The tax problem Hartford business owners notice too late

If you run a business in Hartford, you’ve likely felt this shift already.

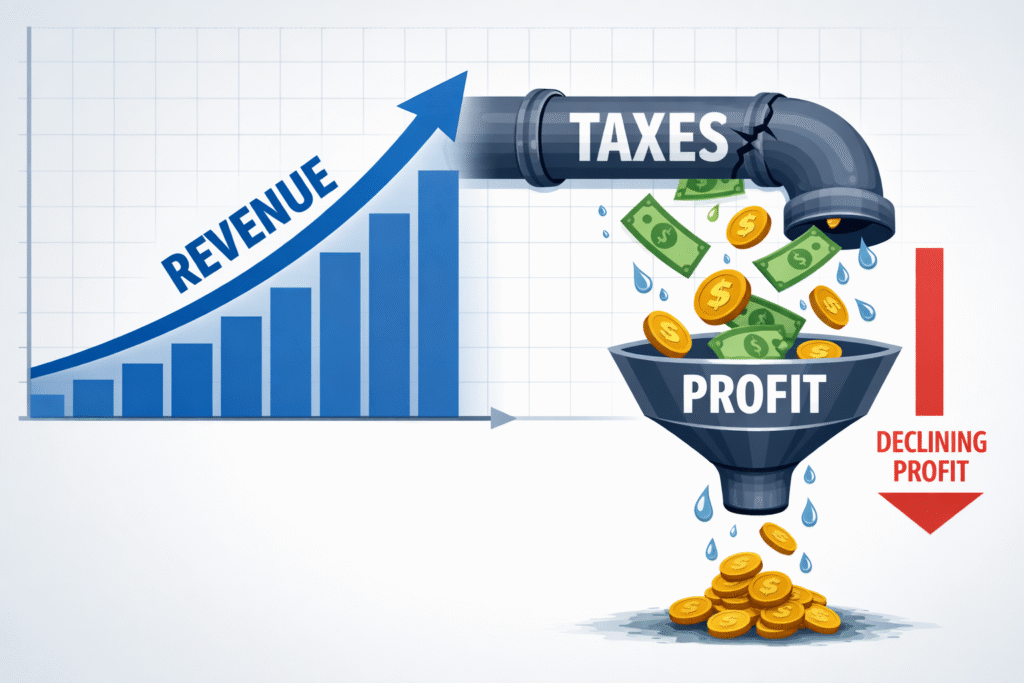

Your revenue grows.

Your workload increases.

But the amount you keep doesn’t follow the same pattern.

By the time tax season arrives, the numbers explain what happened — but they don’t fix it. The decisions that created the tax bill were made months earlier, often without you realizing their impact.

Because in 2026, taxes are no longer just about compliance. They are about control.

And most business owners don’t realize they’ve lost that control until the year is already closed.

That leads to a bigger question… why does this keep happening even to smart, successful business owners?

Why Hartford business owners consistently overpay

The issue isn’t lack of effort. It’s lack of timing.

Most business owners operate inside a system where tax decisions are made after the fact. Income grows, expenses are tracked, and everything is handed to a CPA at year-end. At that point, the role becomes documentation — not direction.

For example, a business owner earning $350,000 as a sole proprietor may only discover in March that they could have reduced self-employment taxes significantly by restructuring earlier in the year. But once December has passed, that opportunity is gone.

This is where the gap begins.

Not because deductions are missed — but because strategy was never built into the year.

So if the problem is timing, the next question becomes: who actually fixes it?

What a strategic CPA changes

A strategic CPA doesn’t start with your tax return. They start with your decisions.

Instead of asking, “What happened last year?”

They ask, “What is about to happen this year — and how do we shape it?”

For instance, when a business owner approaches John earning around $400,000 annually under a default structure, the first step is not filing. It’s identifying how much of that income is unnecessarily exposed to higher tax rates — and what structural changes could immediately shift that burden.

That might involve evaluating whether an S-corp election makes sense, how compensation should be split, or how profits should be retained versus distributed. Each of these decisions directly affects the tax outcome — but only if addressed before the year ends.

