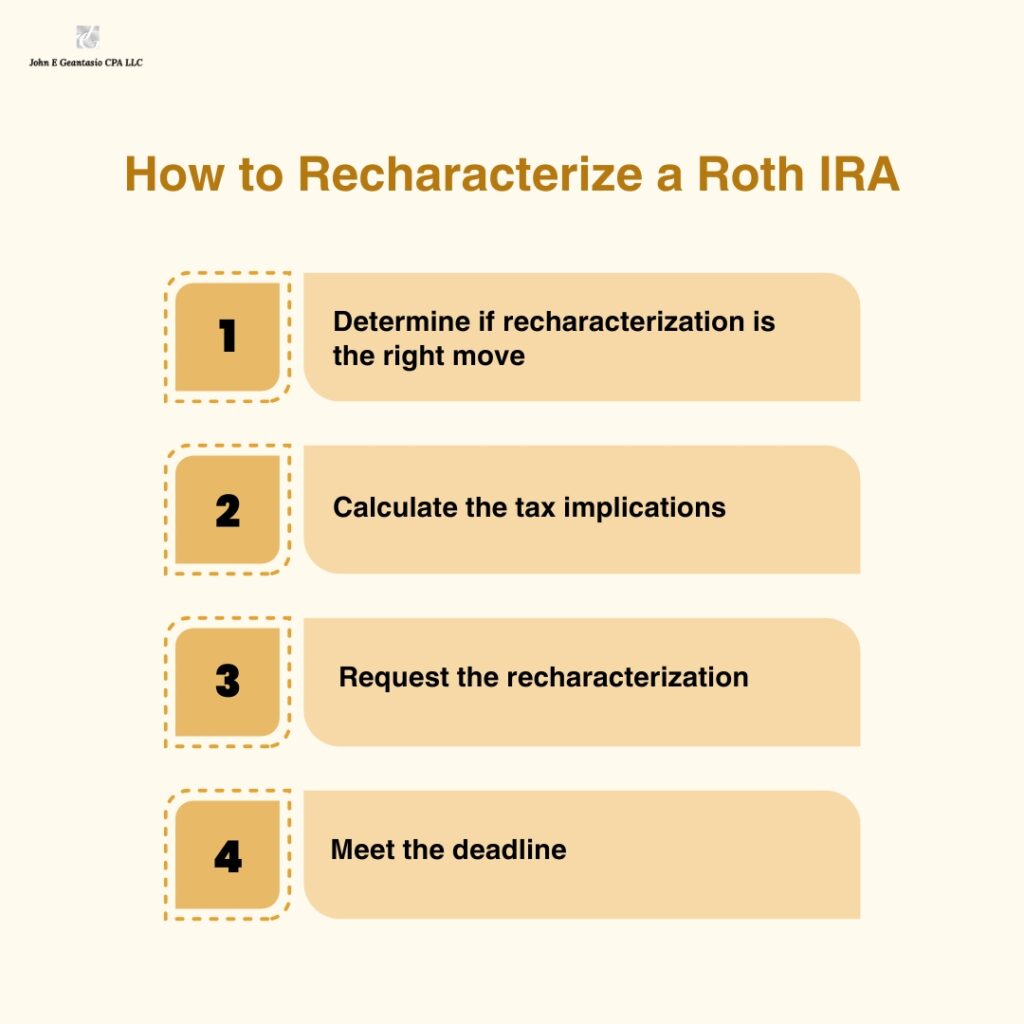

9. Re-characterize Your Annual Roth IRA Contributions

Before 2018, the IRS allowed individuals to reverse a conversion from a traditional IRA to a Roth IRA, a process known as recharacterization. However, the Tax Cuts and Jobs Act of 2017 eliminated this option.

Despite this change, you can still recharacterize all or part of your annual contributions, along with any earnings, between a Roth IRA and a traditional IRA.

For example, if you contribute to a Roth IRA and later realize that your income exceeds the eligibility limit, you can recharacterize that contribution to a traditional IRA, which has no income limits. This flexibility also applies in the reverse; contributions can be recharacterized from a traditional IRA to a Roth IRA.

To complete a recharacterization, the process must be finished by the tax filing deadline for that year, typically April 15th. While recharacterizations are nontaxable, you must report them when you file your taxes.

As of 2024, these rules remain in effect, providing a way to adjust IRA contributions based on your financial situation and eligibility requirements.

10. Roth IRA Can Benefit Your Heirs

One of the great perks of a Roth IRA is that, unlike traditional IRAs, you aren’t required to start withdrawing money at age 72. This means if you don’t need the money, it can keep growing tax-free for the rest of your life.

However, your heirs will need to follow certain rules when inheriting your Roth IRA. They might have to start taking required minimum distributions (RMDs) after your death. The specific rules for these distributions are still being finalized and are expected to be clear by the end of 2024. To ensure your heirs can make the most of your Roth IRA, it’s best to consult a trusted tax professional who can guide them through the process.

