Selling a rental should feel like victory — not a tax bill.

Yet every year, investors cash out, wire six figures to the IRS, and watch growth money disappear.

It doesn’t have to happen.

Two IRS-approved tools — the 1031 exchange and cost segregation — let you keep that capital working, defer taxes, and scale into bigger, stronger assets.

Let’s unpack how the best investors do it.

Part 1 — The 1031 Exchange: Sell Smart and Keep Everything Working

A 1031 Exchange lets you sell an investment property and defer capital-gains and depreciation-recapture taxes by rolling every dollar into another property of equal or greater value.

It isn’t a loophole; it’s Section 1031 of the Internal Revenue Code — and it’s designed to reward reinvestment.

| Step | Timeline | What to Do |

| 1. Sell your property | Day 0 | Proceeds go to a Qualified Intermediary (QI) — never your bank account. |

| 2. Identify replacements | By Day 45 | List up to 3 properties (or more under 200 % Rule). |

| 3. Close on one | By Day 180 | Finish purchase on any identified property. |

| 4. Match value + debt | By closing | Buy equal or greater value and replace debt/equity to avoid “boot.” |

Do this right and you defer all immediate tax.

Real-World Example

A client sold a 12-unit for $2.2 million, realized $1.1 million gain and $280 k in prior depreciation.

Without planning: ≈ $400 k taxes.

With a 1031: moved into a $3.1 million 24-unit, no boot, no tax bill. More doors. Better cash flow. Zero haircut.

Why 1031 Exchanges Matter in 2025

Higher rates and tight capital make every dollar count. Savvy investors now:

- Trade one large asset for several smaller cash-flowing ones.

- Consolidate multiple headaches into a newer property with stable tenants.

- Use reverse exchanges (buy first, sell later).

- Roll renovation funds into a replacement through an improvement exchange.

Plan early and the calendar works for you, not against you.

Part 2 — Cost Segregation: The Hidden Tax Accelerator

If a 1031 lets you defer tax, cost segregation lets you reduce it today.

Together they’re how you grow tax-efficiently year after year.

What Is Cost Segregation in Simple Terms?

It’s a method of breaking your property into parts that wear out at different speeds.

Instead of depreciating the whole building over 27.5 or 39 years, you reclassify items like carpet, lighting, plumbing, and parking lots into 5-, 7-, and 15-year categories.

That accelerates deductions and cuts this year’s tax bill.

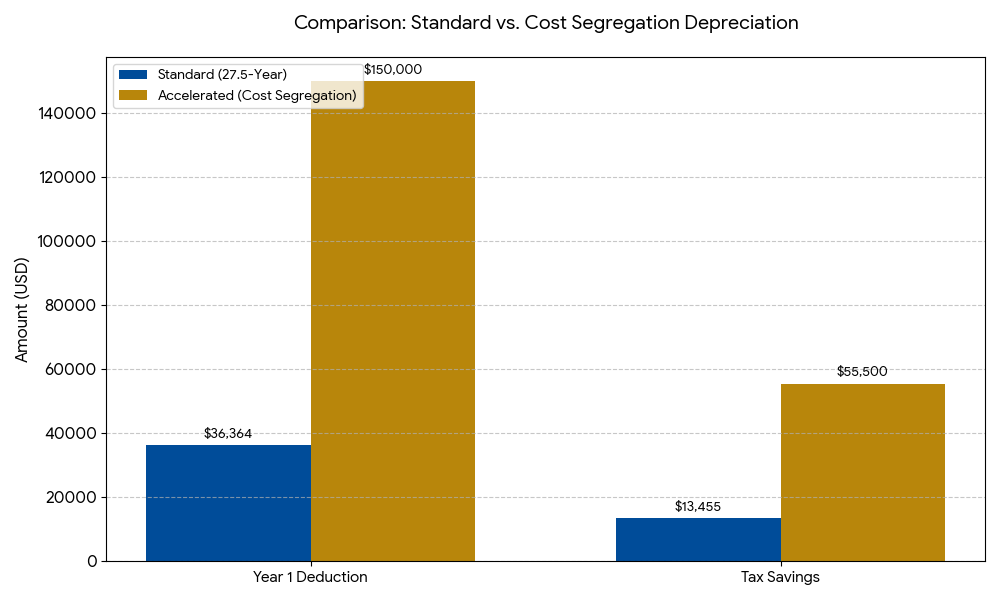

Quick Math

| Scenario | Year 1 Deduction | Tax Saved (37 %) |

| Regular 27.5-year Depreciation | $43 k | $16 k |

| Cost Segregation Study | $420 k | $155 k |

Same property. Same IRS rules. Different timing.

