Tax season is over.

You filed your return. You closed the tab. Maybe you felt relief. Maybe frustration. Maybe confusion.

But here’s the truth most taxpayers never hear:

Your tax return is not the end — it’s a diagnostic report for next year.

And what you do right now, in April… will decide how much you pay next year.

Most people wait until March to fix their taxes.

Smart taxpayers fix them in April.

Filing Your Taxes Isn’t the Finish Line — It’s the Starting Point

There’s a belief that once you file your taxes, your job is done.

That belief is expensive.

Because the U.S. tax system doesn’t work on a once-a-year basis. It works on a pay-as-you-go system, which means taxes are supposed to be paid throughout the year as you earn income .

So by the time you file in April, most of your tax outcome is already locked in.

Your income decisions are already made.

Your deductions are already set.

Your missed opportunities are already gone.

That’s why so many people feel frustrated after filing. They realize something went wrong… but it’s too late to fix it.

Unless they use that return the right way.

Because your tax return is not just paperwork.

It’s a report card of your financial behavior.

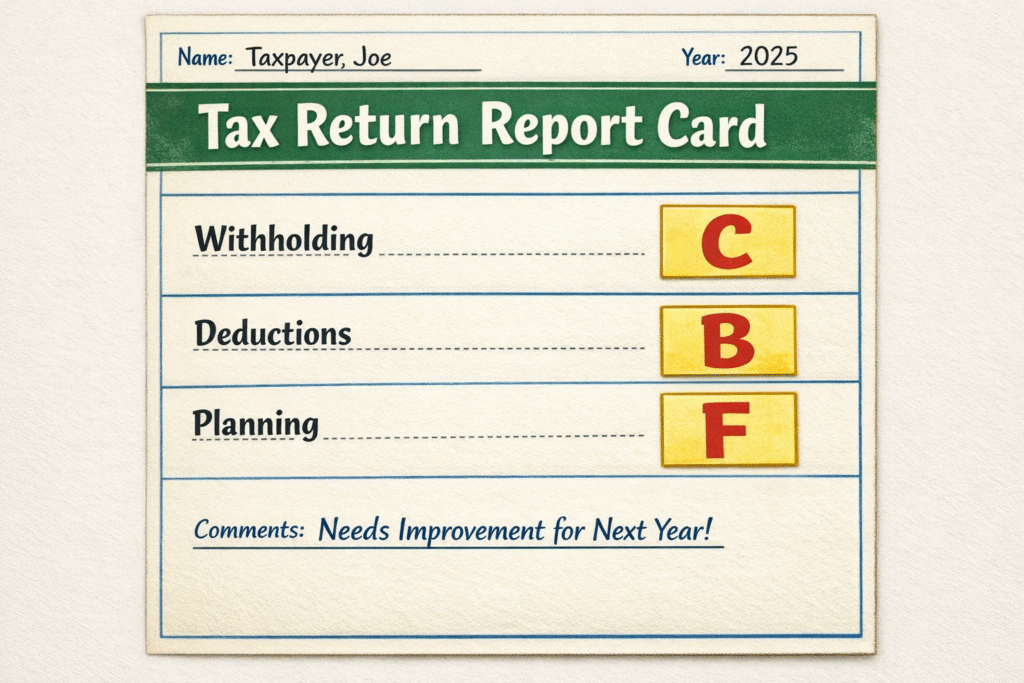

What Your Tax Return Just Revealed About You

Your return is telling you something very specific.

Most people ignore it. Smart taxpayers read it like a strategist.

