Spring Lake is not a typical rental market.

Property values are high.

Appreciation has been strong.

Seasonal demand creates income volatility.

New Jersey income and property taxes are among the highest in the country.

If you own two or more properties here, you are likely sitting on significant embedded gain. On paper, that feels like success.

On a tax return, it creates exposure.

Spring Lake real estate builds wealth quietly over time. Without a structured plan, tax liability builds just as quietly. The cost of not planning often shows up at the worst moment — when you sell, refinance, or transfer property to heirs.

Tax strategy is not about reducing this year’s bill. It is about protecting appreciation that has taken decades to accumulate.

Why Spring Lake Investors Face Unique Tax Exposure

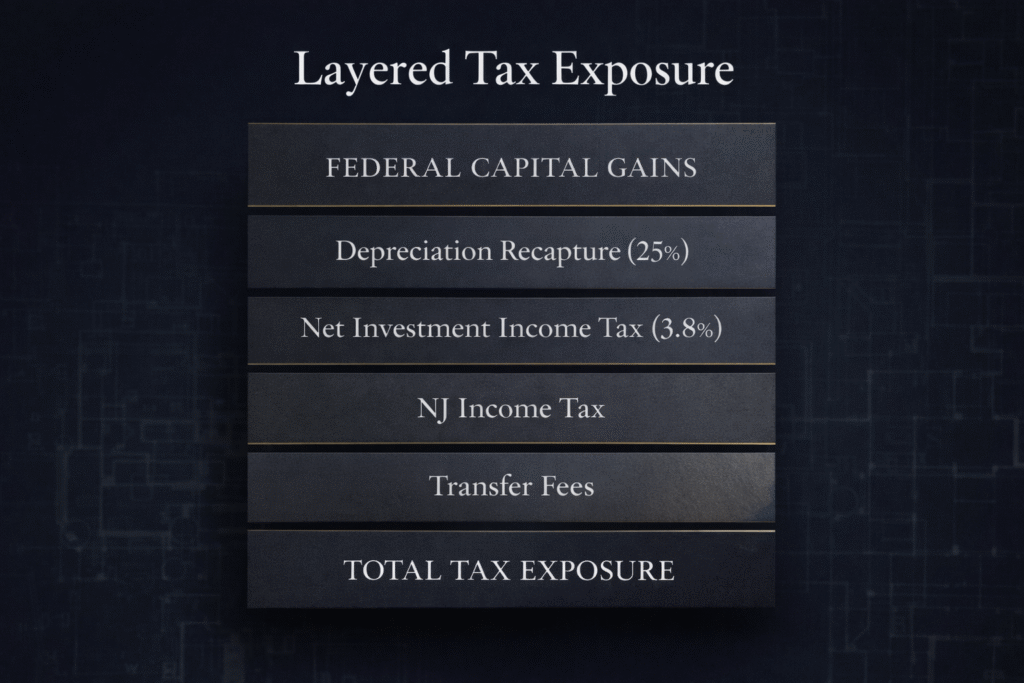

The risks here are layered.

First, appreciation is substantial. Many long-term owners purchased at values that look unrecognizable compared to today’s market. When those properties are sold, the gain is not modest. It often includes:

- Federal capital gains tax

- Federal depreciation recapture at up to 25%

- Net Investment Income Tax for high earners

- New Jersey Gross Income Tax

- State-level transfer fees

The stacking effect is what surprises investors. The gain is taxed at multiple levels, and New Jersey does not provide preferential long-term capital gains treatment the way the federal system does.

Second, passive loss limitations restrict flexibility. Many high-income investors assume rental losses will offset W-2 or business income. In reality, most losses are suspended and carried forward. On paper, you may show depreciation. In practice, you may not receive immediate benefit.

Third, seasonal rental classification can complicate reporting. Shore properties often shift between personal use, seasonal rental, and short-term occupancy. Improper classification can alter loss treatment and increase audit risk.

Fourth, property taxes are substantial. Yet the federal SALT cap limits the benefit of deducting those taxes. You may be paying high local taxes without receiving proportional federal relief.

Spring Lake wealth grows slowly and quietly. Tax exposure grows the same way.

Core Tax Strategies Every Spring Lake Investor Should Evaluate

A sophisticated investor does not rely on one tactic. They evaluate structural strategies that interact over time.

Cost Segregation and Accelerated Depreciation

High-value properties often qualify for accelerated depreciation through cost segregation studies. By breaking components into shorter recovery periods, significant deductions can be front-loaded.

However, accelerated depreciation increases future recapture risk. Without modeling both the deduction phase and the eventual sale, investors can create short-term savings at the expense of long-term friction.

The mistake is claiming acceleration without projecting the exit.

Real Estate Professional Status

For households that qualify, Real Estate Professional Status can convert passive losses into fully deductible losses against active income.