What Is Cost Segregation in Real Estate?

It’s an IRS-approved engineering study that identifies short-life assets inside your property so you can depreciate them faster.

You get bigger deductions now and stronger cash flow to reinvest.

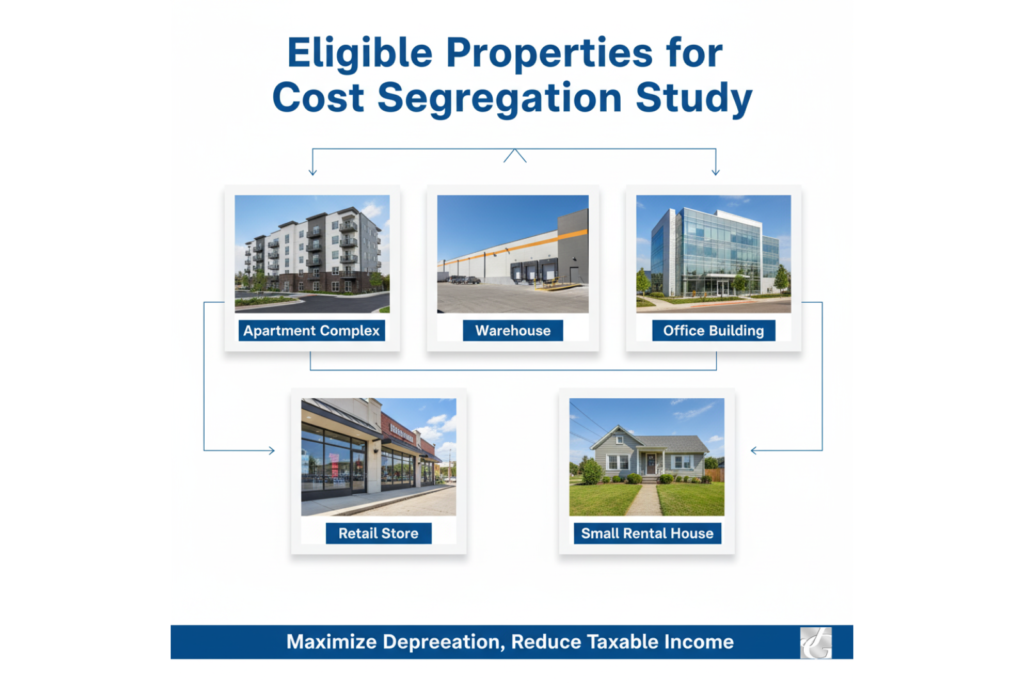

What Type of Property Is Best for Cost Segregation?

- Multifamily and rental homes

- Office, retail, industrial buildings

- Hotels and storage facilities

- Any property over ≈ $500 k improvement value

Even short-term rentals qualify if used for income.

Cost Segregation for Dummies (Plain Analogy)

Your building is a basket of stuff.

Some items last 5 years, others 30. Why wait 30 years to deduct something that dies in 5? Cost seg is just sorting that basket and writing off the fast-wearing items now.

What Is a Cost Segregation Tax Study?

A licensed engineer documents every component, then a CPA maps it to IRS life classes (Pub 946).

You get a full report with:

- 5-, 7-, 15-year asset lists

- Audit-ready work papers

- Bonus depreciation eligibility analysis

We merge it directly into your Form 4562 and books.

What Is Bonus Depreciation and How Does It Work With Cost Segregation?

Bonus depreciation lets you deduct a large percentage of qualified property in the first year (60 % for 2025, phasing down).

When combined with cost segregation, it turbo-charges the effect by front-loading even more deductions.

Example: That $420 k in 5-year property? Bonus rules let you write off 60 % of it immediately — an extra $252 k deduction.

What Is the Downside of Cost Segregation?

- Depreciation Recapture: If you sell without a 1031, part of your gain is taxed at 25 %. Plan exits to defer it.

- Study Cost: $5 k–$15 k for most properties, but ROI is usually 5×–20× in tax savings.

- Complexity: Needs professional integration with your tax return — that’s where we come in.

How Does Cost Segregation Help With Taxes?