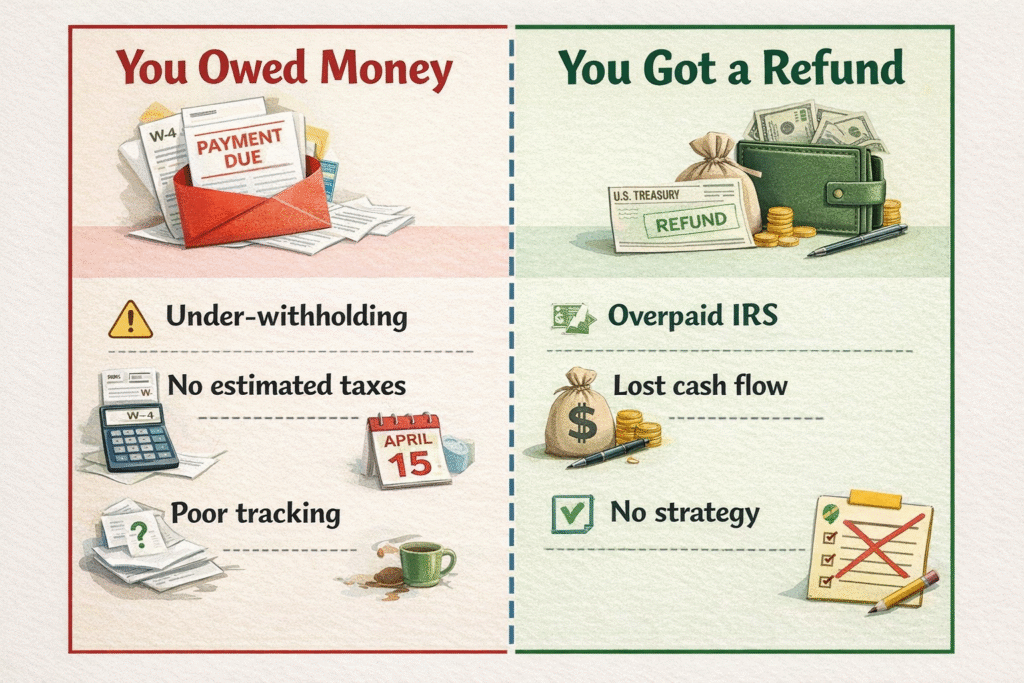

If you owed money, that wasn’t random. It means you didn’t pay enough taxes during the year. That usually happens when withholding is too low, or when income—especially side income or business income—is not tracked properly. The IRS expects taxes to be paid as income is earned, not delayed until filing .

If you received a large refund, that’s not a win either. It means you overpaid all year. You gave the government your money early, and they returned it months later without interest. That’s lost opportunity. That’s cash flow inefficiency.

And if the entire process felt confusing, that’s the clearest signal of all. It means there was no system. Everything was reactive. Documents were gathered at the last minute. Decisions were made under pressure.

Three different outcomes.

Same root problem:

No tax strategy during the year.

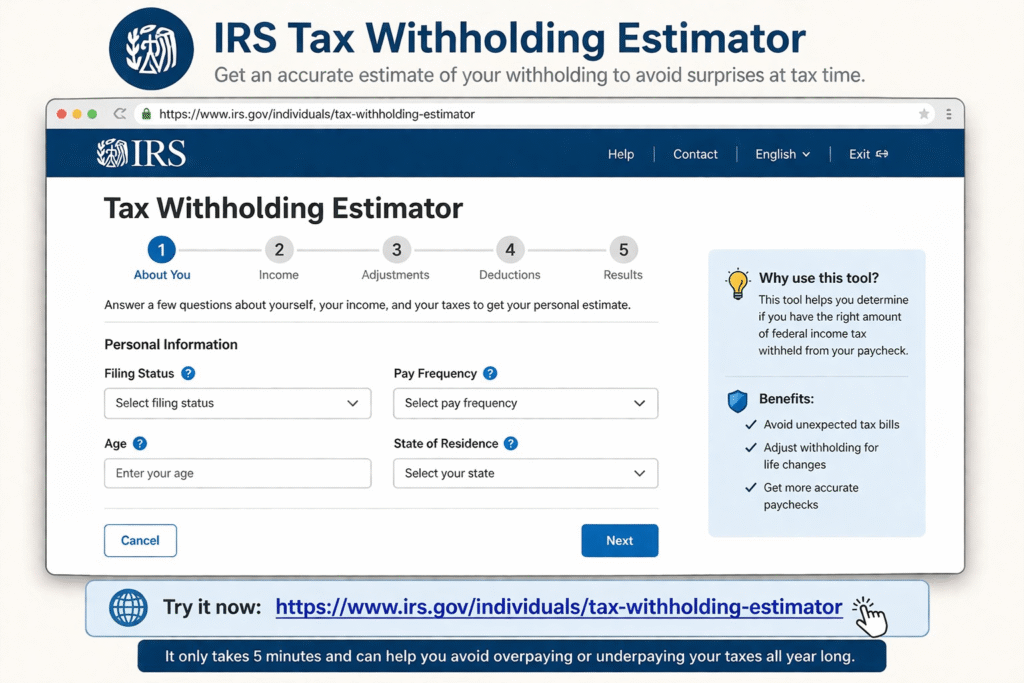

Fix Your Withholding — The Fastest Way to Take Back Control

The simplest place to start is also the most ignored.

Your withholding.

Most employees fill out a W-4 once… and never touch it again. But your income changes. Your life changes. Tax laws change.

Your withholding should change too.

