The tax problem most Tallahassee business owners don’t see until it’s expensive

If you run a business in Tallahassee, the math can feel confusing.

Your revenue grows. Your business gets more demanding. You take on more responsibility.

But when you look at what you actually keep, it doesn’t reflect that growth.

By the time tax season explains what happened, the damage is already locked in.

Because in 2026, taxes are no longer just about compliance. They are about strategy.

Florida’s zero state income tax creates a dangerous assumption — that you’re already tax-efficient. In reality, most Tallahassee business owners are still losing money at the federal level through entity decisions, income timing, and lack of planning. The absence of state tax doesn’t fix a flawed structure; it just hides it.

And once you see where that loss actually happens, the pattern becomes hard to ignore.

Why Tallahassee business owners still overpay — even in a no state tax environment

The mistake isn’t obvious. It doesn’t feel like a mistake.

It usually starts with a simple setup — an LLC, a clean bookkeeping system, and a tax preparer who files everything correctly. From the outside, everything looks under control. But inside that setup, money is leaking quietly.

For example, a Tallahassee consultant earning $350,000 as a sole proprietor pays full self-employment tax plus top federal rates. There’s no salary structuring, no distribution planning, and no control over how that income is taxed. That one decision alone can cost tens of thousands every year — not because something is wrong, but because nothing was optimized.

This is where most business owners get stuck. They assume if nothing is broken, nothing needs to change. But tax inefficiency doesn’t show up as an error. It shows up as money you never realized you could have kept.

So the real question becomes: when does that change — and who actually changes it?

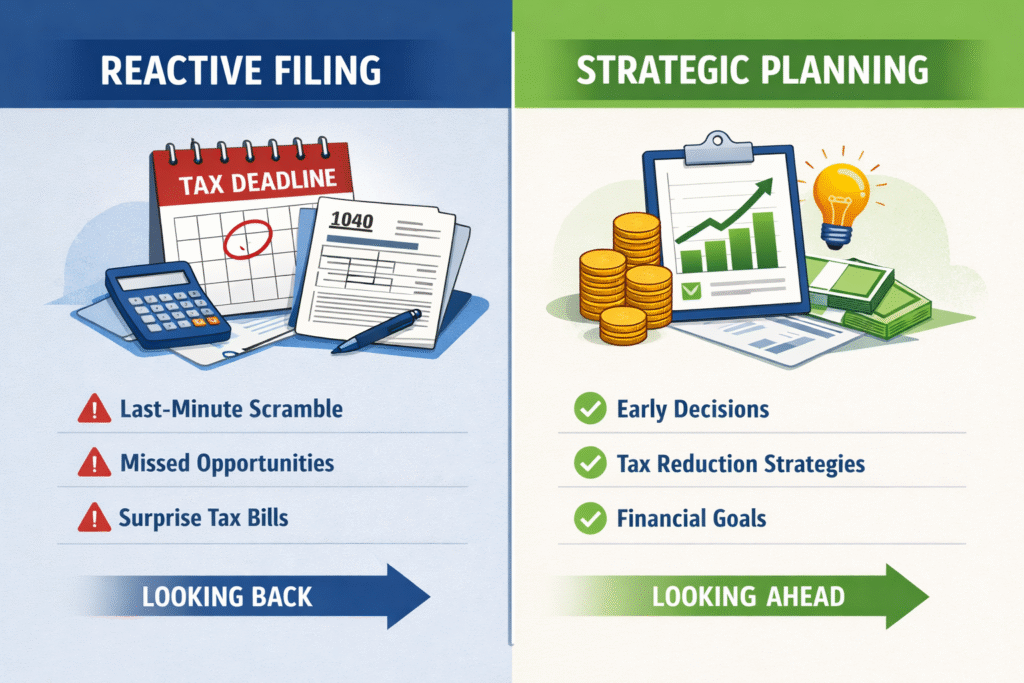

The moment where taxes stop being reactive

Most business owners think tax savings happen when the return is prepared.

That’s where the misunderstanding begins.

Filing is the final step. Planning is what happens months before that.

The first time this shift matters is when it’s introduced: decisions made during the year determine what is even possible at filing. If you wait until April, you are working with fixed outcomes.

The second time it matters — and where it becomes real — is in how those decisions play out. Imagine two business owners in Tallahassee, both earning $400,000. One restructures into an S-Corp mid-year, sets a reasonable salary, and distributes the rest. The other does nothing and files as a sole proprietor. Same income. Completely different tax outcome.

The third and final time it matters is this: if no one is guiding those decisions before year-end, you are not controlling your taxes — you are accepting them.

And that leads directly to where most of the money is actually lost.

Where the real tax loss happens (and why you don’t notice it)

The biggest losses don’t come from obvious mistakes like missed deductions.

They come from decisions that feel normal.

Take this scenario:

A business owner grows from $120,000 to $400,000 over three years. The business evolves, but the structure doesn’t. They continue operating the same way because it worked before.

But at $400,000:

- Self-employment tax becomes a major burden

- Income hits higher federal brackets

- Timing decisions start to matter significantly

What worked at $120,000 becomes expensive at $400,000.

Nothing broke — but everything became inefficient.

