Retirement means you finally get to call the shots with your time. Want to spend an afternoon watching old episodes of Friends?

Go for it.

But there’s another perk you might not have considered—having more control over your money.

When you’re working, your paycheck is fixed, and managing your tax situation is tricky. But in retirement, you decide how much to withdraw and from which accounts, which can significantly impact your taxes now and in the future.

Many experts recommend withdrawing from taxable accounts first, followed by traditional IRAs and other tax-deferred accounts, while saving Roth IRAs and Roth 401(k)s for last. This strategy allows tax-advantaged accounts to grow longer. Withdrawals from tax-deferred accounts are taxed, while Roth withdrawals are tax-free if you’re over 59 1/2 and the account is at least five years old.

Want to make the most of your retirement savings? Looking for a CPA near me for taxes to help minimize your tax bill?

Stick around as we explore the best withdrawal strategies to keep more of your money in your pocket.

Optimize Your Retirement Withdrawals for Better Tax Efficiency

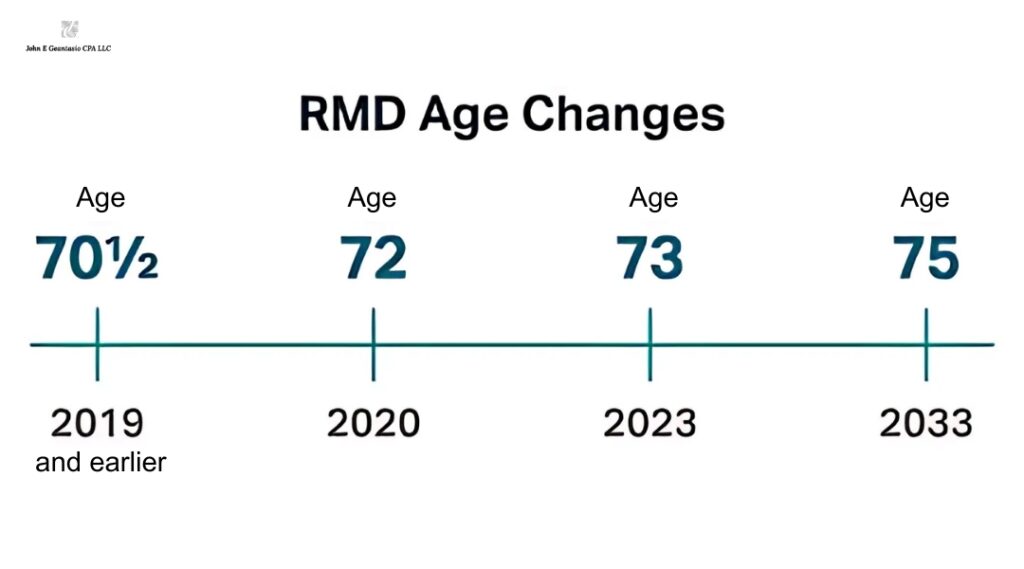

In recent years, some retirement experts have questioned whether the traditional approach of delaying withdrawals from tax-deferred accounts is the best strategy to minimize taxes and preserve your savings for later years. Waiting too long to withdraw can lead to large, taxable required minimum distributions (RMDs), which now begin at age 73.

These RMDs are taxed at ordinary income tax rates, which range from 10% to 37%, and could push you into a higher tax bracket and trigger Medicare high-income surcharges, according to Wade Pfau, a professor of retirement income at the American College of Financial Services

Roger Young, a certified financial planner and thought leadership director for T. Rowe Price, shares this perspective. He points out that the conventional withdrawal strategy tends to concentrate taxable income in the middle retirement years, where almost all of your income is taxable.

Instead, retirees who have a mix of accounts could generate income more tax-efficiently by withdrawing from a combination of taxable and tax-deferred accounts and making strategic conversions to Roth accounts.

This approach helps you stay in a lower tax bracket.

Here’s a practical method to achieve this: start by withdrawing enough from your taxable accounts to cover your spending needs and income taxes.

Next, calculate how much you can withdraw from your tax-deferred accounts and convert to a Roth account while staying within your desired tax bracket.

Maximize Your Tax Benefits with Strategic Withdrawals and Roth Conversions in 2024

In 2024, married couples filing jointly can have up to $94,300 in taxable income and stay within the 12% tax bracket, while for singles, the limit is $47,150.

These thresholds are crucial because they are near the points where you can qualify for a 0% tax rate on long-term capital gains and qualified dividends (assets held for over a year).

Specifically, the 0% rate applies to singles with taxable income up to $47,025 and married couples with joint taxable income up to $94,050.

By strategically withdrawing from both taxable and tax-deferred accounts while staying within these income thresholds, you gain two key advantages.

First, you pay taxes on your tax-deferred withdrawals at a lower rate, reducing the size of these accounts and consequently shrinking your required minimum distributions (RMDs).

Second, you might qualify for the 0% tax rate on capital gains from your taxable accounts.