The IRS provides a tool specifically for this:

This tool helps you adjust how much tax is taken from your paycheck so you don’t owe too much—or overpay—at the end of the year. It’s designed to help prevent unexpected tax bills and maximize your take-home pay .

Run it once.

It takes five minutes.

But it can fix the next twelve months.

Because the difference between owing $5,000 and owing $0 is often not strategy.

It’s just withholding.

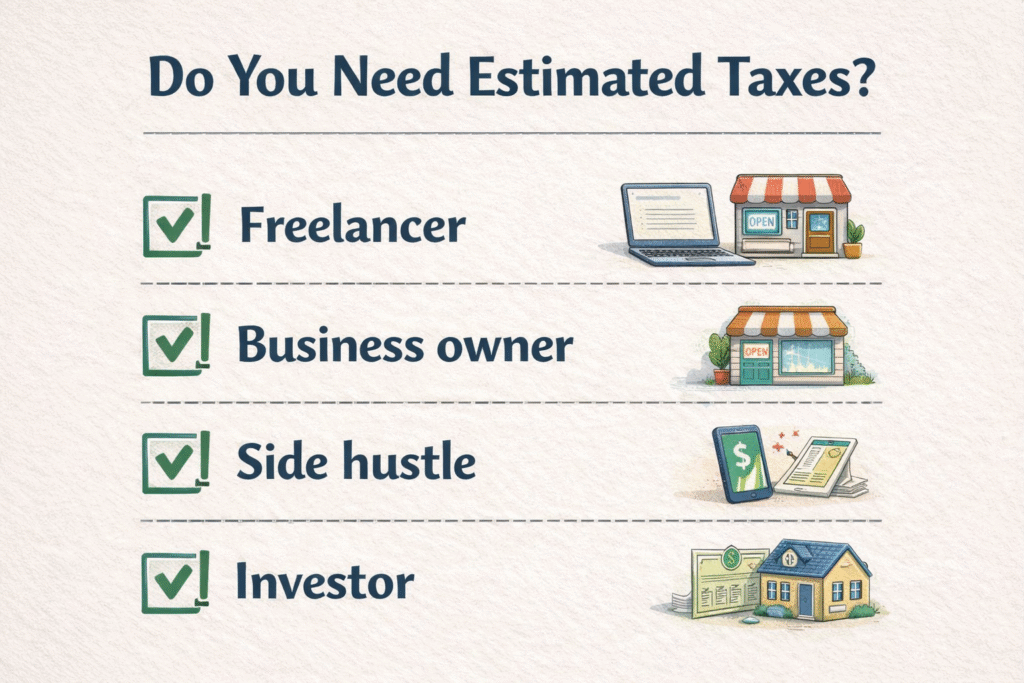

If You Earn Outside a Job, This Step Is Not Optional

If you are self-employed, freelancing, running a business, or earning 1099 income, your situation is different.

No one is withholding taxes for you.

Which means you are responsible for paying them during the year.

