You run a property management company. You work hard — juggling tenants, maintenance, utilities, leasing, eviction, the works. What if you could keep more of that income instead of handing it over to Uncle Sam?

Many property managers and landlords miss out on legitimate tax-savings because they don’t know how the rules apply to property income, management fees, structure and losses.

This blog walks you through IRS-approved strategies for property management companies and landlords. By the end, you’ll know how to use depreciation, structure your activity, choose entity types and stay compliant — so you legitimately reduce tax, not fall into traps.

If you partner with a skilled tax professional (like John, your specialist), you’ll be better positioned to apply these strategies safely.

1. How Property Management Companies & Landlords Earn Money

Before we dive into strategies, let’s clarify how property management firms and landlords typically make money. That matters — because how you earn affects how the IRS views your deductions.

- You collect rent from tenants.

- You may charge a property management fee (for managing the property, handling repairs, tenant screening).

- You might also earn ancillary income (late-fees, service charges, vending machines, parking, etc.).

- Some companies manage properties owned by others; some own the properties themselves.

Question: What kind of property manager makes the most money?

Usually, the property manager who:

- Manages a large portfolio of units (higher scale)

- Offers value-added services (maintenance oversight, tenant screening, tech, premium amenities)

- Controls overhead (efficient staff, outsourcing smartly)

- Keeps occupancy high and turnover low

From a tax-saving view, the manager who structures income and expenses well, tracks everything, and uses tax-savvy tools often keeps the most. For example: if two companies each draw $1 million in gross income, but one deducts 40 % of its income in expenses and depreciation (i.e., $400,000) whereas the other deducts only 25 % (i.e., $250,000), the first company has $150,000 more taxable income — meaning tens of thousands more tax paid. Scale + tax planning = bigger after-tax profit.

2. Setting the Tax Foundation

To save tax, you must correctly report your income and know the rules for expenses, depreciation and losses. The following are foundational steps.

2.1 Report Rental Income

The IRS’s Publication 527 (2024 version) covers rental income and expenses for residential rental property.

Key points include:

- You must report all rental income — standard rent, advance rent, lease cancellations, amounts paid by tenants for services, etc.

- Advance rent must be included in the year received, even if it covers future periods.

- If you rent fewer than 15 days and meet specific conditions, different rules may apply — though this is less typical for full-time property managers.

- Use the correct form — often Schedule E (Form 1040) for many rental properties.

2.2 Correct Forms & Record-Keeping

- Precisely tracking all income and expenses is important — IRS guidance stresses the need for good records.

- In Publication 527 there’s a chapter on “How To Get Tax Help” and pointers for special rental situations.

- Without good documentation, you risk adjustments or penalties.

Getting this foundation right means you can legitimately reduce taxable income rather than simply guessing deductions.

3. Major Tax-Saving Strategies for Property Management Firms & Landlords

Now we hit the heart of the blog: how your property-management business and landlords you serve can put tax-savings to work — all while staying IRS-compliant.

Deducting Operating Expenses

One of the most direct ways to reduce taxable income is by deducting valid expenses.

- Publication 527 says you can deduct “ordinary and necessary” expenses: maintenance, utilities, insurance, advertising, management fees, repairs.

- Distinguish repairs (deduct in the year they occur) vs improvements (capitalised and depreciated). Publication 527 covers that distinction.