And inefficiency at that level compounds. It repeats every year. It scales with your growth.

That’s why the solution isn’t fixing a mistake. It’s redesigning how the income flows.

What actually makes a CPA “the best” in Tallahassee

It’s not credentials. Every licensed professional meets that bar.

The difference is whether they change outcomes or just report them.

The best CPA asks questions that force decisions earlier:

- If your income grows another 30%, what breaks first — cash flow or taxes?

- If you sold this business in five years, how would it be taxed today?

- Are you building income, or building something that reduces future taxes?

And then they act on those answers.

For example, instead of saying “you should consider an S-Corp,” they show you:

“At your current income, staying as a sole proprietor is costing you approximately $25,000–$35,000 a year in unnecessary tax. Here’s how that changes if we restructure now.”

That level of specificity is what turns advice into action.

And that’s where John’s work becomes visible in a way most business owners haven’t experienced.

How John Geantasio changes the outcome

When a Tallahassee business owner comes to John earning $400,000 as a sole proprietor, he doesn’t start with the return.

He starts with exposure.

He calculates how much of that income is being taxed at the highest rates and how much is unnecessarily subject to self-employment tax. Then he shows, in actual numbers, what changes if that income is restructured.

For example, shifting part of that income into an S-Corp distribution model can immediately reduce tax liability while keeping compliance intact. From there, he layers in timing strategies — when to recognize income, when to accelerate deductions, and how to align both with long-term goals.

The difference is not theoretical. It’s measurable in dollars.

And once that structure is in place, the focus shifts from reducing taxes today to building something that keeps working over time.

Building a financial fortress — what it actually means

Most business owners think in terms of yearly income.

But tax strategy, done correctly, is about building something that outlives the year.

A financial fortress is not just savings. It’s a system of assets and decisions that protect and grow your wealth over time.

The walls of that fortress are built from:

- Tax-efficient entities that reduce ongoing exposure

- Assets like real estate or investments that generate income

- Depreciation and credits that offset taxable income

The foundation is how your income is structured before it is taxed.

And what it protects you from is not just high taxes — but volatility, poor decisions, and years of lost opportunity.

The tax code is designed to reward those behaviors. Business ownership, investing, and asset creation are not just financial moves — they are tax advantages when structured correctly.

Without that system, income stays temporary. With it, income turns into long-term leverage.

And that only works if it’s implemented at the right time.

Why timing is where most strategies succeed or fail

Most business owners delay decisions because nothing feels urgent.

But tax strategy is time-sensitive by design.

A restructuring decision in March affects the entire year.

The same decision in December has limited impact.

For example, choosing when to recognize income or when to make a major purchase can change your tax position significantly — but only if done before deadlines pass.

This is why two business owners with the same numbers can end up with completely different results.

Not because one worked harder.

Because one decided earlier.

Who this matters most for in Tallahassee

This becomes critical when your business reaches a certain level.

If you are earning:

- $150,000+ and your tax bill feels high

- $250,000+ and your structure hasn’t changed in years

- $400,000+ and you’re still making decisions at year-end

Then the gap between what you pay and what you could pay is no longer small.

At that point, every year without strategy is not neutral — it’s expensive.

So the question is no longer whether planning matters.

It’s whether it’s already costing you.

FAQs — Best CPA in Tallahassee, Florida

Do I really need a CPA if Florida has no state income tax?

Yes, because most of your tax exposure is federal, not state. Florida eliminates state income tax, but federal taxes, self-employment tax, and entity structure still determine what you pay. For example, a business owner earning $300,000 can still lose a large portion to federal taxes if structured incorrectly. The lack of state tax often creates a false sense of efficiency. In reality, federal strategy is where the biggest savings come from.

When should I start tax planning during the year?

You should start in the first quarter, ideally before your income pattern is fully set. Early planning allows you to control how income is earned, structured, and taxed throughout the year. For example, choosing an S-Corp election in March impacts the entire year, while doing it in December has limited benefit. The earlier you act, the more options you have. Waiting reduces flexibility and locks in outcomes.

How do I know if my accountant is missing strategy?

If your conversations happen only during tax season, strategy is likely missing. A strategic advisor engages throughout the year and focuses on decisions before they are made. For example, they should guide entity changes, income timing, and investment decisions proactively. If your accountant is only reporting what already happened, they are not influencing the result. That gap is where most overpayment occurs.

Is changing my entity structure really worth it?

Yes, because your entity determines how your income is taxed. A sole proprietor pays full self-employment tax, while an S-Corp allows part of that income to be structured differently. For example, at higher income levels, this shift alone can create meaningful savings. But it must be done correctly and aligned with your situation. The impact is real when executed at the right time.

What’s the biggest mistake Tallahassee business owners make?

The biggest mistake is assuming their current setup is still appropriate as they grow. Many businesses start simple and never evolve their structure as income increases. For example, a business that worked well at $100,000 becomes inefficient at $300,000 or more. That gap creates unnecessary tax exposure year after year. Growth without adjustment is where most money is lost.

What happens next

You already have the business. You already have the income.

Now it’s about whether that income is structured correctly.

Work with John, and your numbers get redesigned before they’re reported.