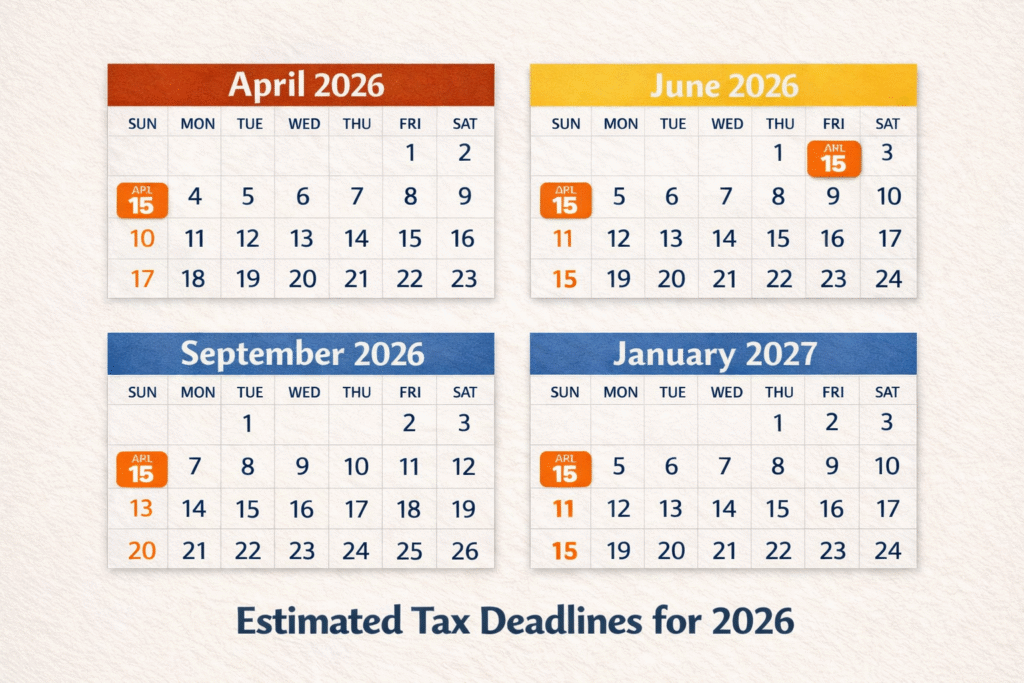

This is where estimated taxes come in.

The IRS requires many taxpayers to make quarterly estimated payments if they expect to owe at least $1,000 when filing .

And here’s the part most people miss:

You can still get penalized… even if you get a refund.

Because the IRS doesn’t just care about how much you paid.

They care when you paid it.

If payments are late or uneven, penalties can apply.

That’s why estimated taxes are not just a compliance issue.

They are a system issue.

The Real Truth: Tax Planning Happens Before December, Not During Filing

This is where the biggest shift happens.

Most people believe tax savings happen when the return is prepared.

They think their accountant “finds deductions.”

But by April, most of the opportunity is gone.

Tax planning is not something you do when filing.

It’s something you do while the year is still happening.

That means:

- Deciding when to recognize income

- Timing business expenses

- Structuring investments

- Using credits before deadlines

For example, energy-related tax credits can significantly reduce your tax bill—but only if the qualifying investment is made before year-end.

This is the difference:

Most people look for tax savings.

Smart taxpayers create them.

And they create them before December 31.

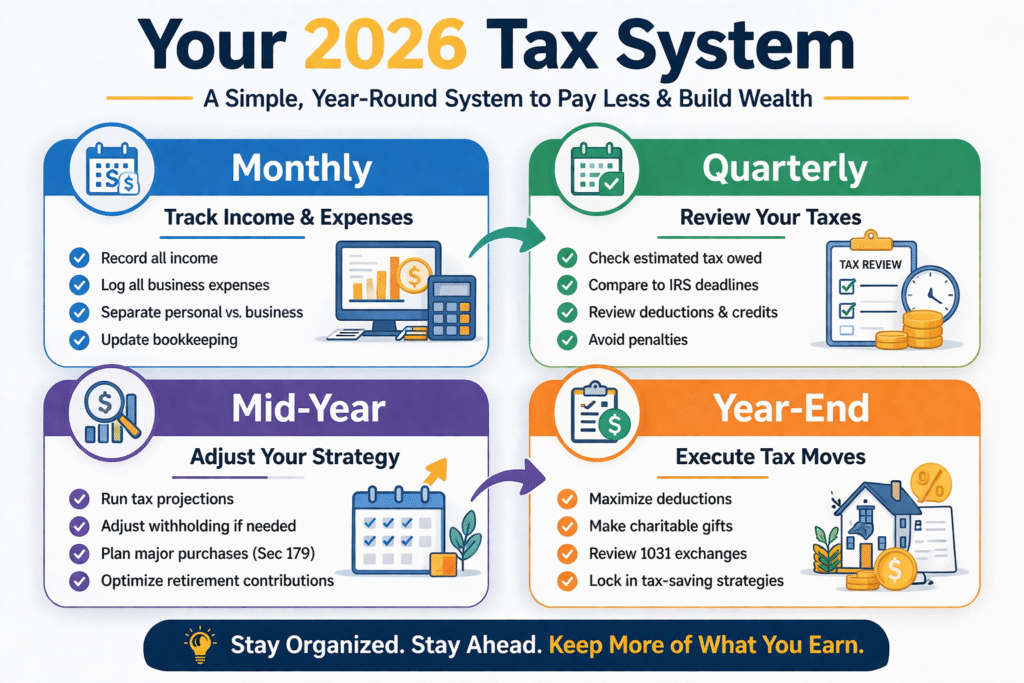

Build a Simple Tax System for 2026 (So You Don’t Repeat This)

The problem isn’t that people don’t know enough.

The problem is they don’t have a system.

Without a system, everything becomes reactive. You forget expenses. You underestimate income. You guess numbers. And by the time you sit down to file, you’re just hoping it works out.

A simple system changes everything.