It creates paper losses that offset rental or even active income (if you qualify as REPS or under STR rules).

Lower taxable income = lower taxes = more cash for growth.

Cost Segregation Calculator and ROI Example

We estimate benefits using purchase price, land value, and tax rate.

| Building Value | First-Year Deduction | Tax Savings | Study Cost | ROI |

| $1 M | ≈ $300 k | ≈ $111 k | $8 k | ≈ 13× return |

| $2 M | ≈ $600 k | ≈ $222 k | $10 k | ≈ 22× return |

We can run this “pre-fit ROI check” in 48 hours so you see real numbers before ordering a study.

Can Cost Segregation Trigger an IRS Audit?

No — when done right.

The IRS Audit Techniques Guide (Pub 5653) lays out acceptable methods.

We follow that line-by-line, and every figure ties to your return.

In fact, a proper study reduces audit risk by documenting facts instead of estimates.

What Is Depreciation Recapture and How Do You Avoid It?

When you sell, the IRS “recaptures” depreciation as taxable gain (up to 25 %).

You avoid or delay it by:

- Using a 1031 exchange to roll into another property.

- Holding until death — heirs get a step-up in basis and the tax disappears.

- Planning recapture timing to match lower-income years.

Depreciation recapture is a timing issue, not a penalty.

How Does Cost Seg Work With 1031 Exchanges?

When you exchange, your basis carries over into the new property.

We apply cost seg after the purchase to reset depreciation on new improvements, while your old basis keeps rolling forward tax-deferred.

That’s how you keep the compounding engine running indefinitely.

Can You Do Cost Segregation on a Short-Term Rental?

Yes. If your average stay is 7 days or less and you actively manage it, you can often use losses against other income.

Many Airbnb owners are saving five figures annually this way.

When Is the Best Time to Do a Cost Seg Study?

- Immediately after purchase to claim bonus depreciation.

- After a major renovation.

- Any time you realize your CPA never adjusted for improvements — you can file Form 3115 and “catch up” missed depreciation in the current year.

We’ve used that catch-up rule to deliver $50 k–$250 k deductions without amending old returns.

Can I Combine Cost Seg With Bonus Depreciation and REPS Status?

Yes — that’s the triple stack.

Cost seg accelerates deductions; bonus depreciation pulls them into year one; REPS lets you use those losses against active income.

Used together, they can zero out entire tax liabilities legally.

How Does Investing in Real Estate Save Taxes Overall?

Real estate combines six advantages: depreciation, cost seg, 1031 deferral, expense deductions, interest write-offs, and step-up in basis.

That’s why the wealthy hold assets — not just income.

| Tax Tool | Purpose | Result |

| Depreciation | Annual non-cash deduction | Lowers taxable income |

| Cost Seg + Bonus | Front-loads deductions | Immediate cash savings |

| 1031 Exchange | Defers gains + recapture | Keeps equity intact |

| Interest & Expenses | Write off operations | Boosts ROI |

| Step-Up Basis | Resets for heirs | Eliminates old tax liability |

Part 3 — Bringing It All Together

- Sell your property through a 1031 Exchange.

- Buy a larger asset with the rolled equity.

- Run a cost segregation study on the new property.

- Use bonus depreciation to supercharge the first-year write-off.

- Repeat each time you trade up.

The result? Tax-deferred growth compounding for decades.

How We Do It at John Geantasio CPA LLC

We engineer strategy around your assets so you never leave money on the table.

- Pre-Sale Modeling: Value, gain, recapture, and exchange path.

- Engineer Partnership: Qualified cost-seg firms with IRS-ready reports.

- Tax Integration: We align study data to Form 4562 and bookkeeping.

- Cash-Flow Forecasting: We map deductions to renovation and refi timelines.

- Exit Planning: Recapture vs 1031 vs estate deferral — your choice, modeled before closing.

This isn’t data entry. It’s cash-flow architecture.

Part 4 — Common Concerns (Answered Briefly)

What if my CPA never mentioned this?

It’s common. Most general CPAs focus on compliance, not engineering. That’s our lane.

Can I do this for properties I already own?

Yes — use Form 3115 for a catch-up deduction. We’ve done it for properties purchased 5–10 years ago.

How long does a study take?

Usually ,4–6 weeks from inspection to report. We coordinate everything with your lender and bookkeeper.

Will this affect my loan underwriting?

No. Your books show non-cash deductions; lenders look at NOI and DSCR, not taxable income.