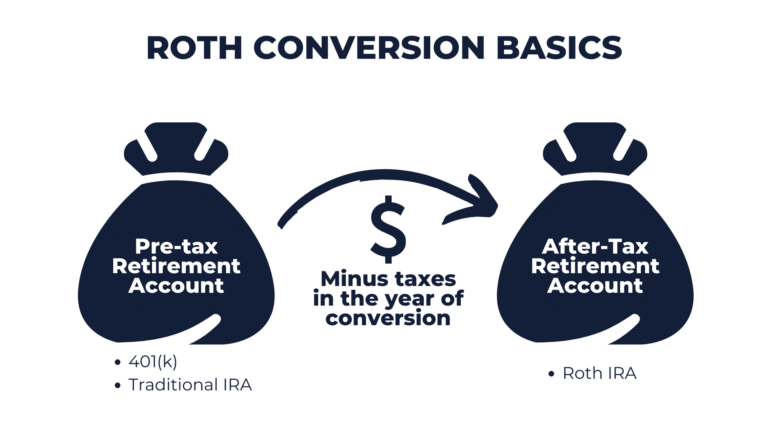

Additionally, making conversions from a traditional IRA to a Roth IRA at a lower tax rate can significantly increase the amount of tax-free income available in your later years. Ideally, it’s best to use assets from your taxable accounts to pay the taxes on these conversions.

According to financial expert Pfau, postponing Roth conversions until after depleting your taxable accounts may force you to use IRA funds to cover the tax bill. While this isn’t disastrous—especially if you’re 59 1/2 or older and can avoid the 10% early-withdrawal penalty—it does reduce the amount you can invest in the Roth, thereby affecting your future tax-free income.

Understanding Taxes on Your Social Security Benefits

Converting funds from your traditional IRAs to a Roth IRA can be a smart move to reduce your taxable income in the future. Ideally, this means that most of your withdrawals will come from your Roth IRA, helping you avoid what some experts call the “Social Security tax torpedo.”

This term refers to the situation where up to 85% of your Social Security benefits may be taxed.

To understand this better, you need to know how taxes on Social Security benefits are calculated. The key figure here is what Social Security calls your “provisional income.”

This is calculated by adding half of your Social Security benefits to other sources of income that make up your adjusted gross income. This includes withdrawals from traditional tax-deferred accounts, dividends, interest, capital gains from taxable investment accounts, and interest from municipal bonds.

Here are the thresholds to keep in mind:

- If you’re a single filer with a provisional income between $25,000 and $34,000, up to 50% of your benefits will be taxable.

- For joint filers, this range is $32,000 to $44,000.

- If your provisional income exceeds $34,000 for single filers, or $44,000 for joint filers, up to 85% of your benefits will be taxable.

These income thresholds have remained unchanged for over 30 years and aren’t adjusted for inflation. As a result, more retirees find themselves paying taxes on a portion of their Social Security benefits. Currently, more than half of retirees are affected by these taxes, according to the Center for Retirement Research at Boston College.

One strategy to reduce these taxes is to increase your Roth IRA holdings through strategic conversions. Withdrawals from a Roth IRA don’t count towards your provisional income.

Additionally, if you can delay claiming Social Security until age 70, your monthly benefits will be higher. This gives you more time to convert funds from your tax-deferred accounts to a Roth IRA, further lowering the taxes on your benefits. T. Rowe Price’s experts suggest that this approach can be beneficial for many retirees.

By planning ahead and making thoughtful decisions about your retirement accounts, you can better manage the taxes on your Social Security benefits and maximize your income in retirement.

Smart Strategies for Charitable Giving from Your IRA

If you’re thinking about donating money from your tax-deferred accounts to charity, you might not need to take out as much as you think right now. A useful way to lower your Required Minimum Distributions (RMDs) and your tax bill is to make qualified charitable distributions (QCDs).

These are donations that go straight from your IRA to approved charities. You can start doing this at age 70 1/2. Once you reach the age when you’re required to take distributions, your charitable donation will count towards your RMD.

While you can’t deduct a QCD, it will lower your adjusted gross income. This can reduce the provisional income used to figure out taxes on your Social Security benefits. For 2024, you can donate up to $105,000 directly from your IRA to a qualified charity.

If you’re concerned about needing money for long-term care or other late-in-life expenses, you can plan to leave your IRA funds to charity after you pass. The charity won’t have to pay taxes on the money, and you can leave more tax-friendly assets to your heirs.

Keep in mind, though, that this won’t free you from taking RMDs and paying taxes on those withdrawals while you’re still alive.

Making QCDs and leaving IRA funds to charity are effective ways to support causes you care about while managing your finances wisely.

Managing Your Estate and Taxes

Transferring more of your assets into Roth accounts won’t just reduce your taxes later in life. It can also help your heirs if they inherit money from those accounts.

Under the SECURE Act of 2019, if you pass away on or after January 1, 2020, and leave behind a traditional IRA or another tax-deferred account, your adult children and other non-spouse heirs have two options:

They can take a lump sum and pay taxes on the full amount, or they can move the funds into an inherited IRA and withdraw all the money within 10 years.

If you were already taking required minimum distributions (RMDs) when you died, your heirs might also need to take annual withdrawals based on their life expectancy, which could mean paying taxes during their peak earning years.