In simple terms, a Roth IRA allows your savings to grow tax-free for as long as you live. After your death, there are rules your heirs must follow, but a tax expert can help them navigate these regulations to make the most of your gift.

Wrapping Up

Understanding the nuances of a Roth IRA can make a big difference in your retirement planning. By paying taxes upfront, you can enjoy tax-free withdrawals later, giving you long-term peace of mind. It’s important to stay updated on contribution limits, explore Roth 401(k) options if available, and even consider converting a traditional IRA for potential benefits.

If you need guidance on maximizing your tax advantages, consulting a CPA near me for taxes can help you make informed decisions. A Roth IRA offers flexibility and hidden tax perks that can optimize your retirement savings strategy.

Happy planning, and here’s to a financially secure, tax-free retirement!

Frequently Asked Questions

Ques1. What is a Roth IRA and how does it work?

Ans. A Roth IRA is a type of individual retirement account that allows you to contribute after-tax dollars. Your investments grow tax-free, and qualified withdrawals in retirement are also tax-free. Contributions to a Roth IRA are made with after-tax money, meaning you don’t get a tax deduction for your contributions, but in retirement, you can withdraw your contributions and earnings tax-free if certain conditions are met.

Ques 2. What are the 2024 Roth IRA contribution limits?

Ans. For 2024, the contribution limits for a Roth IRA are $6,500 per year for individuals under 50. For those 50 and older, the limit is $7,500 due to the catch-up contribution provision. However, your ability to contribute depends on your modified adjusted gross income (MAGI).

Ques. 3. How do I qualify for a Roth IRA?

Ans. To qualify for a Roth IRA, you must have earned income, and your MAGI must be below certain thresholds. For 2024, single filers can contribute the full amount if their MAGI is less than $146,000. Contributions phase out between $146,000 and $161,000, and if your income exceeds $161,000, you cannot contribute. For married couples filing jointly, contributions phase out between $230,000 and $240,000.

Ques. 4. What are the differences between a Roth IRA and a traditional IRA?

Ans. The primary difference lies in how and when you get tax advantages:

- Roth IRA: Contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

- Traditional IRA: Contributions may be tax-deductible (pre-tax dollars), but withdrawals in retirement are taxed as ordinary income. Additionally, Roth IRAs do not have required minimum distributions (RMDs) during the account holder’s lifetime, whereas traditional IRAs do.

Ques. 5. Can I have both a Roth IRA and a traditional IRA?

Ans. Yes, you can have both a Roth IRA and a traditional IRA. However, the total contributions to both accounts cannot exceed the annual limit ($6,500 or $7,500 if 50 or older for 2024).

Ques. 6. What are the benefits of converting a traditional IRA to a Roth IRA?

Ans. Converting a traditional IRA to a Roth IRA can be a smart move, especially if you expect to be in a higher tax bracket during retirement. When you convert, you pay taxes upfront on the converted amount, but future withdrawals will be completely tax-free. This strategy can also be beneficial for estate planning since Roth IRAs do not require RMDs, allowing your savings to grow tax-free for a longer period. If you’re unsure whether this move is right for you, consulting a CPA near me for taxes can help you understand the tax implications and make an informed decision.

Ques. 7. Are Roth IRA contributions tax-deductible?

Ans. No, Roth IRA contributions are not tax-deductible. Contributions are made with after-tax dollars, meaning you do not receive a tax deduction for them. However, qualified withdrawals in retirement are tax-free.

Ques. 8. What are the Roth IRA withdrawal rules?

Ans. You can withdraw your Roth IRA contributions at any time without taxes or penalties since contributions are made with after-tax dollars. To withdraw earnings tax-free, you must be at least 59 1/2 years old, and your Roth IRA must have been open for at least five years. Withdrawals that do not meet these criteria may be subject to taxes and penalties.

Ques. 9. How can I avoid penalties on Roth IRA withdrawals?

Ans. To avoid penalties on Roth IRA withdrawals, follow these guidelines:

- Withdraw only your contributions, which are always penalty-free.

- Wait until you are at least 59 1/2 years old and the account has been open for at least five years to withdraw earnings tax-free.

- Use withdrawals for qualified expenses such as a first-time home purchase (up to $10,000), qualified education expenses, or significant medical expenses.

Ques. 10. Can I contribute to a Roth IRA if I have a 401(k)?

Ans. Yes, you can contribute to a Roth IRA even if you have a 401(k). However, your income level determines your eligibility for Roth IRA contributions. While having a 401(k) doesn’t directly impact your ability to contribute, it may affect your Modified Adjusted Gross Income (MAGI), which is used to determine eligibility. If you’re unsure about your contribution limits or need personalized tax advice, consider consulting a CPA near me for taxes to ensure you’re making the best financial decisions.

Also Read-

The Financial Compass for Expansion: Why You Need a Top-Notch Financial Controllers