Retirement should be about enjoying the income you worked decades to earn — not being surprised by unexpected taxes on your Social Security benefits.

At the federal level, Social Security can be taxable depending on your income. At the state level, however, the rules vary widely.

The good news?

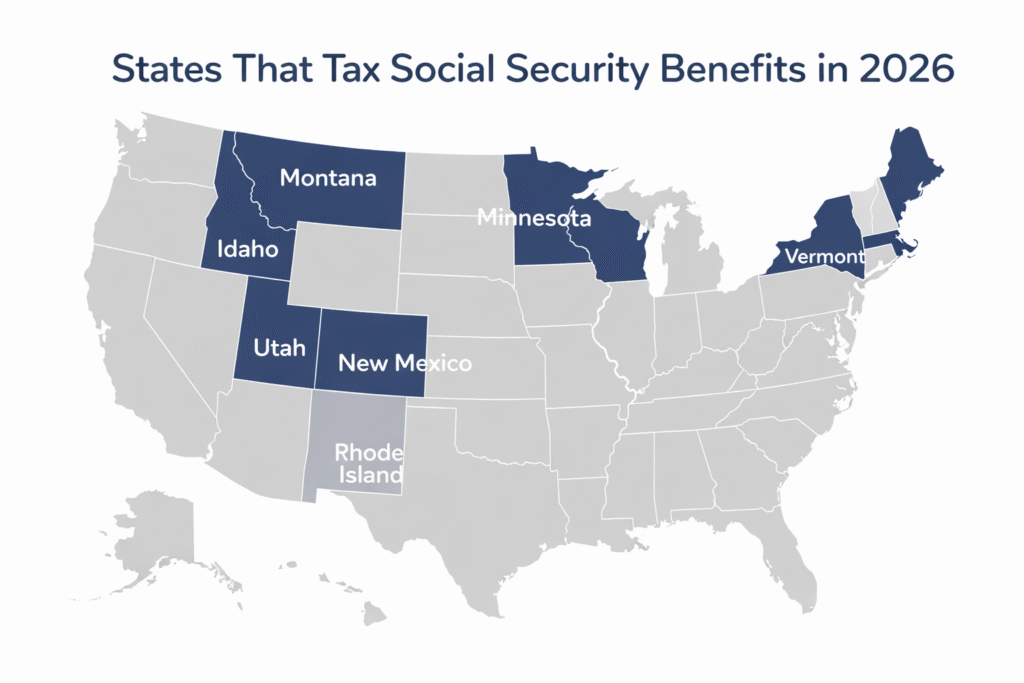

As of 2026, only eight states still tax Social Security benefits.

West Virginia has fully eliminated its tax on Social Security starting in 2026, reducing the list from nine states in prior years.

If you live in one of the remaining states, understanding the rules can help you plan strategically and protect more of your retirement income.

How Social Security Benefits Are Taxed in 2026

Federal Tax Rules

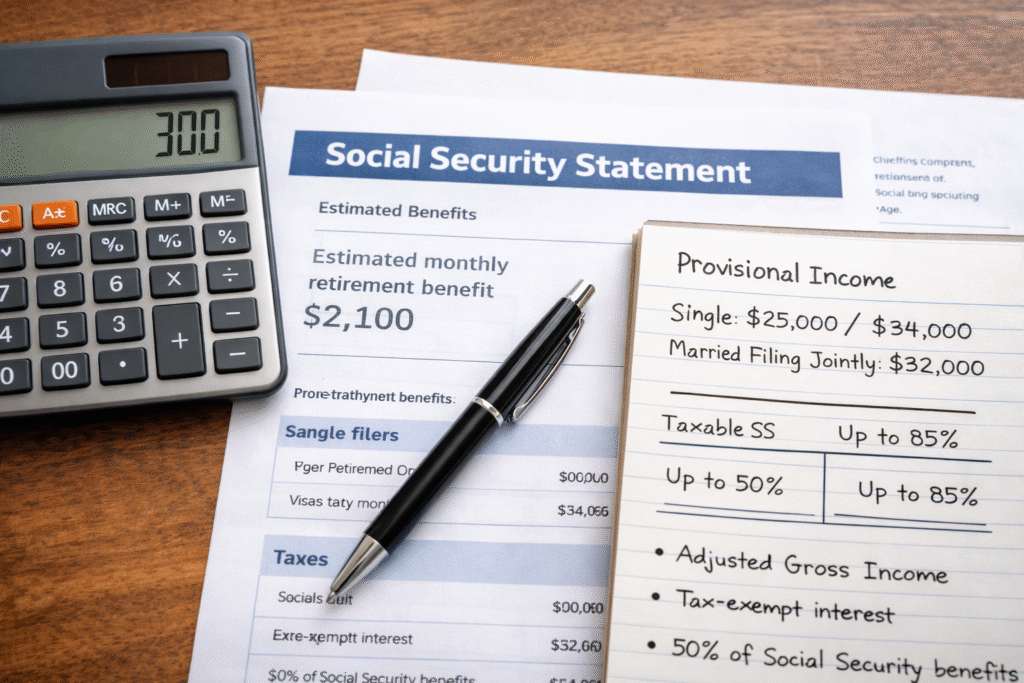

At the federal level, Social Security benefits are taxed based on your provisional income, which includes:

- Adjusted Gross Income (AGI)

- Tax-exempt interest

- 50% of your Social Security benefits

Federal Income Thresholds:

Single Filers

- Over $25,000 → Up to 50% taxable

- Over $34,000 → Up to 85% taxable

Married Filing Jointly

- Over $32,000 → Up to 50% taxable

- Over $44,000 → Up to 85% taxable

These thresholds are not indexed for inflation and remain the same in 2026.