However, spouses can still roll inherited IRAs into their own accounts. Due to confusion about these rules, the IRS has waived the RMD requirement for non-spouse heirs for the past few years and will do so again in 2024.

The 10-year rule also applies to inherited Roth IRAs, but the advantage here is that heirs don’t have to pay taxes on the withdrawals or take RMDs. This gives them flexibility, including the option to let the account grow tax-free for up to ten years before withdrawing the money.

Planning for Your Heirs: A Smart Move with Your Appreciated Investments

If you have a sizable brokerage account that has grown significantly over time, it’s wise to think about how to pass on those assets to your heirs. With the current tax laws, inherited investments benefit from a “step-up” in their cost basis, meaning they are revalued at the current market price when you pass away.

This means that if your heirs sell those investments right away, they won’t owe taxes on any of the gains, no matter how much the investments have appreciated since you bought them.

Final Thoughts

Planning your retirement withdrawals wisely can make a big difference. By working with a CPA near me for taxes, you can create a smart strategy—combining withdrawals from different accounts, making strategic Roth conversions, and even giving to charity directly from your IRA to reduce your taxable income.

A well-managed plan doesn’t just benefit you—it can also help your heirs down the road. With the right tax strategies in place, you can enjoy your retirement without stressing over taxes, leaving more time for what you love, like those Friends marathons.

Take charge of your financial future and make your retirement savings work smarter for you!

Frequently Asked Questions

Ques. 1. What is the best order to withdraw from retirement accounts?

Ans. 1. When planning your retirement withdrawals, the traditional advice is to start with taxable accounts, then move to tax-deferred accounts like traditional IRAs and 401(k)s, and save Roth IRAs and Roth 401(k)s for last. This strategy allows tax-advantaged accounts to grow for as long as possible. However, a more balanced approach—mixing withdrawals from different account types—can often be more tax-efficient based on individual circumstances. If you’re unsure which strategy works best for you, consulting a CPA near me for taxes can help optimize your withdrawals and minimize tax liabilities.

Ques 2. What are Required Minimum Distributions (RMDs) and when do they start?

Ans. 2. RMDs are the minimum amounts that must be withdrawn from your retirement accounts each year starting at age 73. The amount is based on your account balance and life expectancy. Not taking RMDs on time can result in hefty penalties.

Ques. 3. How do Roth conversions work and when should I do them?

Ans. 3. A Roth conversion lets you transfer funds from a traditional IRA or 401(k) into a Roth IRA, paying taxes upfront in exchange for tax-free withdrawals in the future. Timing is key—doing it in years with lower taxable income can help reduce the tax burden. If you’re unsure about the tax impact, consulting a CPA near me for taxes can ensure you make the most tax-efficient decision.

Ques. 4. How can I minimize taxes on my Social Security benefits?

Ans. 4. To reduce taxes on Social Security benefits, consider increasing Roth IRA holdings through strategic conversions and delaying Social Security benefits until age 70. Withdrawals from Roth IRAs do not count towards provisional income, which is used to determine the taxability of Social Security benefits.

Ques. 5. What are Qualified Charitable Distributions (QCDs) and how do they work?

Ans. 5. QCDs allow IRA owners aged 70 1/2 or older to donate up to $105,000 directly to charity from their IRA without counting the distribution as taxable income. This helps reduce adjusted gross income (AGI) and can satisfy RMD requirements.

Ques. 6. What is the impact of the SECURE Act on inherited IRAs?

Ans. 6. The SECURE Act requires most non-spouse beneficiaries to withdraw all inherited IRA funds within 10 years. While traditional IRAs incur taxes on withdrawals, Roth IRAs allow tax-free growth and withdrawals within this period. Spouses have more flexible options, including rolling over the account into their own IRA.

Ques. 7. How can I use a mix of account withdrawals to stay in a lower tax bracket?

Ans. 7. By strategically withdrawing from both taxable and tax-deferred accounts, you can manage your taxable income to stay within lower tax brackets. This approach can help minimize taxes on withdrawals and reduce the size of future RMDs.

Ques. 8. What are the tax benefits of donating appreciated investments to charity?

Ans. 8. Looking for a CPA near me for taxes? Donating appreciated investments directly to charity can be a smart tax move. By doing so, you can avoid capital gains taxes and still claim a charitable deduction for the full market value of the asset. This approach is often more tax-efficient than selling the investment and donating the proceeds.

Ques. 9. How do step-ups in basis rules benefit heirs of appreciated investments?

Ans. 9. When heirs inherit appreciated investments, they receive a step-up in basis, which revalues the assets at their current market price. This means they won’t owe capital gains taxes on any appreciation that occurred during the original owner’s lifetime if they sell the assets immediately.

Ques. 10. What are the 2024 tax brackets and thresholds for married couples and singles?

Ans. 10. For 2024, married couples filing jointly can have up to $94,300 in taxable income and remain within the 12% tax bracket, while singles can have up to $47,150. These thresholds are also where you may qualify for a 0% tax rate on long-term capital gains and qualified dividends.

Also Read-