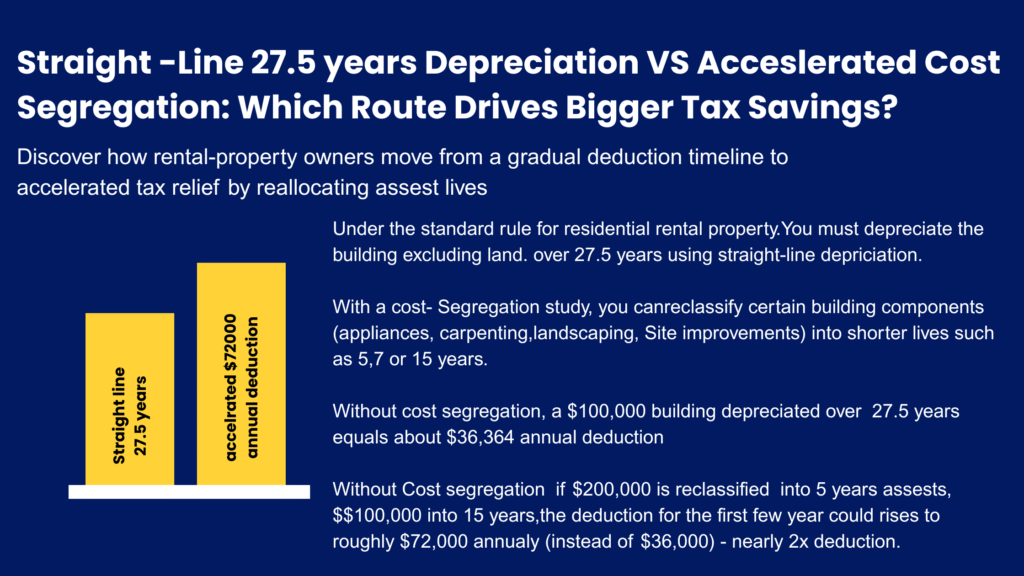

- Depreciation: residential rental property is typically depreciated using the Modified Accelerated Cost-Recovery System (MACRS) over 27.5 years.

- Bonus depreciation: As of the 2024 tax year, the bonus depreciation deduction under Section 168(k) continues its phase-out with the applicable limit reduced from 80 % to 60 %.

Why this matters

If your management company owns a property worth $1,000,000 (land excluded), 1/27.5th is about $36,364 of annual depreciation you can deduct — which at a 24 % tax bracket saves you approximately $8,700 in tax that year just by timing. If you apply bonus depreciation (60 % allowable) in initial year, you might front-load a $600,000 deduction — huge impact.

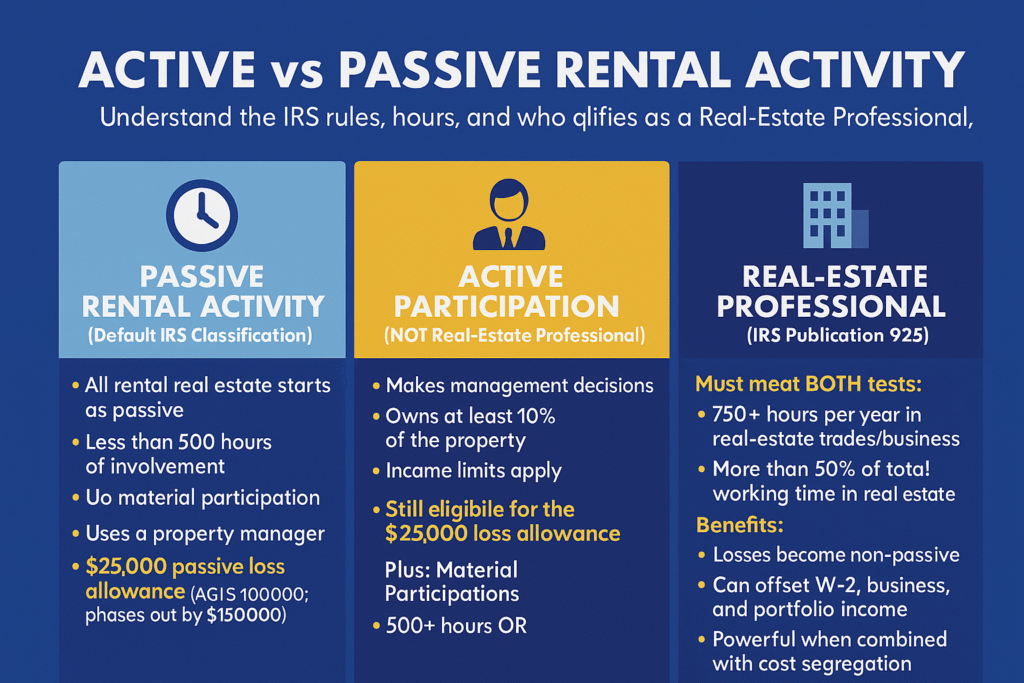

Structuring Active vs Passive Rental Activities

Many rental activities default to “passive” under the law, which limits how losses can offset other income. The IRS’s Publication 925 (2024) explains these rules.

- By default, rental real estate is a passive activity and losses may be limited.

- However, if you qualify as a real estate professional (REPS) and materially participate, your rental activity can be treated as non-passive — which means you may use rental losses to offset other non-rental income.

- Criteria typically: more than 50 % of your personal services working in real property trades/business in the tax year, and more than 750 hours of participation.

Why this matters for a property management company:

If your company (or you) meet these rules, you could treat rental operations as an active business — unlocking full deductions, offsetting other income, and improving tax results. For example: If you have $200,000 of non-rental income and $100,000 rental loss, and you are passive, you may be limited. But if active, you could offset the entire $100,000 against the $200,000 — saving tax at maybe 24 % (i.e., $24,000).

3.3 Entity Structure & Qualified Business Income (QBI) Deduction

While the 20 % qualified business income (QBI) deduction under IRC § 199A doesn’t apply to all rentals, it may apply if your rental/management business qualifies as a “trade or business.”

