Tax strategy is not about shaving a few dollars off your annual return.

For real estate investors in 2026, tax strategy determines whether you build wealth efficiently — or hand over unnecessary profits to the IRS.

With bonus depreciation phasing down, potential TCJA sunset impacts, and continued IRS scrutiny on passive activity losses, this year requires precision. The investors who understand the rules will keep more capital working for them.

Below is your updated 2026 guide to the most powerful tax-saving strategies available to real estate investors today.

1. Depreciation: Still the Most Powerful Tool in Real Estate

Real estate remains one of the only asset classes where you can deduct a “paper loss” while your property appreciates.

Residential property depreciates over 27.5 years.

Commercial property depreciates over 39 years.

This non-cash deduction reduces taxable rental income even when the property produces positive cash flow.

Why It Matters in 2026

Even with bonus depreciation reduced, standard depreciation remains fully intact and continues to be the foundation of real estate tax efficiency.

2. Bonus Depreciation in 2026

Under the post-TCJA phase-down schedule:

- 2023: 80%

- 2024: 60%

- 2025: 40%

- 2026: 20%

- 2027+: Scheduled to phase out (unless new legislation is passed)

As of February 2026, bonus depreciation is limited to 20% of qualified assets placed in service during the year.

This significantly reduces front-loaded write-offs compared to prior years.

Strategic Implication

Cost segregation studies still work — but the immediate deduction impact is lower than it was between 2018–2022.

Planning large acquisitions now requires recalculated ROI projections.

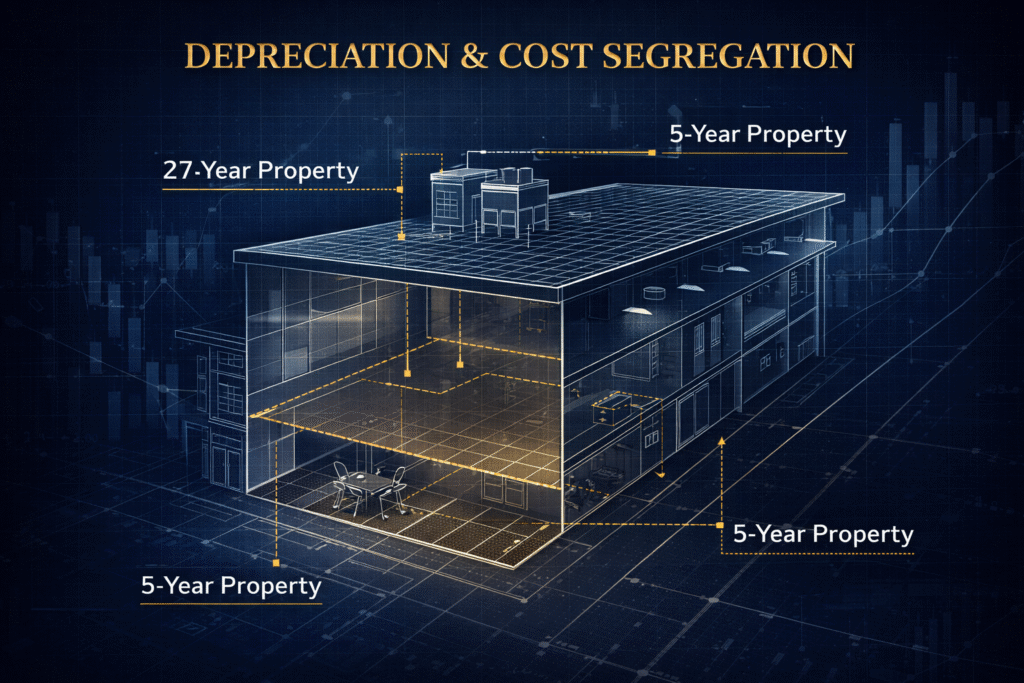

3. Cost Segregation: Still a Cash Flow Accelerator

Cost segregation allows investors to reclassify parts of a building into shorter depreciation categories (5, 7, or 15 years).