This is not theory. It’s applied planning tied to real numbers.

And when this kind of planning is missing, the consequences aren’t abstract — they show up clearly in dollars.

What it costs to stay reactive

When planning doesn’t happen, the cost builds quietly.

It doesn’t appear as one large mistake. It appears as small inefficiencies repeated every year.

- Paying self-employment tax on income that could have been structured differently

- Missing opportunities to shift income into more favorable categories

- Holding profits in ways that increase total tax liability

Individually, each decision might seem minor. But over three to five years, they compound into six-figure differences.

For example, a $300,000 income structured inefficiently could result in tens of thousands more in taxes annually compared to a properly planned structure. Multiply that across multiple years, and the gap becomes significant.

This is where most business owners begin to feel something is off — even if they can’t immediately identify why.

Which leads to the next realization: reducing taxes is not the end goal.

Beyond saving taxes: building a financial fortress

Lower taxes alone don’t create long-term security. What matters is what happens to the money you keep.

The concept of a financial fortress is simple: using tax strategy to systematically move money out of liability and into assets that grow over time.

That includes:

- Real estate that generates income and depreciation

- Retirement structures that defer or eliminate taxes

- Investments that shift income into lower-tax categories

The tax code is designed to reward these behaviors. It encourages business ownership, investing, and asset-building — not just income generation.

A well-built strategy doesn’t just reduce your tax bill this year. It creates a system where each year’s decisions strengthen your long-term position.

Without that system, income alone rarely translates into lasting wealth.

So naturally, the question becomes — how do you know if your current CPA is helping you build this, or just maintaining what exists?

How to recognize the difference in your current CPA

The difference shows up in how conversations happen.

If your CPA primarily engages during tax season, focuses on filing accuracy, and rarely discusses future decisions, they are operating in a compliance role.

If, instead, conversations happen throughout the year — around income timing, entity structure, and strategic moves — that’s a planning relationship.

For example, a proactive CPA might initiate a mid-year review when your income increases significantly, identifying whether estimated payments, restructuring, or reinvestment strategies need to adjust.

A reactive CPA waits until the year ends and reports what already happened.

The distinction is not about competence. It’s about scope.

And once you see that difference, it naturally leads to the next step — what working with the right advisor actually changes.

What changes when strategy is in place

When planning is integrated into your business decisions, the experience shifts.

You’re no longer guessing what your tax bill will be.

You’re no longer making financial decisions without understanding their impact.

You’re no longer reacting under pressure in March or April.

Instead, you have visibility.

For example, if your income spikes mid-year, adjustments are made immediately — not after the fact. If a major purchase or investment is being considered, its tax impact is evaluated before execution.

Over time, this creates consistency.

And consistency is what allows business owners to move from uncertainty to control.

FAQ: What Hartford business owners need to know

Do I need a new CPA, or just better planning?

In many cases, the issue is not replacing your CPA but changing the type of service you receive. A compliance-focused CPA ensures filings are accurate, but planning requires ongoing involvement throughout the year. For example, if your CPA only speaks to you during tax season, planning opportunities are likely being missed. The practical implication is that without proactive guidance, your tax outcome will always be reactive.

At what income level does tax strategy become important?

Tax strategy becomes critical once income reaches a level where structural decisions significantly affect liability, typically around $150,000 to $250,000. At this point, the difference between structures can impact tens of thousands annually. For instance, a business owner crossing $300,000 without restructuring may overpay compared to a planned setup. The implication is that waiting too long increases the cost of missed opportunities.

How often should I review my tax strategy?

Tax strategy should be reviewed multiple times throughout the year, not just annually. Income changes, business decisions, and regulatory updates all affect outcomes. For example, a mid-year income increase should trigger a review to adjust estimates and structure. The implication is that regular reviews prevent surprises and keep strategy aligned with reality.

What to do next

If you’re running a business in Hartford and your income is growing, the risk is not that you’re doing something wrong. The risk is that you’re making decisions without seeing their full impact.

Working with John changes that by bringing those decisions into focus before they’re locked in.

The next step is simple: schedule a strategy session and look at your numbers before this year closes.