- To get QBI, your business must provide services and must rise to trade or business level.

- Example: If your property management company grosses $500,000 and qualifies, 20 % of QBI (after wages & capital) might yield up to $100,000 of potential deduction (subject to income thresholds).

- Note: This is complex and you should work with John (your tax pro) on this.

Cost Segregation & Bonus Depreciation

For properties that your management company owns or refurbishes:

- Cost segregation splits components into 5-, 7-, 15–year categories instead of standard 27.5 or 39 years — accelerating depreciation.

- Although Pub 527 doesn’t fully outline cost segregation, it covers depreciation basics which must be observed.

- Bonus depreciation (60 % for 2024) enables substantial deduction in first year. Example: On a $2 million property, if $500,000 is allocated to fast-life assets, 60 % bonus = $300,000 immediate deduction.

Reducing Property Tax & Other Local Relief

While state/local property tax is outside IRS’s direct control, you can still handle it efficiently:

- Under Publication 527, property taxes paid on rental property are deductible rental expenses.

- At the local level: appeals, abatements, exemptions can reduce assessed value — maybe by 5-30 % depending on jurisdiction and appeal success.

- By reducing property tax liability and then deducting what’s paid, you improve your after-tax return.

Capital Gains & Exit Strategy

When you sell rental property you manage/own:

- Depreciation recapture must be reported and taxed (up to 25 % federal rate) plus capital gains on the remainder.

- A like-kind exchange (1031) may defer the gain if eligible. Publication 527 mentions this possibility.

- Example: You sell a property with $300,000 gain, $120,000 depreciation taken. Depreciation recapture portion taxed up to 25 %, say $30,000 tax; remaining gain taxed at say 15 % yields $27,000 tax. Using a 1031 exchange delays this tax entirely.

Tax-Efficient Landlord Strategies

If you’re a landlord (or your property management company also owns properties) these combined strategies can be powerful:

- Use your own company as the manager and pay a market-rate management fee (internal cost shift).

- Accelerate depreciation via cost segregation and bonus depreciation.

- Qualify as a real-estate professional so rental activity is non-passive.

- Choose an entity structure aligned with risk, tax & estate goals (LLC, S-Corp, etc.).

- Track all expenses, document carefully and proactively appeal local property tax.

4. Frequently Asked Questions

Here are answers to the specific questions you provided, with IRS-based context and explanations tailored to property management companies and landlords.

Q1. What kind of property manager makes the most money?

A property manager who combines large volume (many units), high occupancy, value-added services, efficient cost control — and uses tax-savings effectively. From a tax view: one who deducts ~40-50 % of gross income via expenses/depreciation, uses cost segregation, real-estate professional status, and structured entity. That manager may keep significantly more after tax than one who simply collects rent and deducts basic expenses.

Q2. What is the most tax-efficient way to be a landlord?

From IRS rules:

- Treat your rental as a business (if you qualify) so you may offset other income.

- Use depreciation (Publication 527) to reduce taxable income.

- Ensure expenses are fully deductible (maintenance, management fees).

- Consider entity structure and cost-segregation.

- Work with a tax professional to structure intentionally.

Q3. What is wealth-management tax?

The IRS doesn’t use “wealth management tax” as a formal term. If you mean how to manage wealth via real estate in a tax-efficient way: treat your property portfolio as part of your business strategy, use depreciation, structure income and entity wisely, plan for succession. But always check with a tax professional.

Q4. How to reduce property tax in the USA?

Property tax is a state/local tax; however, at the federal level: property taxes you pay are deductible as an expense for rental property (see Publication 527)

The reduction strategy: appeal your assessment, apply for local exemptions, invest in improvements that qualify for exemption or defer tax. Example: a successful appeal might reduce assessed value by 10–20 %, saving thousands in tax and enabling better net cash flow.

Q5. What is the 2% rule for property?

This likely refers to obsolete home-office or itemised deduction thresholds (pre-TCJA). The IRS currently does not have a specific “2 % rule” for rental property deduction under Publication 527. Clarify for your client that you don’t rely on a self-named “2 % rule” unless specific local state regulation applies.

Q6. What is the least taxing tax scheme for landlords?

No guaranteed “least taxing scheme” exists under IRS rules. But combining: non-passive classification (real-estate professional), accelerated depreciation (cost segregation + bonus depreciation), fully documented expenses, proper entity structure, and long-term planning tends to yield the lowest effective tax rate. Example: Some savvy landlords may reduce effective federal tax rate on rental profit to 10-12 % (versus ~24-32 %) by heavy depreciation and loss offset in early years.

