Many people are living longer, and with age comes the need to consider how to pass on their assets to loved ones. This is especially true for the Silent Generation (people in their 70s and above) who hold a significant amount of wealth.

Tax planning is crucial in this process to ensure your family inherits as much as possible. This blog post will explore several strategies to help you transfer wealth tax-efficiently.

So, keep reading to learn how to preserve your legacy for future generations.

1. Planning Your Legacy: How to Pass on Your Wealth Effectively

Have you ever wondered what happens to your belongings and money after you pass away?

An estate plan helps you decide exactly who inherits your assets, like your house or savings and minimizes the amount of taxes they have to pay.

In the United States, if the total value of your estate exceeds a certain amount, the government can take a significant chunk in taxes. As of 2023, anything over the exemption amount could be taxed as high as 40%! That’s a big chunk of your hard-earned money going to the government instead of your loved ones.

An estate plan helps you avoid this by allowing you to specifically designate who receives your belongings. It also considers what gets deducted from the total value of your estate before taxes are applied. This can include things like outstanding debts, charitable donations, and anything you leave to your spouse. By planning ahead, you can ensure your wishes are followed and your heirs receive the maximum benefit from your legacy.

2. Spouses Can Leave Assets to Each Other Tax-Free

Federal tax law allows married couples to transfer wealth to each other without any tax implications, whether during their lifetime or after death. This means that assets passed to a spouse are entirely tax-free. However, it’s important to note that this defers the tax liability until the surviving spouse passes away.

Since January 2011, the IRS has implemented a Portability Rule to help spouses reduce estate tax burdens. Under this rule, the unused portion of the first spouse’s lifetime exemption can be transferred to the surviving spouse. For instance, if only half of the $13.61 million lifetime exemption is used, the surviving spouse can add the remaining $6.8 million to their own $13.61 million exemption, totaling $20.41 million. To benefit from this rule, the surviving spouse needs to file an estate tax return for the deceased spouse.

It’s important to note that only Hawaii and Maryland extend portability for state-level estate taxes. Additionally, to fully benefit from these provisions, both spouses ideally should be U.S. citizens. While the IRS recognizes same-sex marriages for these purposes, it does not extend the same benefits to registered domestic partnerships or civil unions.

3. Transferring Your Wealth with Less Tax Bite

There are ways to share your wealth with loved ones while minimizing the amount taken by taxes. This can be especially helpful if you’re not married or want to leave money to people outside your immediate family.

One strategy is to create an irrevocable trust. Think of a trust as a special container that holds your valuable assets. You, the grantor, put things like money, investments, or even a life insurance policy into the trust. You then appoint a trustee, a trustworthy person or institution, to manage the trust according to your wishes.

The beauty of an irrevocable trust is that the assets inside it generally don’t count towards your estate’s taxable value when you pass away. That means potentially less money going to the taxman and more going to your beneficiaries. There’s another perk: any income earned by the trust’s holdings gets taxed to the trust itself, not to you. This can lower your annual income tax burden as well.

The catch over here is, that once you put something in an irrevocable trust, it’s generally there for good. You can’t change your mind and take it back. This is different from a revocable trust, where you have more control over the assets. So, with an irrevocable trust, careful planning is key.

4. Saving on Taxes Through Annual Gifting

Did you know you can give away money and reduce your future tax burden? It’s called annual gifting, and it allows you to give a specific amount each year without owing taxes on it. This can be a great way to share your wealth with loved ones while also lowering your estate tax bill.

Here’s how it works: The IRS offers an annual gift tax exclusion of $18,000 per person, per year (as of 2023). This means you can give up to $18,000 to anyone you choose, and it won’t count towards your taxes. This amount is adjusted for inflation each year.

Even better, married couples can take advantage of gift-splitting. By filing jointly, they can essentially double the exclusion amount. So, a married couple could give away $36,000 to their child in a single year ($18,000 from each spouse). And if that child has a spouse and children of their own, the possibilities get even more interesting. In that case, the grandparents could potentially gift up to $144,000 each year to their grandchildren ($72,000 from each grandparent).

5. Saving on Taxes with Educational and Medical Gifts

Making payments directly to an accredited school or medical provider on behalf of someone else can be a tax-free strategy. This means that tuition and medical bills you pay for others won’t count against the annual gift tax exclusion of $18,000 (as of 2023). This is a great way to help out with educational or medical expenses without worrying about tax implications. Contributions to political organizations are also exempt from the annual gift tax limit, offering another avenue for tax-advantageous giving.