Many investors misunderstand qualification. Ownership alone does not suffice. Hour requirements and material participation standards must be documented carefully.

For high-income households, proper qualification can materially change the tax outcome. Improper qualification can create audit exposure.

Short-Term Rental Structuring

Certain Jersey Shore properties with average stays under seven days may avoid passive activity limitations if participation requirements are met.

This can be powerful in the right scenario. But the rules are technical. Income classification and documentation standards matter. The strategy must align with operational reality.

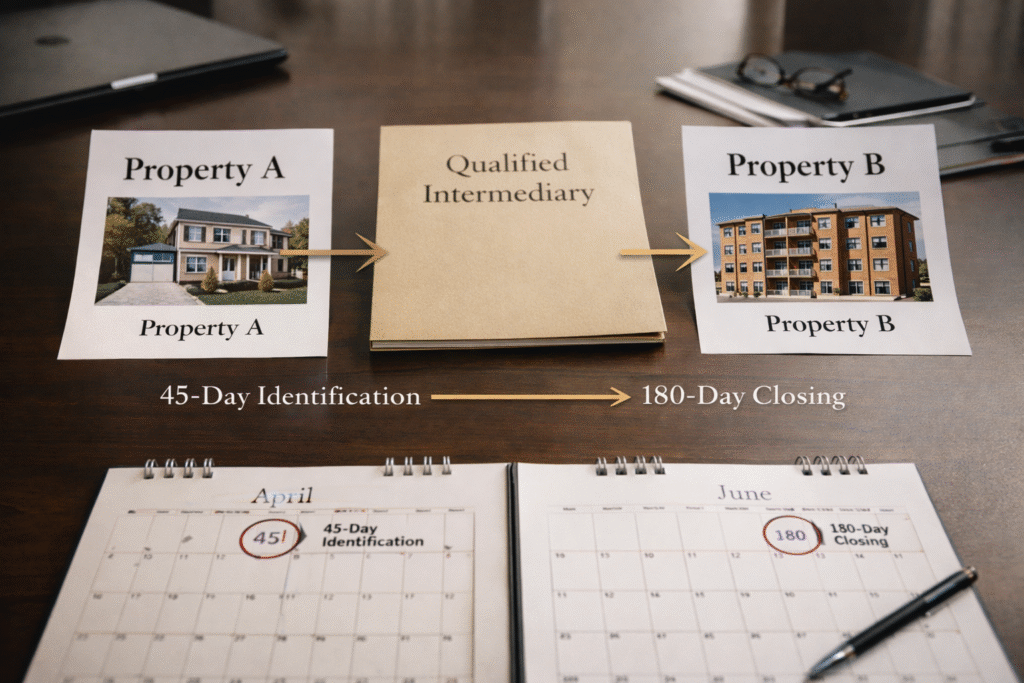

1031 Exchanges

1031 exchanges remain one of the most powerful deferral tools available to real estate investors. But the common error is waiting until a property is under contract to consider it.

Identification windows are tight. Replacement pressure is real. Basis carries forward. The deferred tax does not disappear — it compounds.

A 1031 exchange should be aligned with a long-term capital allocation plan, not treated as a reactive decision.

Strategic Entity Structuring

Entity decisions affect tax efficiency, asset protection, and exit flexibility.

LLCs are often appropriate for asset isolation. S Corporations may be relevant in limited operating scenarios. But New Jersey compliance rules and transfer tax implications must be considered.

The mistake is selecting structure for convenience instead of long-term exit alignment.

New Jersey-Specific Considerations

Spring Lake investors cannot rely on federal strategy alone.

New Jersey Gross Income Tax does not mirror federal capital gains treatment. Gains are taxed as ordinary income at the state level.

Transfer taxes and so-called “exit tax” withholding rules can affect liquidity at closing. Sellers often underestimate how much cash must be reserved at settlement.

Although New Jersey repealed its estate tax, it still maintains an inheritance tax depending on beneficiary classification. For legacy properties, titling decisions and beneficiary planning are not administrative details — they are strategic decisions.

Federal advice without state modeling is incomplete advice.

Exit Planning for Spring Lake Investors

Many Spring Lake investors are long-term holders approaching a transition point. Some are considering downsizing. Others are evaluating estate transfers.

Exit planning is not about deciding whether to sell. It is about deciding how.

Installment sales may smooth income recognition over time.

A properly structured 1031 exchange may reposition capital without triggering immediate gain.

Opportunity Zone investments may offer deferral and potential exclusion benefits if aligned with long-term objectives.

Holding property until death may allow heirs to receive a step-up in basis, effectively eliminating decades of embedded gain.

For highly appreciated assets, advanced tools such as charitable remainder trusts can combine tax deferral with income planning and legacy design.

The right decision depends on timeline, liquidity needs, and family objectives. The wrong decision is making no decision until a buyer appears.