Even with bonus depreciation at 20%, accelerating depreciation can still:

- Reduce taxable income

- Improve early-year cash flow

- Increase internal rate of return (IRR)

Cost segregation remains particularly effective for:

- Properties valued above $500,000

- Recently renovated buildings

- Newly constructed developments

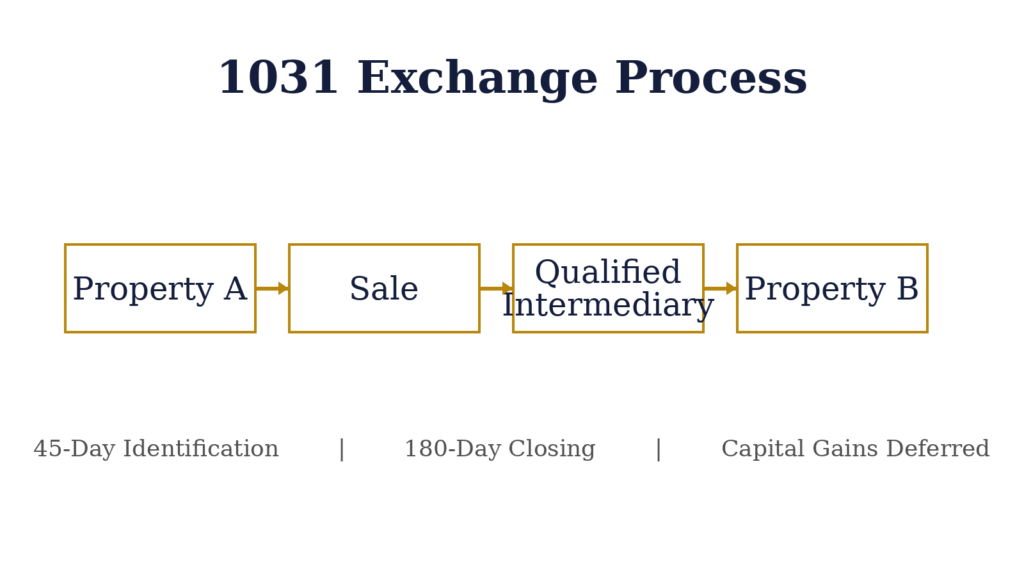

4. 1031 Exchanges: Tax Deferral Remains Powerful

A properly executed 1031 exchange allows you to defer:

- Capital gains tax

- Depreciation recapture tax

As long as proceeds are reinvested into like-kind real estate within:

- 45 days to identify replacement property

- 180 days to close

2026 Reminder

1031 exchanges now apply only to real property (not personal property, vehicles, or equipment).

Used strategically, 1031 exchanges allow investors to:

- Upgrade into larger assets

- Consolidate portfolios

- Relocate investments geographically

- Compound wealth without tax erosion

5. Opportunity Zones: 2026 Recognition Year Alert

Opportunity Zone investments still offer:

- Tax deferral on capital gains invested

- Potential tax-free appreciation if held 10+ years

Important 2026 update:

Capital gains deferred through prior Opportunity Zone investments must be recognized by December 31, 2026, unless disposed of earlier.

New Opportunity Zone investments still qualify for 10-year appreciation exclusion, but the original step-up benefits are no longer available.

This strategy is now primarily long-term appreciation focused.

6. Qualified Business Income (QBI) Deduction — Monitor Legislative Changes

The Section 199A deduction allows eligible pass-through investors to deduct up to 20% of qualified business income.

However, this provision is scheduled to expire after 2025 unless Congress extends it.

As of early 2026, investors should monitor:

- Legislative updates

- Income thresholds

- Wage and property limitation rules

High-income real estate investors may see changes in effective tax rates if QBI sunsets.