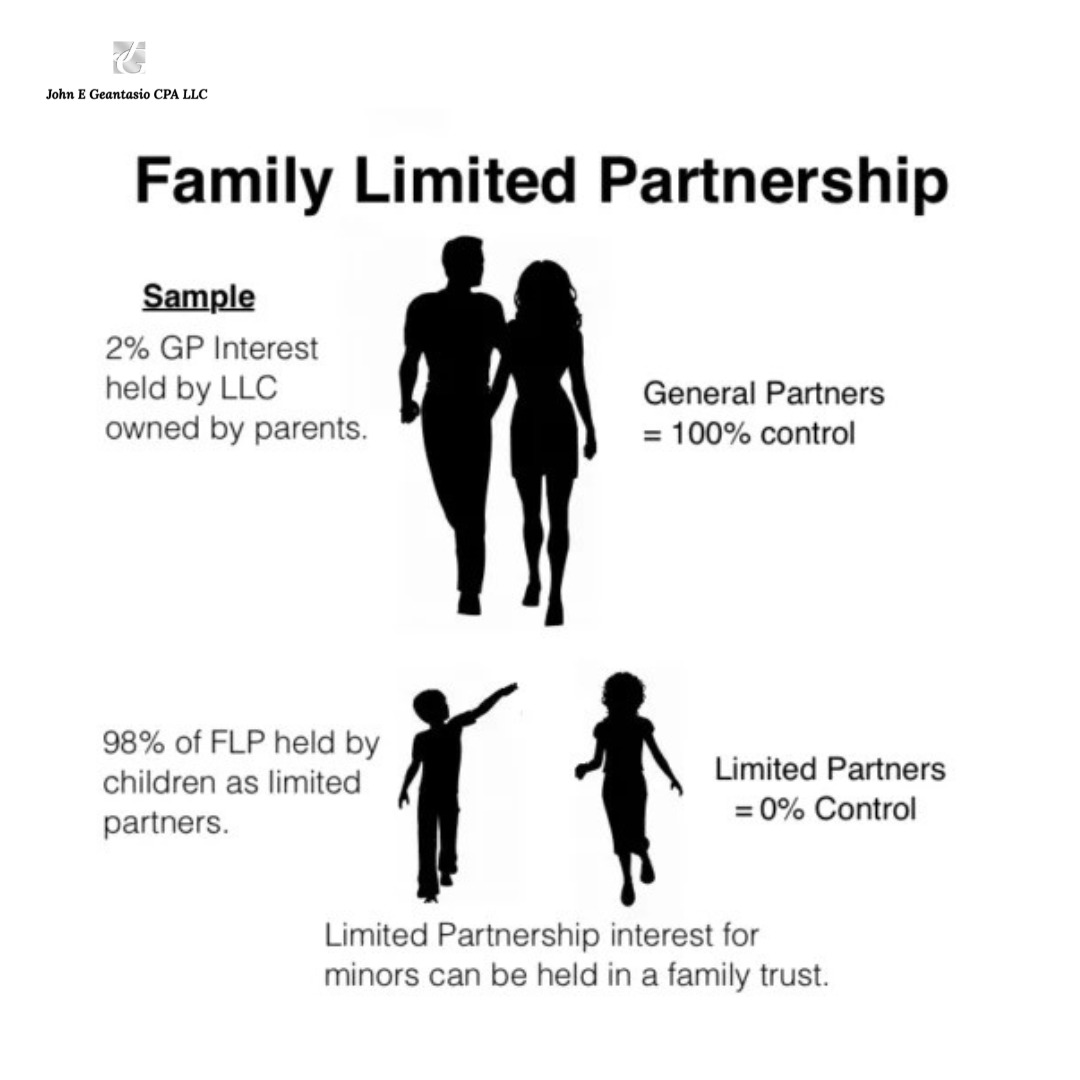

6. Owning Family Assets Together: Family Limited Partnerships

A family limited partnership (FLP) is a way for families to jointly own assets. Think of it like a team where family members work together to manage their wealth. There are two main roles in an FLP: general partners and limited partners.

General partners typically have more control over the assets, while limited partners contribute financially but have less say in how things are run. This can be a good option for parents or grandparents who want to share their wealth with their children and grandchildren but still maintain some oversight.

FLPs can also offer tax benefits. For example, they can help reduce or even avoid gift and estate taxes when transferring assets to heirs. The IRS does require that FLPs have a legitimate purpose, such as generating income through investments.

Overall, FLPs can be a useful tool for families who want to manage their wealth together and potentially save on taxes.

7. Generation-Skipping Wealth Transfer Trust: A Way to Leave Money to Grandchildren

Are you thinking about leaving money or property to your grandchildren? You might want to consider a generation-skipping transfer trust. This type of trust lets you give money to your grandchildren without it being counted towards your estate tax.

There is a tax on gifts and inheritances above a certain amount. Currently, that amount is $13.61 million per person. However, this exemption is shared with the gift tax exemption. There’s also an annual exclusion of $18,000 per recipient that you can use for gifts without them counting towards the tax.

A generation-skipping transfer trust can be a way to use your exemption effectively and pass on more wealth to your grandchildren. The key is to make sure the trust is set up correctly. The beneficiary, which can be your grandchild, must be the only person who can get money out of the trust and they must be able to take out up to $18,000 per year without it counting towards the tax.

Ways to Save on Taxes When Transferring Wealth

There’s no one-size-fits-all answer to saving on taxes when giving away your money or possessions. The best approach depends on your unique situation. However, some strategies can significantly reduce the tax burden on your beneficiaries. Let’s explore a few options.

One approach is to gradually transfer wealth throughout your lifetime instead of leaving everything in a will. The good news is the IRS allows you to gift up to $18,000 per person each year (in 2024) without incurring any gift tax. This means you can spread out your giving to multiple people and maximize the tax benefits.

Another strategy involves creating a special trust, called a generation-skipping transfer trust. This trust allows you to benefit future generations, such as grandchildren or even great-grandchildren, by minimizing the estate taxes they might face when you’re gone. This can be particularly useful if you have younger beneficiaries you want to include in your financial legacy.

Greatest Wealth Transfer in the United States

In the United States, a huge transfer of wealth is happening right now. The baby boomer generation, those born between 1946 and 1964, is getting older and passing down their money to their children. By 2045, it’s estimated that millennials and Gen Xers will inherit a giant sum of $84 trillion from their baby boomer parents. This is an incredible amount of money! There’s a reason why this transfer is so large. The U.S. tax code allows people to give away up to $13.61 million to their heirs without having to pay federal taxes on it. This makes it easier for baby boomers to pass on their wealth to their children.

Editor’s Choice:

The Great Wealth Transfer: Will it Shake Up the Markets?

Tax Season 2024: Why Gen Z Finds Tax Filing So Stressful?

Tax Season 2024: Do this If You Didn’t Get Your W-2 Form Yet