The Bottom Line

Paying tax on growth is optional when you understand the rules.

The 1031 Exchange lets you defer taxes when you sell.

Cost Segregation lets you reduce taxes while you own.

Used together, they form the backbone of how smart real-estate investors build wealth that grows tax-deferred, multiplies cash flow, and compounds faster than almost any other asset class.

When you understand how depreciation, timing, and reinvestment work together, you stop playing defense with your taxes — and start playing offense with your money.

The Long Game: Why These Strategies Matter

The biggest difference between investors who build generational wealth and those who just “flip for profit” isn’t luck.

It’s strategy and timing.

Every time you use a 1031 Exchange, you’re letting your equity snowball without interruption.

Every time you use Cost Segregation, you’re pulling next year’s deductions into today — funding your next project with money the IRS said you could keep.

Do this over multiple cycles and your taxes don’t just go down; your portfolio velocity goes up.

That’s why our firm’s motto is simple:

Don’t pay more tax. Design smarter timing.

When to Start Planning

- Before you sell. A 1031 fails most often because planning starts after escrow opens.

- Right after you buy. A Cost Segregation study delivers the biggest punch in year one.

- Before you renovate. Improvements often qualify for separate depreciation lives — don’t let your contractor close that window.

- Before year-end. Bonus depreciation percentages phase down annually; missing December can cost you five figures.

The earlier we plan, the more options you keep.

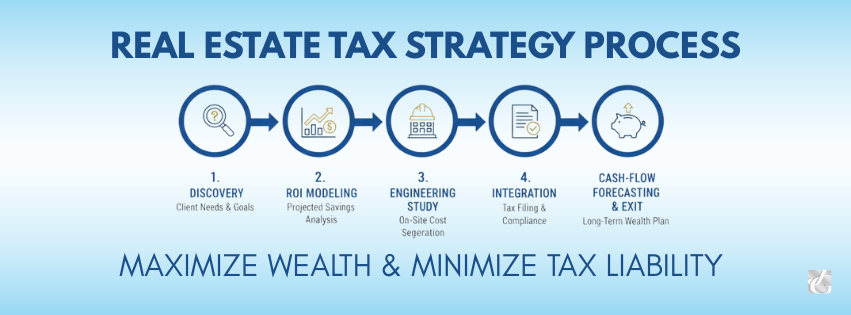

Our Process at John Geantasio CPA LLC

When investors come to us, they usually have two goals: keep cash in motion and stay audit-proof.

We built our system to do exactly that.

- Discovery & ROI Modeling – We review your current returns, fixed-asset schedules, and property list. You’ll see potential 1031 and Cost Seg benefits in plain dollars.

- Pre-Fit Analysis – Using your address and closing data, we estimate first-year deductions within 48 hours.

- Engineering & Compliance – We coordinate a licensed Cost Seg firm, then integrate results directly into your depreciation ledger.

- Cash-Flow Forecast – You’ll know exactly how deductions shift your quarterly estimates and free capital for reinvestment.

- Exit & Estate Strategy – When you’re ready to sell or transfer assets, we model recapture, deferral, or step-up outcomes so you choose what wins long term.

The result? A multi-year tax cash-flow arc that funds your next deal — not the government’s.

Final Thoughts: Keep What You Earn

The IRS wrote both rules — Section 1031 and accelerated depreciation — to encourage reinvestment, construction, and long-term ownership.

They were never meant to be “loopholes.” They’re incentives for doing exactly what entrepreneurs already do: build.

You don’t need a bigger property first.

You need a smarter plan that makes each property work harder for you.

So before you list your next building or start your next renovation, ask yourself one question:

Am I giving the IRS a tip — or am I keeping that money in my next deal?

Book Your Free Strategy Session

Schedule a free 30-minute, no-obligation Tax Strategy Call with John Geantasio.

- Map your 1031 Exchange timeline

- Estimate Cost Seg and bonus-depreciation savings

- Build a clear plan to compound your capital — tax-efficiently

No jargon. No sales pitch. Just clarity and cash-flow math that pays back.

Key Takeaways

- A 1031 Exchange defers capital-gains and recapture taxes when you reinvest in equal or greater property.

- Cost Segregation accelerates depreciation so you claim deductions now, not decades later.

- Combine both and your money compounds, untaxed, through each new acquisition.

- Always plan before closing — the IRS rewards preparation, not panic.