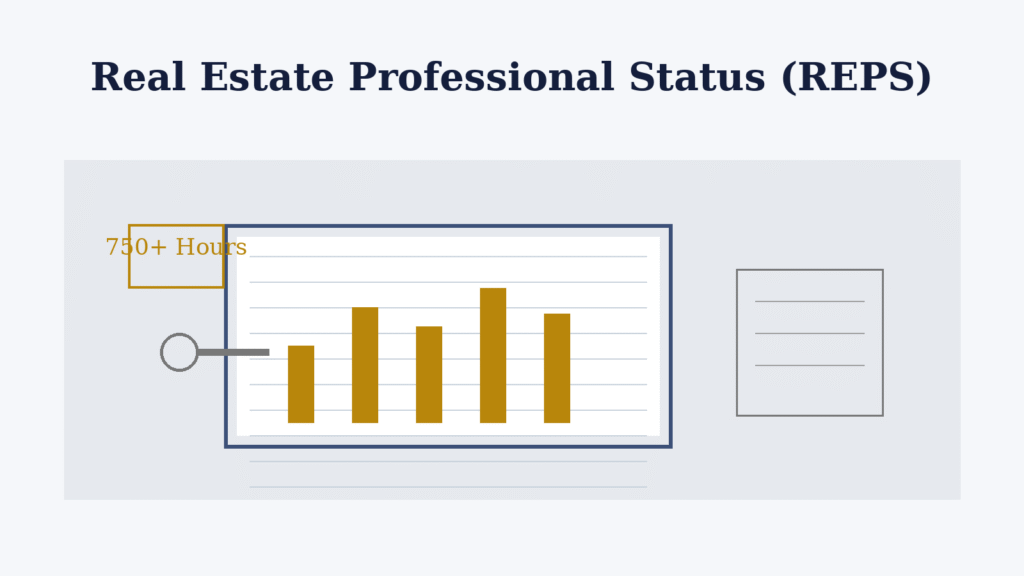

7. Real Estate Professional Status (REPS)

If you qualify as a Real Estate Professional under IRS rules, you can:

- Treat rental losses as non-passive

- Offset W-2 or business income

- Use depreciation more aggressively

To qualify in 2026, you must:

- Spend 750+ hours annually in real estate activities

- Spend more than half of your working time in real estate

This remains one of the most powerful tax classifications available — but requires documentation and compliance discipline.

8. Maximize Deductible Expenses

Real estate investors can deduct legitimate business expenses, including:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Professional services (legal, accounting)

- Travel related to property management

Accurate bookkeeping is no longer optional.

The IRS continues increasing digital audit capabilities in 2026.

Clean records protect deductions.

9. Self-Directed IRAs & Solo 401(k)s

Using retirement accounts to invest in real estate allows:

- Tax-deferred growth

- Potential tax-free growth (Roth structures)

- Higher contribution limits (Solo 401(k))

However, prohibited transaction rules remain strict.

Improper self-dealing can disqualify the entire account.

Professional guidance is critical when using retirement funds for property purchases.

10. Plan for Depreciation Recapture

When selling investment property, depreciation recapture is taxed at up to 25%.

Strategies to manage recapture include:

- 1031 exchanges

- Long-term hold strategies

- Structured exit planning

- Installment sales

Exit tax strategy should be discussed before listing the property — not after receiving an offer.

2026 Strategic Reality: Tax Efficiency Requires Active Planning

The tax environment in 2026 is more complex than prior years:

- Bonus depreciation is reduced.

- Opportunity Zone deferral timing is maturing.

- QBI remains uncertain.

- IRS enforcement funding has increased.

Real estate remains one of the most tax-advantaged asset classes available — but passive investing without tax planning leaves money exposed.

Bottom Line

Tax strategy is not something you think about in April.

For real estate investors in 2026, it is a year-round structural decision that impacts acquisition, cash flow, refinancing, and exit planning.

Depreciation rules are shifting.

Bonus incentives are phasing down.

Opportunity Zone timelines are maturing.

And legislative changes remain possible.

The investors who stay ahead of these changes will protect their margins and compound wealth more efficiently.

The ones who wait will react — and usually overpay.

At John E. Geantasio CPA LLC, we work with real estate investors throughout Monmouth County and New Jersey to design proactive, audit-ready tax strategies — not last-minute filings.

With over 35 years of experience advising property owners, landlords, and developers, John helps investors:

- Structure entities correctly

- Maximize depreciation strategically

- Plan 1031 exchanges properly

- Reduce recapture exposure

- Align tax strategy with long-term wealth goals

Real estate creates opportunity.

Smart tax planning protects it.

If you’re serious about building and preserving real estate wealth in 2026, now is the time to review your strategy — before decisions are locked in.e.