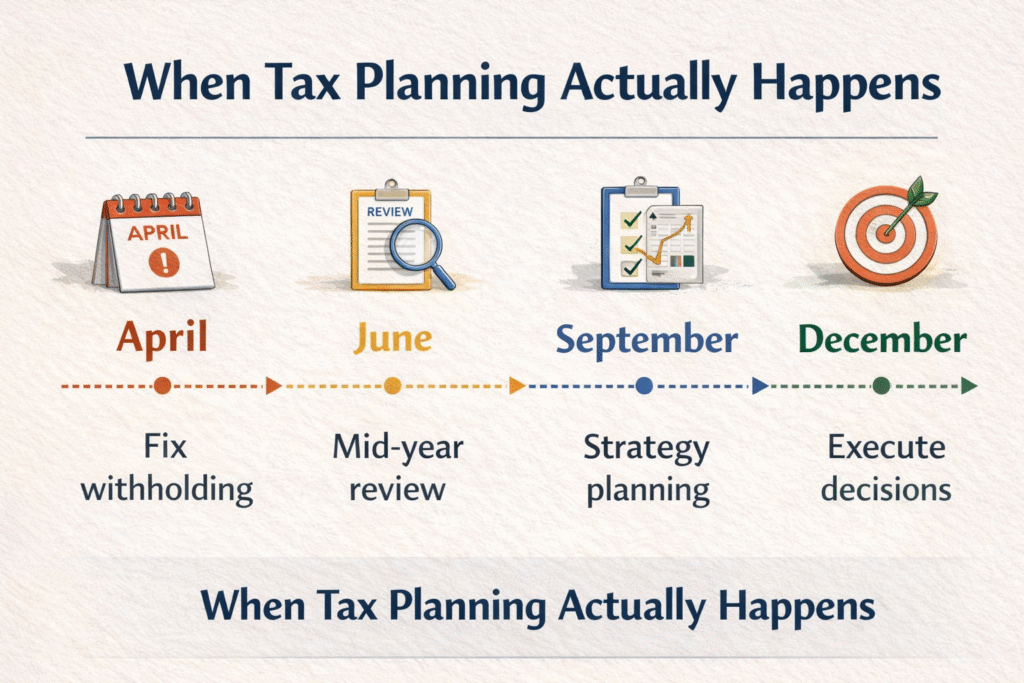

Throughout the year, you should always know how much you are earning and what portion of that is going to taxes. Not approximately. Not eventually. Clearly.

As your income changes, your tax payments should adjust. That could mean updating withholding or increasing estimated payments. Waiting until April is what creates surprises.

Midway through the year, you should pause and review. Are you on track? Are you overpaying? Underpaying? Missing opportunities?

And before the year ends, you should make intentional decisions. This is when strategies actually work. This is when you can still change your outcome.

This is how tax planning becomes predictable.

The Mistakes That Keep People Stuck Every Year

Most taxpayers don’t fail because they don’t work hard.

They fail because they repeat the same cycle.

They wait until March to think about taxes again.

They ignore side income until it shows up as a problem.

They assume deductions instead of documenting them.

They rely on memory instead of records.

And every year, they get the same result.

Unexpected tax bills.

Stress during filing.

No real control.

The IRS has even reported billions in penalties tied to estimated tax mistakes in recent years—largely due to poor timing and lack of planning .

This isn’t a knowledge problem.

It’s a behavior problem.

What Changes When You Start Thinking Like a Strategist

When you shift from filing to planning, everything changes.

You stop reacting to taxes… and start controlling them.

You stop guessing… and start forecasting.

You stop asking, “What do I owe?”

And start asking, “What should I be doing right now?”

That’s when tax strategy becomes powerful.

Because you’re no longer waiting for results.

You’re designing them.

This Is the Best Time to Fix It

Right now, you are in the most valuable moment of the entire tax cycle.

You just filed.

You know what happened.

You know what went wrong.

And you still have the entire year to change it.

This is when real planning begins.

Not in December.

Not in March.

Now.

Your Next Step: A Post-Filing Tax Strategy Review

If you want next year to look different, you need to act differently now.

A Post-Filing Tax Strategy Review is designed for this exact moment.

It helps you:

- Fix your withholding so you don’t overpay or underpay

- Set up estimated taxes correctly

- Identify real opportunities to reduce your taxes this year

You can also explore:

- Your Tax Planning Services page

- A detailed Estimated Taxes Guide

- Strategies on How to Reduce Taxes Legally

- Real outcomes through Case Studies

The One Line to Remember

Most people try to fix their taxes in March.

Smart taxpayers fix them in April.

Because by the time everyone else reacts…

You’re already in control.