States That Tax Social Security Benefits in 2026

As of 2026, the following eight states still tax Social Security benefits in some form:

- Colorado

- Connecticut

- Minnesota

- Montana

- New Mexico

- Rhode Island

- Utah

- Vermont

West Virginia has fully phased out its Social Security tax starting in 2026.

Each of the remaining states applies different exemptions, credits, and income-based thresholds.

Let’s review each one.

1. Colorado

Colorado applies a 4.4% flat income tax rate in 2026.

However, retirees may deduct:

- Up to $24,000 of retirement income if age 65 or older

- Up to $20,000 if ages 55–64

For many retirees, this deduction fully offsets Social Security income, meaning no state tax is owed.

If retirement income exceeds those limits, the excess is taxed at 4.4%.

Planning Tip: Many retirees in Colorado owe little or no tax on Social Security, but higher-income households may still see exposure

2. Connecticut

Connecticut offers full exemptions for Social Security benefits if your AGI is below:

- $75,000 (Single)

- $100,000 (Married Filing Jointly)

Above these thresholds, up to 25% of benefits may become taxable.

Connecticut’s approach creates a middle ground: moderate-income retirees pay nothing, while higher earners face partial taxation

3. Minnesota

Minnesota taxes Social Security benefits but allows a subtraction:

- Up to approximately $4,560 (Single)

- Up to approximately $5,840–$9,000 (Married), depending on income levels

This subtraction phases out at higher income levels.

If phased out, federal rules apply and up to 85% of benefits may be taxed at Minnesota’s progressive rates (which range up to 9.85%).

Minnesota remains one of the less retirement-friendly states from a tax standpoint.

4. Montana

Montana largely follows federal taxation rules.

Up to 85% of benefits may be taxable depending on provisional income.

Montana’s top state income tax rate is 5.9%.

Some limited retirement deductions may apply, but there is no full exemption specifically for Social Security benefits.

5. New Mexico

New Mexico provides full exemption for Social Security benefits if AGI is below:

- $100,000 (Single)

- $150,000 (Married Filing Jointly)

Above those thresholds, benefits may be taxed as regular income under New Mexico’s state income tax rates.

Middle-income retirees often avoid taxation, but higher-income households should plan carefully.

6. Rhode Island

Rhode Island exempts Social Security benefits if AGI is below:

- $95,800 (Single)

- $119,750 (Married Filing Jointly)

Above those limits, benefits are taxed at rates ranging from 3.75% to 5.99%.

Small income adjustments can determine whether benefits are fully exempt or partially taxable.

7. Utah

Utah applies a 4.55% flat income tax rate in 2026.

However, Utah offers a Social Security tax credit:

- Full credit if income is below $45,000 (Single)

- Full credit if below $75,000 (Married Filing Jointly)

The credit phases out at higher income levels.

Many moderate-income retirees pay little to no state tax after credits are applied.

8. Vermont

Vermont exempts Social Security benefits if income is below:

- $50,000 (Single)

- $65,000 (Married Filing Jointly)

Partial exemptions apply at slightly higher income levels.

Above those thresholds, Vermont follows federal taxation rules and applies state tax rates that range from 3.35% to 8.75%.

Vermont remains one of the less tax-friendly states for higher-income retirees.

West Virginia

West Virginia previously taxed Social Security benefits but has fully phased out the tax beginning in 2026.

As of tax year 2026, Social Security benefits are completely exempt from West Virginia state income tax.

This reduces the total number of taxing states from nine to eight.

What This Means for Retirement Planning in 2026

State taxation can materially impact retirement cash flow.

However, relocating solely for tax reasons is rarely the only factor to consider. Healthcare access, cost of living, estate taxes, and overall income structure all matter.

In many cases, careful income planning — such as managing IRA withdrawals, Roth conversions, or capital gains timing — can reduce or eliminate state Social Security taxation without changing residency.

Bottom Line

As of 2026, only eight states tax Social Security benefits.

But “taxed” does not always mean “fully taxed.”

Most of these states provide income-based exemptions, credits, or phaseouts.

Retirement tax planning is no longer just about federal rules — state taxation plays a critical role in protecting your income.

Before making major financial or relocation decisions, review your income structure carefully.

Strategic planning can often preserve more of your Social Security benefits — without drastic lifestyle changes.