Q7. Which strategy is most effective for maximizing rental income?

From a tax perspective:

- Controlling expenses (aim for expense ratio under 30-35 % of gross rents)

- Maximising deductible items + depreciation

- Structuring for non-passive status

- Efficient property management (occupancy > 95 %, turnover < 20 %)

Example: If gross rent is $600,000 and expense ratio is 35 % ($210,000) and depreciation allocates $90,000, taxable income is $300,000. If you reduce expenses to 30 % ($180,000) and increase depreciation by cost-seg ($120,000), taxable income drops to $300,000-7k = $230,000 — big savings.

Q8. What is a simple trick for avoiding capital gains tax?

Not a “trick” but a legitimate strategy: use a like-kind exchange (1031) to defer capital gains when selling rental property. Publication 527 mentions the tax-free exchange option.

Example: Selling for $1,000,000 with $400,000 gain might lead to $60,000+ in tax. A properly executed 1031 exchange lets you defer that, keeping that cash working for you.

Q9. What is the most tax-efficient way?

For many landlords/property managers:

- Treat rental as business (active)

- Use cost segregation + bonus depreciation

- Choose right entity

- Offset income via real-estate professional status

- Monitor local/state tax efficiency

Example: A business making $800,000, where you reduce taxable to $500,000 via depreciation and expenses, gives you huge savings vs paying tax on full $800,000.

Q10. How to avoid 40% tax?

If you’re in a higher bracket, you can reduce taxable income via these strategies: high deductible expenses, depreciation, cost segregation, real-estate professional status. While you can’t “avoid” the tax rate entirely, you can reduce taxable income so your marginal bracket (say 35 %) is applied to a smaller base. Example: Pre-strategy taxable income $500,000 taxed at 35 % = $175,000. Post-strategy taxable $350,000 taxed at 35 % = $122,500 — saving $52,500.

Q11. Do property managers file taxes?

Yes. The property management company must report its income (management fees, service charges) on the appropriate business tax return. If the company is owned by you, your personal tax return will reflect distributions, salary, etc. Also, landlords must report rental income and expenses. Publication 527 covers how rental income is reported.

Q12. How are property management fees taxed?

For the property management company: management fees earned are business income, taxed according to business entity tax rules (taxable income less business deductions).

For the landlord: payment of management fees to a third party is a deductible expense (if ordinary/necessary) reducing taxable rental income (see Publication 527).

Ensure you document the management agreement, the fee structure, and keep clear books.

Q13. Does a property management company need a 1099?

If the management company pays independent contractors (e.g., maintenance workers, service vendors) more than $600 in a year, it must issue Form 1099-NEC (or 1099-MISC) to those contractors and file with the IRS. The landlord or the property management company must ensure that vendors are properly classified (employee vs independent contractor) and that 1099 rules are followed (see IRS instructions for Forms 1099-NEC/MISC).

While I didn’t pull a direct IRS publication here, the IRS guidance on independent contractors and 1099 filing is well established.

5. Pitfalls & Audit Triggers

Here are some red lights to watch for:

- Poor documentation: If you can’t show days rented vs personal use, expense receipts, asset classification (repair vs improvement), you risk adjustment by the IRS.

- Misclassifying your activity: Claiming real-estate professional status without evidence of > 750 hours & > 50 % of personal services may invite scrutiny.

- Mis-using cost segregation: If you accelerate too aggressively without a proper study, the IRS may challenge your deductions.

- Ignoring 1099 / independent contractor rules: Paying vendors as contractors but treating them like employees — IRS may reclassify.

- Mixing personal and rental use: If property has personal use days, incorrect allocation may reduce deductions. Publication 527 covers mixed use.

6. Conclusion & Call to Action

- Report all income correctly and keep detailed records.

- Maximise legitimate deductible expenses and depreciation (especially via cost segregation where appropriate).

- Understand passive vs active rental rules and aim for real-estate professional status when feasible.

- Structure your property management company and ownership entity with tax strategy in mind.

- Plan exit strategies (capital gains, like-kind exchange) ahead of time.

If you manage properties — or your company handles properties for others — it’s wise to sit down with a tax professional like John. He can leverage these strategies tailored to your situation, and help you stay fully compliant with IRS rules while keeping more profit in your pocket.

Next Step: Schedule a consultation with John today. Bring your property portfolio summary, recent financials and questions like:

- “Am I a real estate professional under IRS rules?”

- “Can I use cost segregation on my portfolio?”

- “How should I structure my business entity to optimise QBI and depreciation?”

When you combine smart business strategy with these tax-saving rules, you give yourself a serious edge.

Start now — your next tax return could be your best one yet.